These are derived from the cost to the dealer of providing thebasic transaction. Where forexample the client is a buyer of the forward, it is the cost to thedealer of borrowing currency to the forward date to finance a spotmetal purchase, less an interest rate to reflect the rate at which themetal can be lent out until maturity of the forward. The majordeterminant in the calculation of this rate is the availability, oraliquiditya, of gold, silver, platinum or palladium to fund metal inthe case of forward sales.

Forward rate = Dollar interest rate a metal lease rate.

Traditionally gold interest rates are lower than dollar interest rates.This gives a positive figure for the forward rate, meaning thatforward rates are at a premium to spot. This condition is oftenreferred to as contango. On very rare occasions when there is ashortage of metal liquidity for leasing, the cost of borrowing metalmay exceed the cost of borrowing dollars. In this scenario, theforward differential becomes a negative figure, producing aforward price lower than, or at a discount to, the spot price. Thiscondition is known as backwardation.

I was trying to see how many times in History has the Gold Forward differential become negative - to establish any real risk - and came across this piece.

My initial thoughts, as I looked at my objections, and decided to pursue further. Not enough facts on the Table:) Sharing so that we can have some more converts help us dig more!

1). Gold Industry -Not for me. Thisis

**

REL grew only by Exports till 2010 ~18000 Crs. Gold Import/Export is a highly regulated activity monitored directly by the RBI. All contracts are backed by LCs with Banks that demand a 1:1 collatoral. 100cr order => 100 Cr LC opening => implies 100 Cr FD must be maintained with Bank

_

_

So where is the scope for any malpractices/laundering/hawala? I had to give REL the benefit of doubt here

2.This talk.The **

Yes. And I take this very seriously. Without the benefit of a blind Management Q&A date that we had, I would have most probably given this a pass. But as we spent the 8 hours at REL factory and offices and discussions, interacted with several people down the line… it became apparent to the sceptic in me that the strengths that REL enjoys today has been built by dint of sheer hard work, perseverence, passion and a fixed goal in front of them - over many many years of trials and errors, automation ideas/chemicals borrowed from other fields (dentistry for e.g.). I am absolutely convinced — this automated manufacturing is a work of pure passion - Only rare folks would have the vision or the guts to go after this kind of a seemingly impossible dream. Not a normal business this. This folks believe in doing things differently!

_

_

It appeared to me that the integrated refining-mfring- retail has been the plan all along. They made a success of manufacturing…and refining was the easier part to backward integrate perhaps, but retail was a different baby. They have struggled now with the format for over 5 years -2006 onwards - and getting many things right only now - The stores looked good, the product, pricing and franchisee model seemed to be working.

3). Corporate Governance )-

**

_

_

No defence. I would just like to see how Managements response when asked the obvious.

_

_

4). Is Real- **

This is an aspect that intrigues me and proably all of us. Unless there is some hanky panky why should the business quote a huge discount? Now that we are understanding some parts of the business, we can get deeper into the books. Reserve comment on this till we have all the tools/knowhow to look objectively at this.

Scale of opportunity is huge! Strengths of the company are obvious. We are now seeing success on the ground that can be verified.

**

**

why would you not want to join the efforts to investgate further??

**

**

Scuttlebutt also works here. The skeptics and we need more of you . Please help scuttlebutt the reputation about the actual business of Rajesh exports.

_

_

My limited enquiries so far in the Industry…a friend with contacts in Surat Jewleers/Diamond Traders has also been active. All feedback about the company has been so far positive form fellow players.

_

_

No one has said their books are cooked. Infatc everyone has said these guys are solid. REL has defined the Gold Industry and its development in India. They made it happen - when everyone was clueless (reference to Gold Control Act)!

_

_

why would you not want to join the efforts to investgate further??

There were many brokerages who took out reports on Rajesh Exports in 2005 - including the respected Parag Parikh Financial Advisory Services (PPFAS), when the company first talked about retail foray, acquiring Oystrerbay, etc.

Interestingly none of these reports incl. PPFAS makes any mention of SEBI strictures against REL, or the ban on accessing Capital Markets from 2003-2006!!

The balance sheet is highly leveraged… though it is not very evident. looking at the FY11 BS my observations are:

The short term liabilities amount to more than 8800 cr as they have 6400 cr Payables and 2400 cr short term loan.

