Not to nit-pick but 3 months from Aug 17th would sustain only till mid November. That leaves around 1.5 months still left in Q3. Cannot ignore that period from the calculations given it is almost half a quarter.

Rain finacial year is from Jan to Dec

Can Aluminum industry not import CPC directly instead of relying on domestic CPC producers?

CPC is also a form of PET Coke. So as per the current update…they cannot import

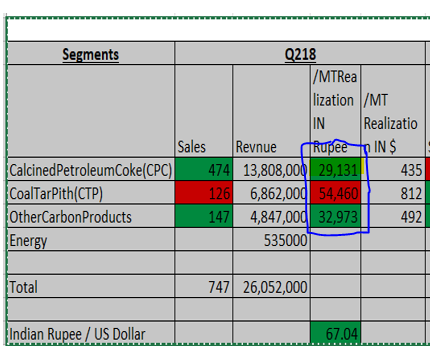

Hi Sunil, Thanks for the presentation, have a question on the following slide

Can you let me know how the MT realization for this quarter is calculated.

Thanks.

Divide the Revenue by Sales

13808000/474 = 29131 @ 67.04 $ rate works out to be 435$

https://aluminiuminsider.com/the-great-comeback-of-evs/

Interesting article

current projections say that by 2030 aluminium demand from EVs will reach 10 million tonnes, a ten-fold increase on 2017 figures. (Not considering construction sector demand)

CPC demand and aluminium production go hand-in-hand

Thanks

Ashit

Indian aluminium production should increase now with rising demand, but pet coke is banned in India.

Overall its a positive news.

1 Like

Dear Sunil…

a good logically analysed answer…

however what surprises me is why the market only picking Rain to hammer whereas none of this downside is sen in any other stocks…

i have this feeling is something else is cooking which we all do not know??

hope i am wrong

Discl: I am new to investing. I have very limited knowledge about investing and also about the industry Rain operates in. There might be mistakes in my write up. I have written this up to put my personal opinion about RAIN’s developements. I believe there is no new information present in this post, which is not already discussed in this forum. Invested & looking to add more. Corrections & Contra views are welcome.

CPC:

It has chinese competition in CPC who can not be taken for granted even during these pollution control crackdown times. That said the Indian chemical companies are commanding premium PEs as clients to Chinese companies are moving to India.

All their new investments in CPC are in india.

-> In the new CPC capacity coming up, they are using Chinese technology, which is vertical shaft (it seems it is literally equivalent to our old method of Oil extraction using rotating Ox) which uses less power consuming and produces denser CPC (this, I believe, might make it competitive to Chinese import prices). I guess this technology is still evolving, which might have caused the delay of 6 months in this CPC capacity expansion. This project is worth $65 mn (500 cr) for capacity of 0.37 mtpa. They keep 100$/ton margin in CPC. At its 80% capacity utilization, they can recover it in 4 yrs (300000 ton * 75 $ = $22.5 mln; Construction period + stabilization period considered for 1 yr).

[Google search yielded this: https://link.springer.com/chapter/10.1007%2F978-3-319-48160-9_157]

-> They are talking about MARPOL 2020 becoming an advantage to RAIN (if enforced), even though it eliminates huge amount of GPC out of global market, as RAIN can use lower quality GPC due to its Sulfur scrubbing technology. My another wild guess is, if Ships start using sulfur scrubbing to meet the 0.5 emission standard, it can sell its sulfur scrubbing patented technology.

-> It is widely predicted that due to MARPOL 2020, the Sour crude price would fall a lot. This benefits RAIN, by bringing down raw material prices for RAIN’s petro chemical business.

CTP:

The Steel, aluminium, chemcal manufacturing is shifting to low cost manufacturing destinations like India, china etc from Europe & US. This is bad for their CTP business in long run.

More than Rain, Its European & US competitors like Koppers might be finding it hard to survive, which is a positive thing.

Cement:

With 42 Cr investment (Change of technology), they are expanding the capacity to 2.79 mtpa from 2.03 mtpa.

7MW waste heat recovery plant construction is started which will be entirely used in house leading to power savings.

Chemicals:

I think lot of companies market their chemical under a brand name. But these revenues should fall between pure commodity to pure retail. They sell their chemicals under brand names: CARBORES, NOVARES & PETRORES,

Advanced Material:

They brought in a 30 years experienced guy from BASF, who worked in Electrical battery segment to head the Advanced material division. This shows management intent to focus on this sunrise sector which might enjoy long +ve cycle.

They are investing $65mln for Hydrogenated white water resins. According to management, there is good demand for these due to environmental regulations.

Other factors:

->They have recently completed (not sure how recent) functional integration of its various geographies using SAP, making it easier to manage and be more efficient.

