Interesting capacity coming up in Thailand from competition.

3 Likes

Today, India officially entered in to recession by posting GDP de growth for consecutive 2 quarters. Auto sector is cyclical, so it is natural that Rajratan global wire has de growth.

The recession definition is not correct please. It should be negative growth for 2 consecutive quarters over previous year. India is very much growing - lower positive growth is not negative growth

10 Likes

50,000 shares purchased by promoters from market last fortnight in the price range of 718 -746

1 Like

22nd Mar23 --Rajratan Global Wires–CNBC Interview :

–Customers are telling us that growth will be more than GDP growth in India. Also forcasting growth in export of tyres so overall 65k tons tyre mkt is to grow to 1.65Cr mkt by 2030 so if we factor all these no.s we are looking at growth of 10% in Indian demand for bead-wire next yr.

–Special sectors like commercial tyres we are witnessing good growth and in PV sector also its good growth but 2W which is rural economy based demand is not doing well

–Volume growth for FY24 --10/15% in India i.e currently we are close to 59/60k tons which will grow to 65/68k tons in India and Thailand was more of a problem last year as Thai tyre cos are there to export to europe and USA and it was low traction there due to geo-politics / freight rates had gone high / demand destruction in US and Europe and people had high inventory --now this has normalised.

–Looking at current indications from cust in Thailand and exports from Thailand we are projecting 30/35% growth in Volume in Thailand

–Blended it will be 20% growth for FY24

–Margins will be retained at 18/20%–Projections are based on this. Tgting bigger mkt share which will not be possible with a high margin as we are in a competitive industry

–Promoters are buying Equity and we are only in one Biz and dont want to divert our focus from this so whatever we have we investing back in this co.

–Solar Roof top project —Installed in Thailand and in Chennai also , its not a big saving but little savings in the power cost but the bottom line wont make much difference but we will continue to work on it.

11 Likes

Tepid results from Rajratan

https://www.bseindia.com/xml-data/corpfiling/AttachLive/9e1e7b78-da3e-40a2-b89b-62f5061d6251.pdf

Let us wait for addition of the new capacity. Before that it is difficult to get any improvment.

As per Investor presentation situation doesn’t seems good.

There is over supply in the market.

Operational Margin has fallen to 15 level

( I assume that it will fall further because of over supply).

Notes from Q4 FY23 concall whatever I could capture. Please counter check from the actual transcript as there might be some errors in my listening:

Overall Results & Future Outlook:

- FY24 guidance - 18 % EBIDTA at consolidated level and 15-20 % growth in revenues.

- Indian tyre market expected to grow to Rs.165,000 crores in 2030 from Rs.65,000 crores in FY23. This is what the tyre manufacturers are expecting. Tyre exports may double, as per our customers.

- Currently we have 8 % global market share.

- Total production next year - expected to be 110,000 tonnes.

- RM costs have now softened, we are seeing about 2 % reduction this quarter.

- Thailand tyre companies are mainly exporting whereas Indian tyre companies mainly sell to domestic market. This is the difference between Thailand & Indian tyre market.

- There is no major disruptive technological change in bead wire as a product.

- Shift to EV - only change this will cause is EV requires lightweight tyre, noiseless tyre. There is no change in the requirement of bead wire in that. EV vehicles are heavier as batteries are heavy, so if anything, tyre requirement will be higher in future.

- We are world no. 4 or 5 probably but Chinese numbers are unreliable. Ex-China - we will be 2nd biggest in the world after 180,000 TPA expansion is complete.

- Time lag in passing on RM cost price increase to customers is 1.5 months approx.

- Bead wire cost is 3 % of the tyre cost.

Thailand:

(There was a lot of discussion on Thailand since that is where the company has taken a hit)

- Saw Chinese competition in Thailand, they were selling at lower prices while we decided to hold our prices. So lost market share and volumes were lower.

- Five main Chinese competitors (could not understand the names). They are much bigger companies with bigger capacities in China.