This figure is huge as compared to the shareholders equity of 1597 cr, Long term loans of 115 cr, fixed assets of 71 cr (again FA is < LT loans) andinventory of 377 cr

And while the market cap is 3650 cr, you are actually paying 3650+8800 = 12450 Cr for the cash & cash equivalent of 8000 cr.Keep in mind that the borrowings are the year end figures which are usually lower than the borrowing during the year.

Looking at the Income statement, the operating margins are negative, the low net profit margins are due to other income, which is again mainly income from forward contracts. PBT is 269 Cr, while Other income is 330 Cr ( of which 240 Cr is FX and forward contracts related and Interest is 68 Cr). So the operations are making losses? Should we invest in the operations that make losses?

There are qualifications by the auditor as well in the AR which need to be noted:

pg15 of AR

" In our opinion and to the best of our knowledge and … and subject to (i) that the Company has adopted the Accounting Policy with regard to accounting of interest income on interest bearing loans other than bank deposits from accrual to cash basis, as a result of which profit for the year has been understated by r.33,08,58,068/- (as stated n Para A.6 in schedule ‘S’); (ii) that during the year 99.055 Kilos of gold jewellery is charged off from the Stocks as same is not recoverable from some of the employees and (iii) that there is no value addition in sales made in SEZ Unit of the Company in the quarter ended 31st March 2011… read with other notes…"

ThePara A.6 in schedule ‘S’ further states that import and export of gold takes place without the fixing of price.

The 99 KG of Gold would be 27 cr

This is enough for me not to waste further time on this stock, also knowing that the Promoters have not displayed the best practices earlier.

In my preliminary look most of the points raised by you have answers. Since you have made the effort I will urge you to persist and seek more information/explainations. Some answers are evident from the business model/sales process unique to REL

1). Working capital Management -REL enjoys strong bargaining power with its suppliers and gets 240 days credit (at aninterest of LIBOR + 80 bps) for making payment towards its purchases of gold. However,RELâs working capital management team effectively utilizes this credit period for generatinginterest income. From its customers, REL gets payment on cash on delivery basis andmanufacturing and delivery of jewellery takes approximately 15-20 days. Because ofhigher creditor days (approximately 240 days) and significantly lower debtor days (15-20days), REL enjoys negative working capital. The money received from customers isgenerally kept in fixed deposits for 6-8 months where company earns interest rate of 8-9%pa. This interest rate differential enhances cost efficiencies and boosts margins ofthe company.

2). Adjusting for Interest Income -REL has a unique business model with very high rawmaterial cost and very thin profit margins. Under the current accounting standards, itlooks like the company makes operating losses. Theraw material cost includes interest cost ,which suppliers add in invoice of gold, making ita part of cost of goods sold. Because of very thin processing margins (2-3% only) andhigher interest charges (4-5% pa), REL reports operating looses in its financials. On the other hand, the interestearned on fixed deposits is treated as other income. If thisinterest income is treated as business income, one would not see the Operating loss.

Will send you an invitation for the REL Investor presentation (shared at Acrobat.com). I am sure these aspects will be clear to you as soon as you see examine the details shared. We can compare notes again post that!

3). Short Term Liabilities - Yes, this needs to be dissected properly. I am deliberately wanting to get at this last. Make sure we first understand the sales process, working capital management, gold hedging/forward premia and other aspects completely before making that judgement call.