-> Though temporary in nature, the Chinese winter shutdowns & pollution reduction measures would benefit reduction CPC exported out of China to India, middle east etc. Even temporary gains like these benefit RAIN as it has debt.

-> Partial amount of Aluminium capacity shifting to US due to tariffs, would benefit Rain in small way

-> Supreme court ruling (hanging knife) & stock trade restrictions are keeping the price low (my belief; can’t underestimate the supreme court though; occasionally they deliver irrational judgments) providing good buying opportunity.

Seems good overall. The valuations at 5.5 PE (though peak earnings; but does not include big depreciation) are still low. If aluminium cycle lasts another 4 or 5 yrs (if more aluminium in Aluminium in electric vehicle theme plays out), RAIN may turn out to be very good investment.

3 Likes

Thanks for posting such a fantastic report… for a layman like me…

regards

Hi,

I doubt ship’s will start installing sulphur scrubbbing tech. At present US , Europe region ship’s are burning low sulphur. Ship’s prefer expensive low sulphur bunker than scrubbing tech.

Reason

The regulation for ship’s are very strict in ports with heavy fine including loss of freight to owners, if they fail to comply the regulation.

Owner don’t rely on technology, if an option for expensive oil is available.

I am in shipping so got some fair idea of owner’s thinking.

Rgds

Prashant

1 Like

Discl: I have read only couple of article on MARPOL 2020 and have very very limited knowledge on sour & sweet crude dynamics.

Thanks for your opinion. I mentioned it precisely to invite expert opinions on MARPOL implications.

The author’s writing articles on MARPOL 2020 imply same opinion as you mentioned. Although, it is all market dynamics which will come into play. The sour crude price is kind of expected to go down as some of its demand would shift to gas, sweeter crude etc. When the price comes down significantly, people would find ways to use it (which has again the opposite effect of bringing the price back up to certain extant). One of the least likely scenario is, the ships would use the scrubber technology to use the cheap sour crude. I don’t know whether the scrubbing technology RAIN patented can be used for ships or not. Even though, it is least likely to happen, we can track this point of view, since its a massive opportunity, if ships adopt the technology use and RAIN’s technology can be used for this purpose.

Discl: Invested

Hello,

How did u calculate the intrinsic value to be 280 inr per share ?

ITAStompel.pdf (415.7 KB)

Presentation on the European coal tar scene, made earlier this month at the International Tar Association conference. Useful independent view on Rain’s CTP assets – especially it’s ability to offer a “full-package” of electrodes to the Aluminium industry.

Disc: Invested; views biased.

6 Likes

Rain Ind Q2 FY19 Shareholding.

Ace Investors have increased the stake from last Qtr. Mutual funds have decreased their holding

1 Like

Sorry , but i could not decipher who was increase the stake. Could you explicit state it ? Thanks for doing so.

Cloning is very dangerous unless you know your limitation and wealth to absorb short-term shock. Investors who invested by cloning Monish Pabrai at @400 level, have lost significant wealth unless he/she has stomach to absorb this bear market shock

Any latest update on following news story -

Goa Carbon says if SC doesn’t lift pet coke ban, it would be ‘disastrous’ for company ( I think it is disastrous for retail investors who bought at pick)

1 Like

Shareholding info is very important to ascertain the flow of smart money. IMHO, monitoring the investing styles of ace investors incl our VP stalwarts will enable you to expand your horizon to look for ideas which suits your investment style. If you see the past numbers (past is not an indicator for the future ) their mkt cap is less than two times of their EBIDTA , EV to EBIDTA ratio is less than 4.5.

I feel it is compelling to add at this level notwithstanding the bear market and market meltdown.

Discl: I am invested and look to add and hence my view is biased.

1 Like

Hearing is on Oct 9. While, we can not say what could be the outcome of judgement, we can clearly layout essence of the case. Petcoke is used as an alternate source of fuel (substituting coal) by companies, which is the real source of pollution. And precisely the reason for SC imposing a ban and above media articles.

Companies like Rain, Goa Carbon, Graphite, HEG etc use petcoke as feed stock and not as a fuel. Infact, Rain utilizes advance technology/processes which enables it to use low grade petcoke and does not cause any serious emissions.

And lastly, SC /GoI had already given clearance to GI/HEG to continue to use petcoke as feed stock. Rain uses petcoke to manufacture CPC, which inturn is used by Aluminum industry. So, on 9 Oct, a common hearing to allow companies like Rain. Goa and companies in steel/Aluminium sector to continue to use petcoke as feed stock will be held. Per my understanding and deducing from the previous verdicts, I expect a positive response. I may be wrong.

Disc- invested from lower levels.

2 Likes