- In Thailand, EBIDTA margin was 8.5 % in Q4.

- Thailand supplies to Bridgestone and Continental. Their requirements came down this year.

- Earlier the customers were operating at 50 % capacity since July but now since Feb - March onwards there is a pick up.

- Our Thailand market share in the last quarter was 16-17 % vs 20-25 % generally. The dip was due to 5 Chinese tyre companies who shifted to Chinese bead wire companies. And Sumitomo - one of our major customer - operating at a lower level.

- In Thailand, we expect minimum 40,000 tonnes sales (70 % capacity utilization) next year, up from 30,000 last year. But at lower margins.

- We expect 14 % EBIDTA margin in FY24.

- No major capex required here now.

India:

- We saw 15% growth, Production target for FY24 is 70,000 tonnes in FY24.

- We expect EBIDTA margin will be above 18 %, may be 20 % also.

- In India there is less competition.

- We are the only supplier to Michelin in India. But it is incremental demand and does not multiply the demand.

- Current level realizations in India will sustain if RM prices remain the same.

- Chinese bead wire companies cannot sell in India, there is no threat from them here. They used to sell in the past when there was 13 % subsidy given by their govt. But not now.

Chennai Plant:

- Rs.30-40 crore capex this year before the production starts. Total Capex in Chennai is Rs.160 crore.

- New plant may start production in H2 of this year but our projections do not include any production from Chennai.

- PLI benefits - we have requested to shift the benefits one year forward which the govt has agreed. So, it will start in FY25, not FY24.

- Scale up of Chennai plant - it will take 3 years to achieve full utilization.

Exports market:

- Discussions going on with several customers at an advanced stage - Bridgestone, Continental, Euro + 3 - 4 Korean tyre companies.

- Next year lot of volumes will go to Europe and America.

- China de-risk trend is still on, companies looking at India now.

- Europe demand is now picking up, nobody is talking about war or energy crisis.

(Disc: Invested)

18 Likes

Rajratan Global Consolidated June 2023 Net Sales at Rs 203.85 crore, down 18.92% Y-o-Y

| Financials | Q1 FY2024 | Q4 FY2023 | % Change |

|---|---|---|---|

| Total Income | ₹ 205.15 crs | ₹220.27 crs | -6.86% |

| Net Profit | ₹12.43 crs | ₹20.28 crs | -38.71% |

| EPS | ₹2.45 | ₹3.99 | -38.60% |

The quarter witnessed aggressive competiton in our Thailand business coupled with sharp drop in realisation (led by drop in raw material price), thereby impacting our overall revenue growth and profitability in Thailand operations, inspite of volume growith in Q1FY24 versus Q4FY23.

2 Likes

After the Q4 FY23 results, the management guided for 15-20 % growth in revenues and 18 % EBIDTA for full year FY24. If this has to come true now, company needs to record a revenue growth of 28 % in the remaining 3 quarters of the year. Operating margin for Q1 was 12 %, so achieving 18 % for the full year is also a tall order. After Q4, the management said there was Chinese dumping in Thailand, and they erred in trying to hold on to their margins, which led to a loss of market share. But now, they have decided to match the prices and so volumes would recover. They did, but my impression was that while Thailand problems would be arrested, India was doing fine already.

But in Q1, volumes in India have dipped QoQ, and are now at 14,717 MT. At this rate, the volumes for the full year FY24 will be 58,868 MT, almost flat for the year. More worryingly, the Q1 presentation contains two sentences that foretell trouble ahead.