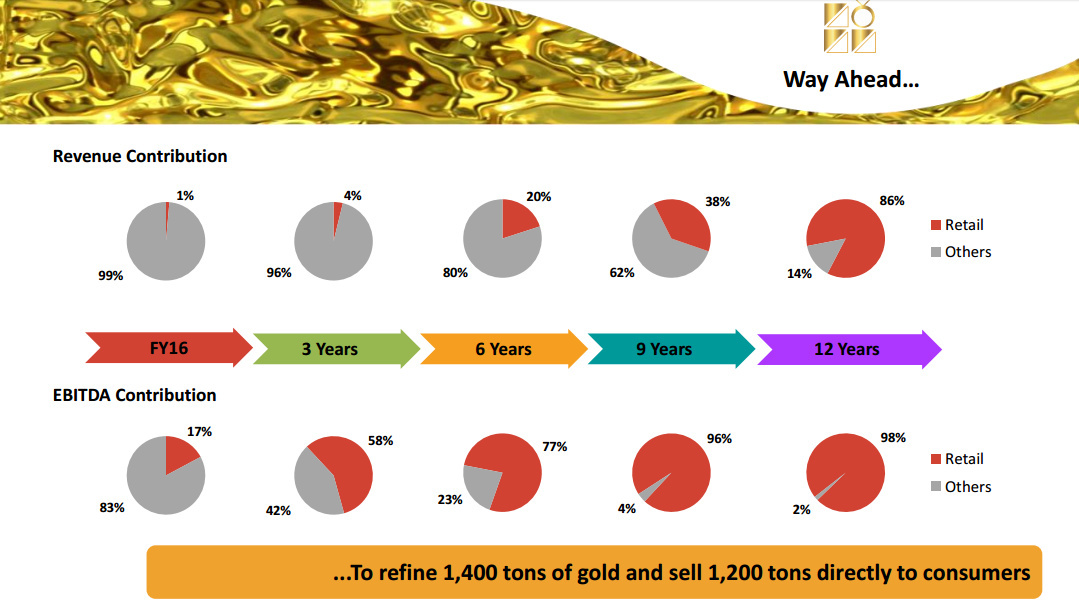

Progress of Shubh Retail Stores. Thanks Mahesh for supplying the missing links!

FY11

FY12

FY12E

SHUBH

Q1

Q2

Q3

Q4E

Stores

30

55

48

75

90

90

Sales

(Cr)

450.4

236.3

374.85

492.8

540

1643.95

EBITDA

(Cr)

21.5

12.7

28.19

32.03

32.4

105.32

EBITDA %

4.77%

5.37%

7.52%

6.50%

6.00%

6.41%

Avg

Sales/Store

15.01

4.30

7.81

6.57

6.00

18.27

The data is from company sources but from disparate announcements, conference calls, etc. There is some discrepancy on company owned vs franchisee stores, etc.

Looks like good progress to me in a years time. No of stores are likely up 3 fold. Sales & EBITDA have grown at a higher rate - which indicates good acceptance. Margins are on the way up as expected.

These two old reports also go about explaining the negative working capital cycle of Rajesh Exports due to supplier credit 240 days, but with additional interest cost of Libor+80 bps added (works out to between 4-6%). REl places FDs for 6-9 months duration at 6-9%, The differential Interest Income being treated as other Income and not Business Income results in the Operational Loss. Looks quite regular to me.

Someone had asked earlier why Tanishq or other jewellers do not face the same issue. As far as I can make it out, no other jewellery guys has the license to direct import raw gold. So it is only REL which gets this benefit of 240 days credit cycle, but padded with Libor+80 basis points additional interest cost; which REL is using ton their advantage.

just wanted to highlight that the latest AR tries to explain many of the issues raised. I found the communication quite effective and some complex topics explained well. Please give that a good read.

The company seems to be trying hard to change perceptions. Is that a good or bad thing?

Got below details from one of the article on dark side of this company

REL has just 1-2% net profit margins. How can a company which claims to be the largest and best in the industry have such low profit margins. Company’s balance sheet shows a Net block of just around 70 Cr. What kind of value addition can take place in a business where the company is earning revenues of 20,000 Cr from such low asset base. There are some other serious charges,

1.) REL is raising 2500 Cr of debt through ECB route to fund its plans. Why does a company with a franchisee/ associate model require such huge sums of money ? Where is the balance sheet strength to raise such kind of leverage ?

2.) Management has never kept its promises. Management of Rajesh Exports gave out statements in 2007 saying that the company would start improving its margins from 1.8% to 10% in the next few years. It has been 5 years since the announcement and margins are still at 1-2%.

3.) Mr. Mehta has been repeatedly promising development on the real estate front and retail from 2006, but there has been no significant progress. The management seems to be building castles on thin air and promising the moon for investors.

4.) They were initially suggesting that the company had 1300 Cr of cash and they would get 4500 Cr of credit from gold suppliers for their plans. All these plans have gone haywire. More importantly, company only recently converted nearly 150 Mn $'s worth of FCCB’s.

