Are these premco numbers real ? It’s a local auditor and no one in this business makes these kind of margins -

Just asking so that we invert and think of what can go wrong.

Are these premco numbers real ? It’s a local auditor and no one in this business makes these kind of margins -

Just asking so that we invert and think of what can go wrong.

is hdfc bank their banker? if so gives comfort.BTW HDFC bank was interested in investing in 2 textile cos sometime back.Sarla Perf fibres and Premco.In Sarla they took stake but in Premco owners own direct n indirectly nearly 70% stake after increasing it substantially in recent years.HDFC bank would have done some home work n wud hv the confidence in nos n promoters.

If some hanky panky happens promoters will be the biggest losers,the co is constantly reducing its debt,Co has very long relationship with almost all reputed OEMs,Co has a dynamic new ED WITH a global vision and education .Vietnam expansion is v logical as its the textile capital of the world…

Lets all plan to attend AGM and prepare the list of queries.Lokesh harjani had v patiently answered all the queries from bosco due to which i had invested in range of 160-230.at times cos open their mouth in AGM only. no instt/hni ownership so far in this yet undiscovered co .journey is starting imho.

HDFC is mentioned as a banker - but we don’t know if is a borrowing bank. It could be a deposits bank for the company. None of the credit rating agencies cover the company.

When is the AGM and where

it shud b in mumbai date n AR not yet out

Vivek

Have been looking into this stock since its illquid Rs.90 price band

Just wanted ur views on how do you forsee Premco’s business vis-a-vis Arrow textile.

Both seem to have some common clientele…

Regards

Have not tracked Arrow Coated Sreekanth.

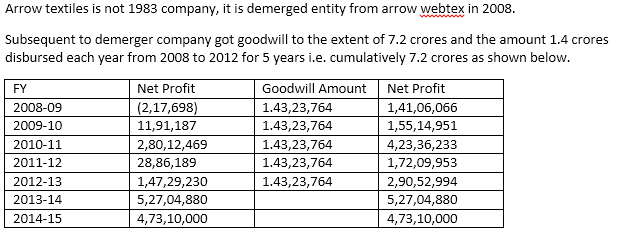

wow - that was helpful. Arrow textiles looks like an orphaned step child of jaydev mody of delta corp fame. Numbers look a notch below premco’s at 25 % EBITDA margin and about Rs. 60 cr. in terms of size - they are also growing well but not as fast as premco

I plan to talk to them to understand what they are doing and how they view premco - at 9 x PE, their valuation is also on par with premco.

I am attaching a doc that is on their website - the one big difference is on ROCE where premco’s is at 32 and arrow’s is at 14-15 %. That’s ridiculously large - so either premco is sweating its assets exceptionally well or these look large because of the historical asset values of premco and hence, may not sustain going forward whenever they add in new capacity, which should be in the not too distant future

This has been a concern I have always had - premco is a 50 year old company and I am sure their assets are at 60’s and 70s cost of real estate/machinery. What will incremental ROCE be once this asset gets maxed out ?

premco is generating Rs. 72 cr. of revenues with a net block of Rs. 13 cr. whereas arrow is generating Rs. 47 Cr. with a net block of Rs. 20 Cr.

premco was founded in 1966 whereas arrow was started in 1983 - that’s a two decade gap

neither of them have added too much to their net block over the last 5 years - hardly 10-15 % growth.

any counter views ? @ayushmit, @Vivek_6954, @rohitbalakrish_ ?

.arrow textiles.doc (203.5 KB)

Karan,

The MCA Site indicate charge being registered only in favour of HDFC Bank. While there is no certainity of credit being provided by HDFC, it is sure that sanction has been done by HDFC Bank.

http://www.mca.gov.in/DCAPortalWeb/dca/ViewIndexOfChargesAction.do.

Also, please refer to page Page 21 of FY14 annual report. It clearly mention that the company have taken term loan form HDFC Bank.

Hope this satisfy your concern.

Hi Varadharajan,

Arrow textile’s business is different from Premco’s. The former is into manufacturing of labels while the later is into elastics.

Arrow also seems to be doing well. Earlier their nos were subdued as they were writing off the goodwill. Now that the same is over since an year or so…the current numbers portray a better picture.

