Anyone tracking recently.

Does anyone have recent input for fundamentals.

1 Like

Anyone actively tracking this company.

I am invested and wanted to get more info however very limited information is availlable on there site asl Annual report is not that informative.

of some one is tracking please share the input.

Corp governance issues highlighted by the account below

https://twitter.com/BeatTheStreet10/status/1664906129942646784

Disc: Not invested

2 Likes

Hi @Donald ,

I am invested in Rajesh export for last 2-3 years.

very limited information available about this company however I invested based on Rajesh’s mehta’s interview.

Question : are you still follwoing this company and having connect with Management? if yes - pls share more inputt on this company.

Hi @Donald ,

I have a few concerns regarding the company and would like your views on them if you are still following the company.

#1. Promoter promises but doesn’t deliver repeatedly. Ex: They were saying in 2005 they will increase margins, also in 2010, also in 2015 and so on. But Margins have fallen from 2.5 % in 2010 to less than 1 % now!!

#2. 0.2% dividend yield (5% of profits, and profits are not increasing yoy for many years now!!).

#3. Tax rate of 3% (biggest issue for me, I want to understand this point specifically). Has fallen from 8-9% in 2010 to 3 percent now!!

Point #3 is my biggest concern and I couldnt find any reason for it.

If anyone else has any views (or any facts which would be even better), please add to the dicussion.

Hey @Shubham_Jain1 ,

I have been studying the balance sheet, performance and tracking information about Rajesh Exports. You are true on many of the facts, but as per my knowledge exposure till now (where I could be wrong)

-

Balance sheet shown is cumulative of all it’s subsidiaries, from the Auditors comments mentioned at NSE disclosures also we can see they do say two subsidiaries resulted were not audited by them and they were accepted and according to the law of the respective country. (AFAIK this should be Valcambi, Switzerland.

-

Tax Rate slab falling from 8% to 3%, could it be because of India’s Tax Policies, I could just find this article but these all might be wrong too

But the only thing pushed me to buy this stock under this range as it is very close to it’s PB and recently video from Vivek Sir did provided meaningful insights what must be going on.

Cons:

- Management is not friendly (not to credit ratings, not to investors) in terms of providing big details

- Transparency is not very good, very limited and necessary information is published by them only

Disc: invested

1 Like

My assumption is that this is due to their acquisition of Valcambi in 2015 for 400 million USD. Valcambi is the world’s largest gold refiner and refineries work on very thin margins. So this adds a lot to their revenue but not necessarily to their bottom line.

Result: Broken promise ![]() and narrow margins!

and narrow margins!

1 Like

True. The Valcambi business which they acquired 7 years ago totally changed their revenue and OPM. What we need to bother is how company can improve on its margin going ahead because revenue has doubled in 4 years but profit has decreased by 15%.

An outstanding achievement by the company is to bring down the debt/equity ratio from 1 (immediately after Valcambi acquisition) to 0.05 now.

Management transparency is the negative factor. But i have been accumulating for the last 2 months since P/B = 1, D/E = 0.05 and business is more like consumer discretionary.

1 Like

Stock has been bitten down badly ,falling to long term support level of 440 with high volumes. What lies ahead?

3 Likes

Can anyone throw highlight on what is happening to this share since last month as it has been down to its 52 week low and near to its book value now

Not sure whats going on. fundamentally seems they are doing good. however transperancy to investor is very less so not sure whats going on.

Can someone please throw light on this? Thanks

2 Likes

The probable reason on why it continues to slide.

https://twitter.com/BeatTheStreet10/status/1724706663427609010?t=WICbzsR74OF3bz6RYc704Q&s=19

