Why Buy Now, Pay Later is making a comeback in the Mumbai real estate market? Even Raymond seems to making this offer

Now that the shareholders meeting is concluded in favor of creating two separate companies, when do we expect the process to start and we get shares of the new company?

For the demerger process to complete and to list, management has given guidance of Q1 25, may be one more quarter if some delay, I have been adding since 1500, though there is some problem with chairman, management is fully professional

[Can Raymond be a Turnaround Story?]

Raymond is a very prominent name in Men’s Suiting. I guess everybody in India would know the Brand Name. But not many people would know that Raymond is also present in Realty as well as in Engineering in national and international markets. They also had a Consumer Care business which is acquired by Godrej Consumer Products Ltd. for 2825 crore. As this sale took place, they turned debt free 2 years ahead of guidance. They currently have 1100 crore on cash as of September, 2023. Additionally, Raymond issued NCD of 1,700 cr to RCCL to facilitate the repayment of external debt of 1,029 cr in 1QFY24.

Under their textile business, they cater to the B2B and the B2C space. They have brands like Raymond, Park Avenue, Parx and Colorplus. They also cater to Indian wear via their brand Ethnix. They have also diversified themselves into Custom Tailoring. The company has made 46 net store additions during the quarter to take total at 1,453 as of Sep’23 v/s 1,376 in Sep’22. Raymond plans to open 200 retail store in next 12-18 months. The textile segment saw a revenue growth of 40% from FY22 to FY23. PBT grew by 97% from FY22 to FY23. ROCE of this revenue segment is around 60%.

Raymond Realty started in 2019 with the development of a small piece of land in Thane to introduce a new standard of living that pushes the envelope on every aspect – construction quality, design aesthetic and comfort feasibility. The company has about 120 acres of land parcel at a prime location in Thane. Nearly 40 acres of land is under development for revenue potential of 9000 cr while 60 acres (~7.4 million sqft) has another saleable potential of 16,000 cr. Revenue in FY23 was 1115 cr from 700 cr in FY22 which saw a 57% growth. PBT grew from 143 cr in FY22 to 276 cr in FY23 registering a 93% growth. ROCE of this revenue segment is around 58%.

Now coming to their Engineering division, one of their subsidiaries is JK Files & Engineering (JK Files) which is involved in the manufacturing and sale of precision engineered components for tools and hardware such as steel files, drills, hand tools and powerful tool accessories as well as auto components such as ring gears, flexplates and water pump bearings.

Another subsidiary is Ring Plus Aqua Ltd (RPAL), a prominent Ring Gear, Water Pump Bearings and Flexplate manufacturer in India. It has a market leadership position in Ring Gears with a volume share of more than 50% in Passenger Vehicles and more than 45% in Commercial Vehicles in India in Fiscal 2021.

Coming to their latest acquisition of 59.25% stake in Maini Precision Products Limited (MPPL), they are trying to get into the sunrise sectors of EVs, Defence products & Aerospace parts. This transaction will be completed by FY24. Bengaluru-based MPPL has a 70% exports contribution and generated around 750 Cr in revenue in FY23.

Raymond will then consolidate its engineering business of JK Files, RPAL and MPPL under one entity building scale and size and will form a new subsidiary ‘Newco’. Raymond will hold a 66.3% in ‘Newco’ that will focus on precision engineering products. The proforma consolidated revenue of ‘Newco’ as of FY23 are Rs 1600 crore with an EBIDTA of Rs 220 crore. 60% of the revenue in FY23 is coming from exports.

MPPL has a good hold in Europe and North America market which will eventually help Raymond’s engineering division gain its market share in those regions. They also have a great client base like Bosch, Eaton Vehicle Group of the US, Danfoss of Denmark, Marelli Powertrain India, Volvo Group of Sweden, Cummins India and BorgWarner Cooling Systems, Safran Aircraft Engines, Marshall Aerospace, Eaton Aero, ITP Externals SLU, Parker Aerospace and Woodward Inc.

Coming to the leadership of the new conglomerate Newco, Gautum Maini will be leading the business who has been leading Maini Precision since last 26 years. He expects the combined business to drive a top line growth of 15-18% and EBITDA by 20%. There is no major Capex required for further expansion and the free cash flows are enough to service the interest and debt repayments of the consolidated engineering business. Margin improvements are likely by 250-300 basis points. In FY23, if we consolidate the revenues of the above Engineering conglomerate, it comes to around 2000 crores. Engineering businesses these days enjoy a MCap/Sales Ratio of around 4. So if we consider the same for Raymond, the Market Cap comes to around 8000 crores (66% of current Market Cap of 12000 crores).