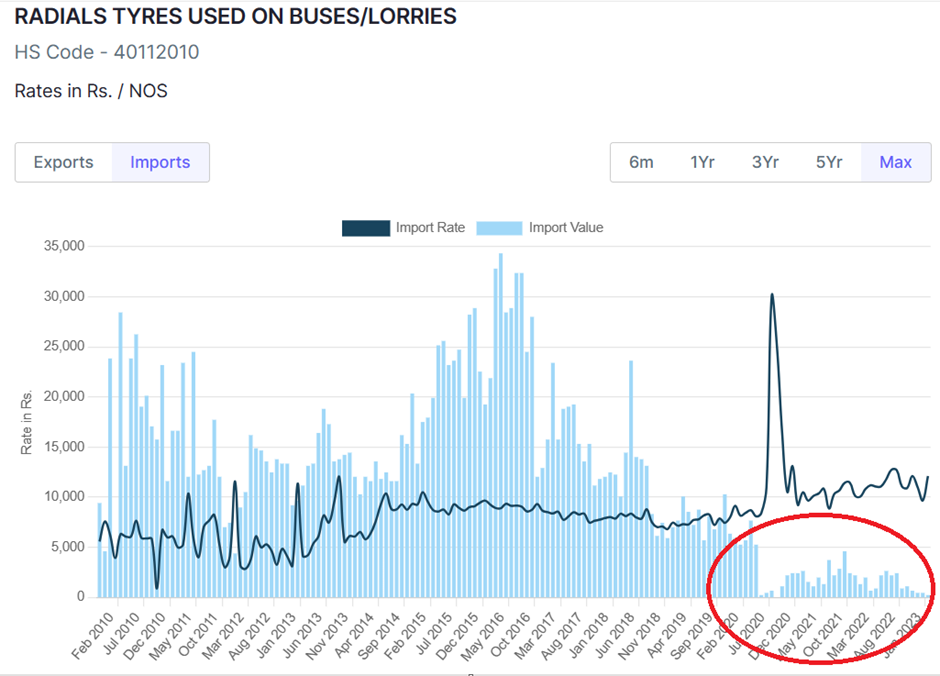

The CMD says there is “increased competitiveness in imports from global players”. I am not sure if he is talking about bead wire or tyre imports, but either way this is surprising and worrisome. Tyre imports were put on restricted list category in June 2020. Though the ban is still in place, it is possible the government has become more liberal in giving out licenses for import. Rajratan’s revenue boom had coincided with this tyre import ban.

Secondly, the investor presentation also talks about “expansion in capacity by one of the competitors”. It is not clear who this competitor is, but I understand the other main bead wire player in India is Tata Steel with a 33 % market share. Tata Steel’s AGM presentation talks about wire capacity expansion of 100,000 TPA underway. I assume this is wire rods, so not all of this will become bead wire perhaps, but their aggressive forward integration plans across the broader steel value chain are well known. Rajratan cannot win a price war with Tata Steel, since price cuts do not hurt them as much as they do Rajratan.

My reason for pointing out all this is that Rajratan is doubling its domestic capacity at a time when demand is under pressure and supply has increased. Even in the best of times last two years, the company has struggled to grow its India volumes as the below table shows:

Q1 FY24 results show company level margins have already gone back to pre-Covid levels. Pre Covid, the company’s average OPM was 10.89 %.

All this points to ominous signs going ahead, especially when we look at the Balance Sheet.

Consolidated Debt is currently at Rs.170 crore and will rise further in the coming year. Rs.30 to Rs.40 crore capex is the remaining for Chennai plant. Short Term Liabilities maturing within the next 1 year as per the latest Balance Sheet are Rs.130 crore. Assuming fixed operating costs of Rs.60 to Rs.70 crore per year and interest of Rs.20 to Rs.25 crore, the company needs around Rs.250 to Rs.300 crore of cash (40+130+70+25=265) to run its operations.

Currently, Receivables are Rs.136 crore. CFO in FY2023 was Rs.162 crore, but this includes strong numbers in the earlier part of the year. If we go back to pre-Covid numbers (which is what the coming year is going to resemble), CFO used to be in the range of less than Rs.50 crore per year, at around 10 % of revenues. At Rs.800 crore of revenues in FY24, this will be Rs.80 crore at the most. This (136+80=216) still leaves a gap of around Rs.50 crores to be filled at the minimum. This gap will have to be filled with more borrowings, which in turn creates further pressure on future cash flows, and so on.