5.) Rajesh Exports has very bad accounting practices and we really doubt the kind of figures that have been audited. A little dig through the accounts will show that, the company suffered 40 Cr of loss by trading on MCX derivatives. Our suspicion increases with the smooth numbers of earnings and expenses during the entire downturn when there was severe volatility in Gold prices, Rupee and Demand.

6.) You would read only good news about the company as Bennett & Coleman has stake in the company. Also company has been charged by SEBI for manipulation as early as 2002.

These article was shared pretty early in the discussions.

All these points have been discussed by members. Donald has tried to deal with all of these in a detailed categorical way. Please follow the discussion thread from the start, and you may see that much of these are based on perceptions.

But there is a serious charge against the company - by SEBI - of market manipulations, and penalised. This reveals the intentions of the Management way back in 2002, and does not show them in good light.

Retail expansion is a story happening on the ground though. margins are already expanding and will expand further. Valuation mismatch is being examined in light of this.

This is not for everyone. Only for high risk takers. I will abstain

The recent budget initiative of levying excise on all unbrandedjewellrlysold in India which is resulting in a long strike all over India is a major game changer.This implies close monitoring of so far unorganized sector & clientele moving from unorganized to organized segment.

If this happens this implies

Huge size of opportunity

The evergreen formula of buying commodity n selling brand like Shubh come into place.

Now the question remains of ethical practice of the promoters.

If the promoters have learnt the lessonthen we shud closely monitor the company n make our next move.

Aint Ivery glad to see you back, value picker has got a shot of steroids now!

Wonderful to know about your work for underprivileged children, 2 months is a very long time, congrats for your efforts!

Shubh has been already analysed to a great extend. Since a major part of your interest is in the retail foray, I would like to share my experience. Me and my wife had been to one of their stores in Bangalore about a year back. She did not like the store much in terms of their collection. Even the ambience and the size of the store gave a lower-segment player image. To gain market share by attracting the big wedding spenders they need to build a high class image with much snazzier stores with better collection. Trust and brand image are big factors for traditional gold buyers.

I doubt their managerial capacity for building a great retail brand. If the intend is only to gain higher margin bus by a pan-india store presence theymight fail again.

Being the lowest cost manufacturer they should be supplying to most of the current retail players right? Who are the major clients?Wonder if they are supplying only basic designs (just a guess as they are highly automated). Also wonder how other “higher cost” manufacturers are surviving asRajesh Exportsthemselves have wafer thin margins.

Titan is being allowed to import gold directly. So, a lot of the advantage that REL had, will get wiped out by this move, according to me. Tanishq is a much more valuable brand, they know the retail market much better, extremely capable management and now lower input costs.

I was deliberately sleeping over Rajesh Exports:), to see where the odds lie for me.

1). The BS does add up, The Cash in FDs some 6400 Cr or so, comes out of the adept leveraging of supplier credits. Some 4 orders/shipments seem to be running concurrently.

2). The retail story - I visited some more stores with new “eyes” accompanying. The verdict was mixed. Fair to say, not everyone was excited or jumping at the 10% cheaper rates.

3). The Valuations are not so juicy - at the moment - esp. when you factor in past corporate misadventures. That one action of manipulating stock prices - puts a big question mark on Management Intent!!

4). We can wait and watch the Retail Expansion journey for a couple of more quarters, I felt. Also, there is some uncertainty on the Gold duties, excise, other policies, changes are being prescribed, etc.

However if the retail story gallops away Qtr by Qtr, I reserve the right to change my bias:). Needs close watching. Remember in 2007, the stock had galloped away, notwithstanding the ban by SEBI from markets from 2003-2006. Brokerages and Markets have a short memory. (Not one report in 2005-7 timeframes we saw, mentioned the corporate governance misadventures! Wonder why, These included PL, PPFAS, and more!)

Grand Opening of 20 New SHUBH Jewellers shorooms in the state of Karnataka on Akshaya Tritiya|24/04/12 12:20

Rajesh Exports Ltd has informed BSE regrding "Grand Opening of 20 New SHUBH Jewellers shorooms in the state of Karnataka on Akshaya Tritiya (April 24, 2012)"