please explain contingent liabilities more than 800 crores? were are they exposed to? Source of information?

1 Like

I am just looking at their balance sheet in screenr

As far as I know I don’t know if they have any serious contingent liability

Except any lawsuits by sdp

Or if any legal agreement with the existing customer for compensation incase of non completion of project

1 Like

Good time to add the stock right? Have added some in today’s 10% fall.

Operating margins are not lower than this for them historically. Also PE is super reasonable. I can only upside from here on both earnings and PE going ahead.

Heard that the stock is down due to some big exit today. Views from others on this?

2 Likes

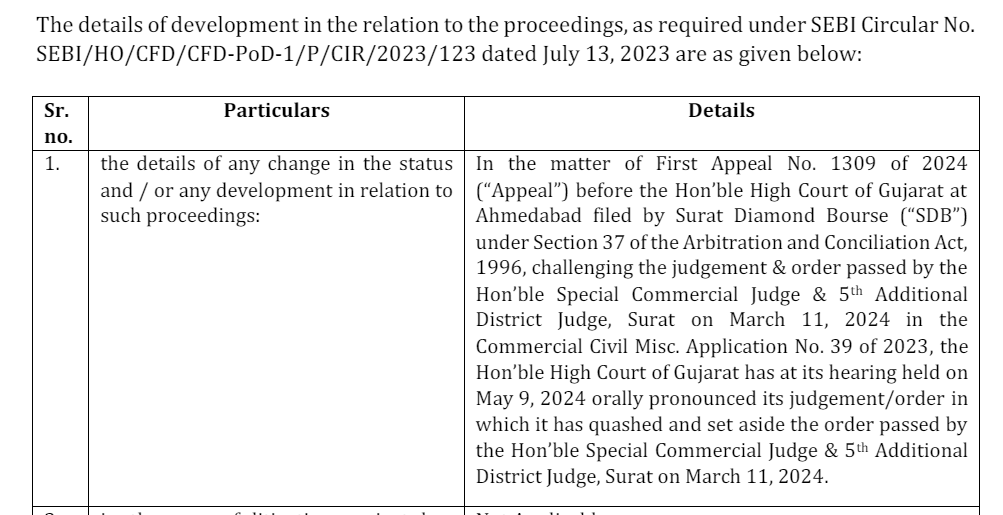

I think there is also overhang of ongoing disupute with Surat Diamond Bourse.There claim is approx Rs 530 Cr. and litigation is going on. so, the working capital of company is stretched and in case SDB dispute settelement is delayed , they may go for QIP. But, these disputes are part of business and in my opinion long term prospects of company is good.

Disclosure: Invested and no transaction in last 30 days

3 Likes

Value research article on PSP projects

https://www.valueresearchonline.com/stories/201137/psp-projects-hidden-gem-or-value-trap

Disc: Invested

2 Likes

Can someone throw light on these statistics I got from comparing annual report of March 2018 with March 2023.

PS Patel’s compensation was 4.09 Cr as March 2018 and went up to 15.6 Cr as of March 2023. (Yet to get the latest figures). During the same time, the companies net profit went up from 42Cr to 133Cr. PS Patel’s compensation has improved 4x whereas the PAT has grown 3x. Ratio wise, the comp is > 10% of the PAT (even though < 10 % of EBIDTA) Is this desirable?

Few thoughts:

-

Even after factoring in delayed revenue from projects such as SDB, why is the board giving so generous compensation to one individual?

-

When the PAT fell ~20% YOY (FY '22 to FY '23), PS Patel’s compensation was seen rising from 14.8 Cr to 15.6 Cr for the same timeframe. Isn’t compensation linked to performance? What is in it for shareholders?

-

From what I know, PS patel does not offer shares to employees. How can this organisation sustain from this one man army. This does not sound well.

Please help me understand if this is par for the course? These certainly don’t seem like a good situation.

1 Like

No stock becomes multi-bagger by adding 5-10 Cr to the annual bottom line by cutting CEO’s salary.

What matters to me is that the company has done 3X net profit in 5 years. If PS Patel can deliver 4X in next 5 years, shareholders might be happy to further compensate him.

However, if you are bringing in inequality angle between him and his employees, then it begs a different discussion and different forum. Also, I believe ESOPs should be offered to select employees, who are key for company’s success and to retain them.

Thanks,

You are right that we need to reward merit. That being said I became a bit skeptical looking the growth of PAT and growth in comp. Shouldn’t performance be linked to PAT ?

On my other point though I am not worried about inequality but rather the incentives for others to perform.

to me it looks positive, as I wrote earlier, I was expecting 100Cr only

In the November call, they only cited ~100Cr of receivables for booked, unbooked, and retention money. Even in a recent call, I heard a similar figure; what is the 400Cr amount? According to my understanding, it is using a price increase provision following a force majeure to negotiate 100+ crore. I see the focus is largely on recovering ~100 crore.

disclosure: invested

1 Like