And all of this is the optimistic scenario, as I have just annualized the Q1 numbers. If the declining trend in revenues (see image below) continues in Q2 - as it appears from the management commentary - things would be worse. Any further loss of volumes in the domestic market will spell the doom for the company. See the declining trend in the image below:

If we annualize the performance of Q1 for the full year (again: optimistic scenario!), company will end the year with a PAT of Rs.50 crore which gives an EPS of Rs.9.79 per share. At a median PE of 18.5 (pre-Covid was actually 15!), that gives a share price of less than Rs.200 per share.

To summarize, Rajratan’s debt funded capex is coming in at the wrong time, the expected demand pickup has not materialized and there is a supply glut in a commodity product. These problems are not cyclical but structural in nature.

(Disc.: No positions. I may be wrong, so do your own analysis.)

28 Likes

Recent interview from Sunil Chordia after Q1FY24.

2 Likes

Short term liabilities of 130 cr will not become 0…it will be more or less at 130 cr…hence those funds will not be required and to that extent your calculation is erroneous.

@chandragupta

The competitor is Tata steel who has expanded capacity by 25,000 tonnes. I got this info from kaptify person which manages investor relation for Rajratan. Also the bead wire import happened from Kiswire which is a korean based company and the Michelin imported it from them. The import however is not much and its around 15,000 tonnes out of a total of 130,000 tonnes of domestic consumption. Now the competition has increased however we must also take into account that tyre companies are increasing their capacity so naturally demand will increase and accommodate additional capacity created.

9 Likes

Rajratan Global Q2FY24 Concall Summary

3 Likes

The previous quarter had shown initial offshoots of improvement in Thailand, while in Q3 we have

achieved 80% capacity utilisation in Thailand, leading to 73.5% volume growth YoY. We have witnessed stiff competition, causing pricing pressure leading to lower operating margins. However on a blended basis we were in touching distance of 15% EBITDA Margin led by higher volume growth in Thailand. We are incorporating a subsidiary (sales, marketing & warehousing) in USA and sales and marketing offices in Europe to focus on our export business. Chennai expansion is on stream and will start trial shortly and commercial operations in Q1 FY25. While the last 12 to 15 months have been challenging due to various global factors, we have always excelled in coming out bigger, better and stronger from these challenges to Outperform. We continue to do so to make Rajratan a leading and large player globally in the business of bead wire.

2 Likes

The company is losing its pricing power due to intense completion from China however I believe this would be temporary. Sunil Chordia has said that they have seen Chinese competition and come and go in last 25 years. I believe domestic Chinese economy is not doing well and hence the Chinese companies are dumping in international markets. Not just Rajratan but specialty chemical companies are also facing intense competition from China. Some time in the future, the Chinese players will start supplying more locally once their economy picks up which will open up opportunity and reduce competition in international markets. I also believe US and Europe are lagging in demand due to higher interest rates. Interest rates are likely to lower as US elections are nearing and these high interest cannot be sustainable for a long time. Customers in these regions rely heavily on borrowing so with easing interest rates, demand from them is bound to increase. Domestic demand is also likely to increase looking at the expansion plans of tyre companies. With demand increasing in near term domestically as well as internationally, I believe demand will outpace supply and pricing power will be regained. However, this will take some time and I don’t see this happening at least for a year minimum. I could be wrong but this is how I think the scenario will play out. Market is currently reacting as if the company is going bankrupt.

8 Likes

Latest Concal:

Management:

Yes. So, our main competitor is Tata Steel. They have increased the capacity last year. Okay.

And they will also try to push bigger quantity.

No, first year, I will not, would not like to give any number on EBITDA from Chennai.

Because it’s a new plant, it will take some time to stabilize.

Very difficult to predict what China will do. We will have to look at government support to

whom fight with China because they supply without margin, they supply at a loss also. So, that is not a competition we can talk about. Otherwise, we are competitive with any other country,any other plant in the world other than China.

Tata Steel has capacity of 60 KT.

1 Like