The stock presents a Reasonable Valuations at current prices as compared to the fundamental developments that are happening. However, there are a few negatives as well. Promoter’s Family Feud has been affecting the stock price as well. The most affecting point in this Family Feud for retail shareholders is how much of the family’s wealth Nawaz Modi Singhania (Gautam Singhania’s wife) eventually demands in the wake of the separation. Another point that comes to mind is the pledging of promoters in the company.

But the new developments in the company, especially taking their Engineering Conglomerate and their Land Bank into consideration, it posts a positive picture about the company fundamentals. Thus, I believe the stock could be a good turnaround story.

Happy Investing!!!

4 Likes

Nice detailed notes.

Just one observation on the valuations of engineering business. JK files revenue has been stagnant for some time now and not sure of revenue CAGR of Maini. Hence, valuation of Market cap to Sales ratio of 4 looks quite rich. Also, on the combined engineering entity, Raymond would only be holding 66% and wouldn’t own it completely.

Another point to consider is denim business that’s a 50-50 JV. The fact they want to retain it at Raymond Ltd and not Raymond Lifestyle indicates they might sell it at some point like they did with FMCG business. So, we need to add the value of the denim business as well to overall group valuation

3 Likes

Dear All

currently Raymond has only hangover of Family dispute. It makes me nervous to hold. I was holding it since last 4-5 years but sold it when family dispute came in the news

Prashant

1 Like

Hi All,

I’m an aspiring ER analyst and have been tracking Raymond LTD. for 3 months.

What is the corporate governance issue that everyone mentions about this company?

My analysis hasn’t pointed out any serious red flags.

Thanks in advance

Sir, would you mind sharing your analysis here for the benefit of all members?

Sorry, I have no idea about corporate governance issue. Thanks

As far as I know, the in-fighting in family over renovation costs of JK House (if it should be taken up by Raymond Ltd or not) was the major issue that created lot of headlines many years ago.

Other than that, there was a recent news article about how Gautam Singhania bought foreign luxury cars using company resources & people to avoid customs duty

Not sure of any other issue

Trying to make amends with his father ? If yes, it’s good for them and for company

1 Like

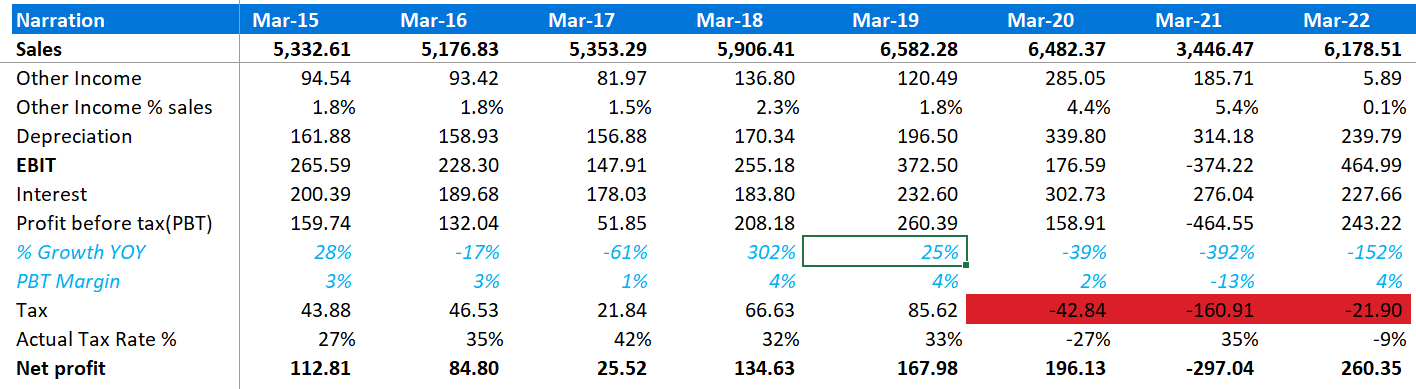

Tax is negative in the year FY20-FY22, can anyone explain this to me and should this reduce the loss in PAT as given in screener.

any update on the demerger?

Should happen by Q1 end or most certainly by Q2

got it - searched recent news but no announcements yet on final date.

Whats your estimate on the value that demerger can create?

thanks - this is helpful. So basically the record date is yet to be announced. The stock should rise once they announce that

Good set of results, especially from real estate division. Good EBITDA margins as well.

But I don’t understand they keep restructuring the group business very often. Post de-merger, Raymond Ltd is supposed to be a real estate company with 63% holding in the merged engineering entity (which includes Maini precision). Now, they are carving out the A&D part from the engineering business and will keep it separately.

Hence Raymond Ltd (being primarily an RE company) will hold 63% in these two entities (Engg and A&D)

1 Like