2 Likes

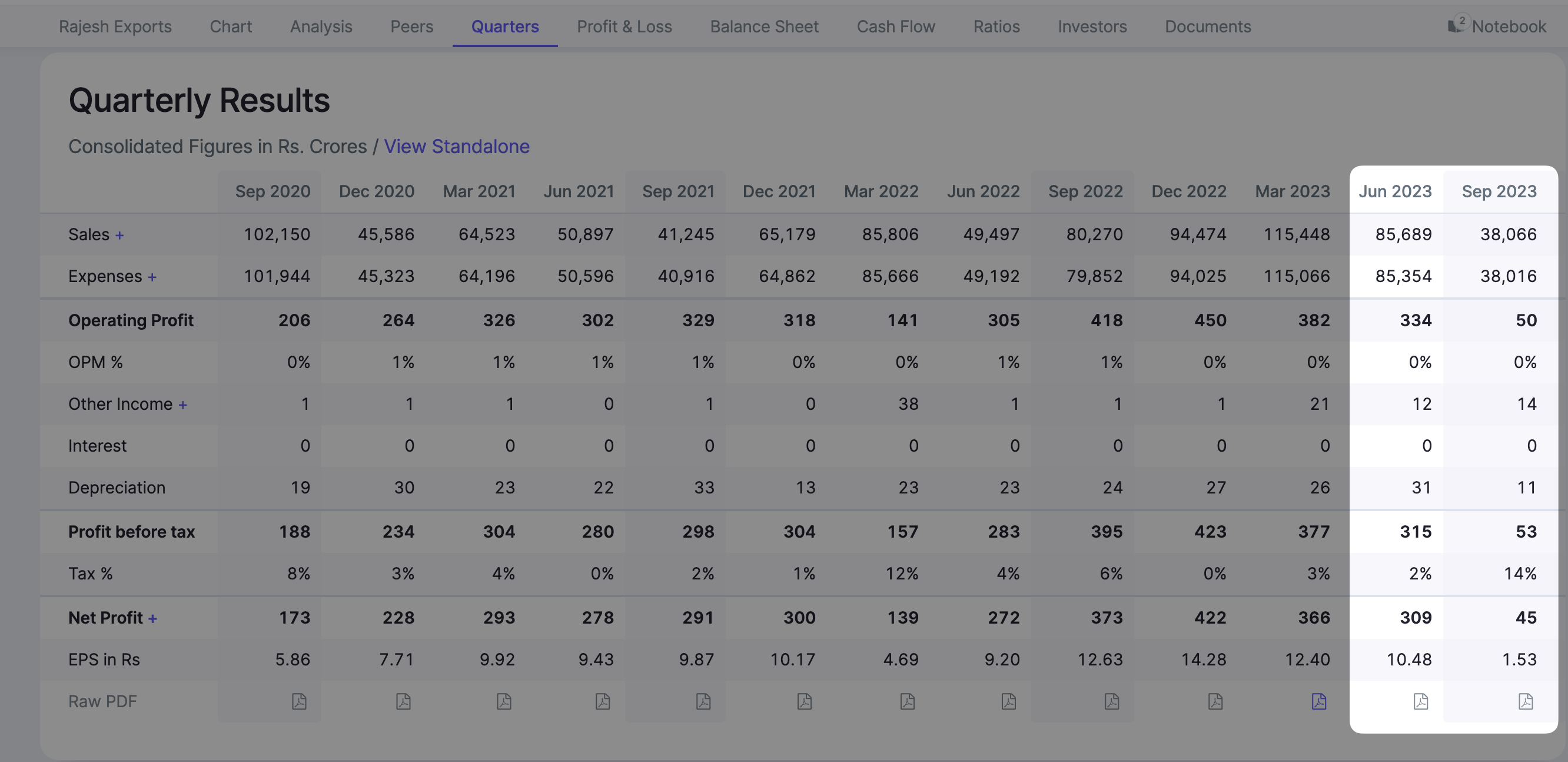

Indeed, the company hasn’t followed the financial report compliance. However, the Sep 23 Sales and profits have fallen more than 60%

The major problem that as Investors we face is that we are unable to find the reason for such a dramatic fall in the data. Thus, it is hard to conclude what is happening with the company and importantly what to do from here.

3 Likes

I think Rajesh export management need to be more transperent for minority share holders. they seems to be just working in the business but not bothered about sharing information to their own share holders.

last investor presentation was done in 2020,where they mentioned about their focus on retail which will increse their margins. post that there is no update on retail business progress nor we are able to see its impact on their profitability number.

@Donald - if you have any ground update

1 Like

Rajesh-Exports-2Mar2021.pdf (353.6 KB)

Something fishy with related banks too is being cooking

1 Like

pls share intellegence from the shared report.

one observation : this is March -2021 document. is this still relevent?

1 Like

Is this a good time to buy?

No, unfortunately it is not.

1 Like

I remember reading a Covid time financial dispute with Canara bank? Felt it was a genuine disagreement due to an unexpected extraneous factor and the company had deposited a large amount till adjudication.

I have a small stake in my high risk portfolio (was a mistake and i ignored the obvious red flags on corp governance.) But staying out as my bet was on Valcambi, which has signed a JV with a Middle east conglomerate. The deal ia controversial but may bump up turnover by 10%.

1 Like