I see the thread for this company stopped long back. I started following markets in the last 3 years and still consider myself a novice in this arena. Just putting my study over here, might help anyone.

First Lets Cover the Paper Sector, I have few points from CRISIL Research:

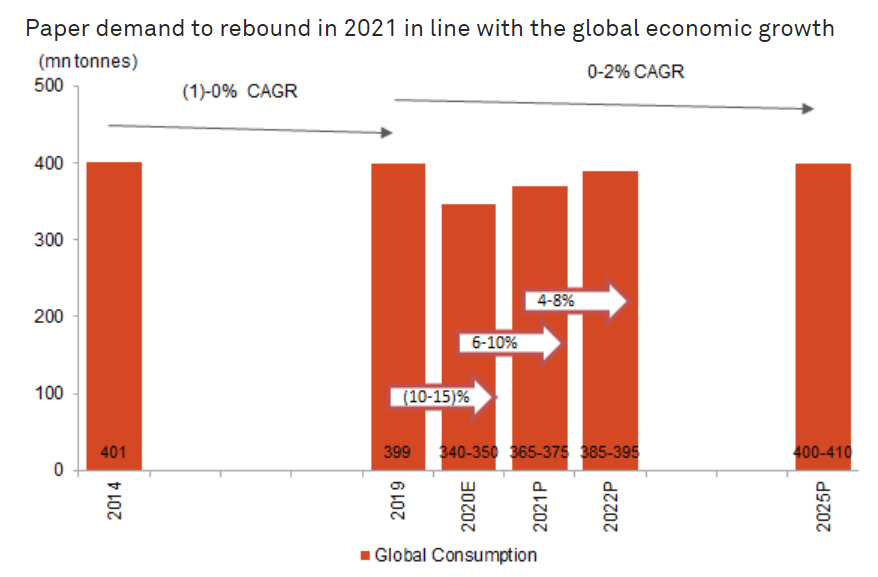

The Global Demand for the Paper & Paperboard industry is ~400 mn tonnes. from 2014 to 2019 Demand remained around 400mn tonnes for the paper industry and the demand is expected to stay flat at ~400 mn by 2025.

The Paper sector can be divided into 3 broad segments

- W&P (Writing & Printing Paper) (23%)

- NewsPrint (5%)

- Paperboards (72%)

Paperboards contribute to the majority of paper industry demand.

While the overall paper sector demand is expected to be remain muted for the next 5 years, each sector has different growth projections by CRISIL research.

Global Paperboards segment is expected to clock 3-5% cagr growth in the next 5 years, whereas the W&P paper and Newsprint segment are expected to degrow by (3-4%) CAGR and (8-9%) CAGR.

China is the largest consumer & producer of paperboards globally and has a 100mn tonne capacity.

Let’s talk about the Domestic paper industry:

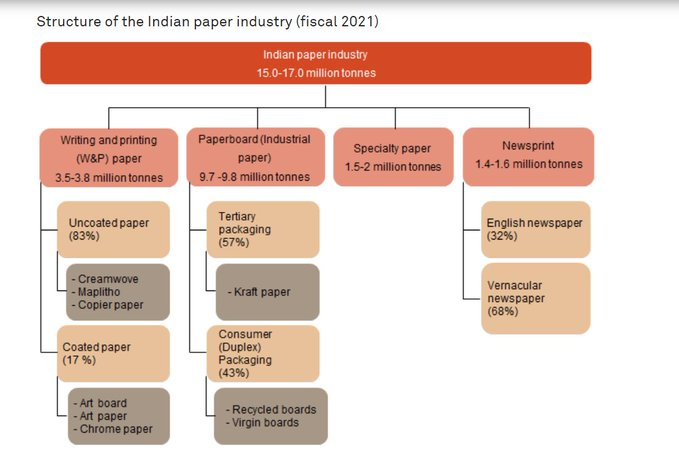

The domestic paper industry also has the same segments as global, paperboards can be further split into paperboards & specialty paper.