Ayush

Think Premco used to manufacture labels. They stopped it some years ago.

Now its being manufactured by another group company

Mr. Varasdharajan,

Premco global appreciated from 190 to 408 with in hardly one year. Is there any margin of safety for buying this stock at this price?

It got recently recommended by forbes. In Forbes list of 200 stock below a billion. there were 11 indian Companies

Avanti

Borosil

Byke

Caplin

Centum

Kaveri

Kitex

Ngl fine chem

Vakrangee

Premco

Latest shareholding pattern. Interesting to observe that Sonia Ashok Harjani bought 1845 shares which were not appearing March 31 2015 promoters holding. Also, in my search on BSE, I could not find any disclosure about purchase by Ms Sonia. Can anyone through some light whether the promoter can purchase share and does not inform stock exchange? Also, whether my search is correct or I missed the disclosure on BSE?

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=e3675a3f-44e3-4d58-9434-4da9d26b2819

Senior members, at this price of 590, is there some value in this counter ?

My first post - hope to be constructive. A few points to add:

Inventory has increased substantially: The sanctions on Premco might have led to a pile-up of finished goods inventory of Hanes. Or, to take advantage of low crude and rubber prices (lowest since 2009), perhaps this could be a stock up of requisite raw materials in 1H15 (inventory as of 1H15 was 9cr versus 15cr as of end-FY15). My bet would be on the former. Receivables have decreased YoY - perhaps as collections from Hanes continue while no further dispatches were made circa 2H15. This seems to also explain lower YoY sales (Hanes being their largest customer by far). Does this oversimplistic logic seem to fit in ?

Disclosure regarding Vietnam facility reveals an interesting point: From the filing made to BSE on 19-May-2015,

Quote

The Company thrives on Export to Vietnam, the Export grew from 28 Crore to 38 Crore in Vietnam.

Unquote

It is instructive to note that the Annual Report mentions FOB Value of Exports as 37cr in FY14 and 25cr in FY13, implying that almost all exports are made to Vietnam.

If the newly created capacity in Vietnam would cater exclusively to Hanes (as it seems from the same filing), it could mean that utilization in the India plants would drop considerably in the near future ?

There were preferential allotments of 1,50,000 shares each in FY13 and FY14 towards the promoter family, diluting the voting rights of the minority shareholders. This is poor corporate governance.

The excellent economics have been mentioned ad nauseum, and I believe that Premco Global operates in an industry (innerwear) which does not face obsolescence, is a necessity, and needs replenishment on a continual basis. Whether the pricing is elastic (no pun intended), is arguable.

Additional uses like luggage straps, shoelaces, car seat belts, etc would grow, albeit cyclically. Even if Pixel Packaging represents all of the “Others” in “Sales and Services”, the INR 25 Lakh revenue contribution does not justify the capitalized emphasis in the description used within the website.

The economics of the Vietnam facility and utilization of Indian operations thereon would be key factors to watch out for. Look forward to more commentary on the same.

Disclosure: I own shares of said stock.

The bet is also on dynamic new ED since 2011 Mr Lokesh Harjani

1)Who is in his 40s the right age for any CEO in pink of his health n full of growth mindset

2)He is the catalyst behind all positive changes

3)He is patent holder in US who had his education in US which included law

4)He is taciturn ,speaks only at AGM sign of an ethical promoter focused on his business n execution

5) Being US citzen with US upbringing n accent he brings a new horizon <Corp Governance and a big comfort to his mostly American customers

6) In small co 80% bet is on promoter only.Big opp size n 45% ROCE is just an icing on the cake for a still microcap co with huge opp size staring at it ^

Vivek

I think the ROCE is very mis leading since most of their assets are held at 60’s cost - when the company was founded. what will be interesting is to observe incremental roce’s from vietnam facility.

Then again, issues like no CFO, no one except promoters signing off on the numbers, so so auditor and a hardly impressive board are not great signs.

if lokesh had a growth mindset, he would also professionalize the organization - look at the AR - there is no one earning Rs. 10 lakhs p.a. in the company - that;s not a good sign for the future.

discl: invested, and a 4 x - so not a story of sour grapes.

This keeps on hitting UC everyday

It seems market is anticipating another fantastic quarter ?

Any views on Q1 result expectation on 11th Aug ?