The below image from CRISIL research explains the broad split of the domestic paper industry

While the global demand is expected to remain muted, domestic paper demand is projected to clock 5.5% to 6.5% CAGR over the next 5 years and have an annual demand of 23-25 million, and demand for specialty paper is expected to grow by 10-12% CAGR. Demand for W&P and the newsprint segment is expected to remain flat in the next 5 years and the main reasons are a shift towards digital books, news apps than ever before. The paperboards segment is expected to continue growing on the back of healthy demand from the FMCG, Pharma & food delivery industry.

CASE STUDY: PUDUMJEE PAPER PRODUCTS LTD

PPPL is engaged in Specialty paper manufacturing and has expertise over 40 years in paper manufacturing. The company was initially created as an SPV in 2015 for merging it into the paper business of Pudumjee pulp and paper mills ltd, pudumjee industries ltd & pudumjee hygiene products ltd.

The company is currently operating under a lease agreement in the property owned by promoter group companies. The company operates from Theragoan Pune, where it has seen increased urbanization around the manufacturing plant and facing difficulties with increased compliances.

The company has invested in 80 acres in MIDC Mahad and plans to shift operations gradually over there. Due to Covid and uncertainty surrounding the demand, the company has shelved plans to shift operations to Mahad.

The Companies product portfolio consists of glassine & grease resistance papers, laminating base paper for flexible packaging, packaging tissues for precision engg components, and other tools. Decor paper for furniture and laminates. Fine papers for the bible, parchment for textile cones, papers for baking cakes, pharma packaging, paper for packing surgical instruments.

Hygiene products brand Greenlime has good recall value in luxury hotels, airports & corporate offices.

Things I like about the company:

- Company Operates in Specialty paper segment, which is the segment with niche products and good expected growth rate of 10-12% CAGR for the next 5 years.

- Company has been consistently improving the operating margins (though still less than listed peers like JK Paper, West Coast Paper Mills)

- Company trades at a valuation discount compared to peers

P/S ratio of peers (FY 21 sales)

Pudumjee 0.84

JK Paper 1.59

WestCoast Paper Mills 0.78

Seshasayee Paper 1.62

Emami Paper 0.99

P/E (TTM)

JK Paper 12.9

Seshasayee Paper 12

Emami paper 21

Pudumjee 5.8

FY21 had an exceptional item of 24.5 crores

- 71.2% Promoter Holding, No Promoter pledge & Promoter increased stake in last 3 quarters

Things I do not like about the company:

-

Company is heavily dependent on Raw material for its manufacturing, hence exposure to raw material price volatility and forex volatility

-

Power supply for the company is a huge concern as there is no co-generation facility for the company. The company has been obtaining power under open access scheme and group captive scheme which would cost lower than the power obtained through discoms. State electricity board imposed levies/tariffs on the company for using power through open access for the years 2016-2019 amounting to 33 crores of which 24.5 crores has been provisioned in 2021. There is still uncertainty about the power supply for the company and how the company would mitigate its power concerns

-

Company has been planning to move its entire operation to MIDC Mahad and expand capacity, which would require substantial Capex even though the company is expected to receive state govt incentives operating from Mahad.

-

The company was having significant ICD’s (Inter-corporate deposits) within promoter group companies, which is a red flag for me as it creates multiple transactions with related parties and is difficult to determine if the transaction has been done at arm’s length. ( forensic accounting experts on the forum can help here)

Rating:

My Overall opinion would be that company is poised to have a decent growth of 10% for the next 5 years as the sector it operates in is expected to grow at 10%. capacity utilization is improving and margins are improving consistently for the company. The company also has a very low debt-to-equity ratio. The company also has a good credit rating of - CRISIL A-/Stable by Crisil.

Link to Crisil rating report

So at this price, I find this company a decent buy in this buoyed market. the company shifting operations to Mahad, expanding capacity, and resolving its power supply would be the next triggers for the company. But more related party transactions in the future would be a red flag again.

Thanks for reading!!.

Would come up with more study about the whole sector and other good companies in the sector. I am happy to stay corrected if anything is incorrect in the above reading.

Disclaimer: I am invested in the company and this is only for educational purposes. I am not a SEBI registered investment advisor. Do your due diligence before you buy the stock. Microcap investments are illiquid and sometimes exit is not easy. Consult an investment advisor before you buy.

.