Hi all,

Great to see the discussion on Premco Global. I had looked at this company sometime back, and had invested small amounts (Due to a lack of complete conviction). Most of what I had researched has been covered beautifully here by posters. A few things, which I can add:

Does the company have pricing power?:

It certainly does, but : a) Not to a 1:1 extent b) With a time lag (I presume the contracts must be fixed for 3-6 months and renegotiated thereafter). Certainly shows reasonable bargaining power, which is critical when you are dealing with giants.

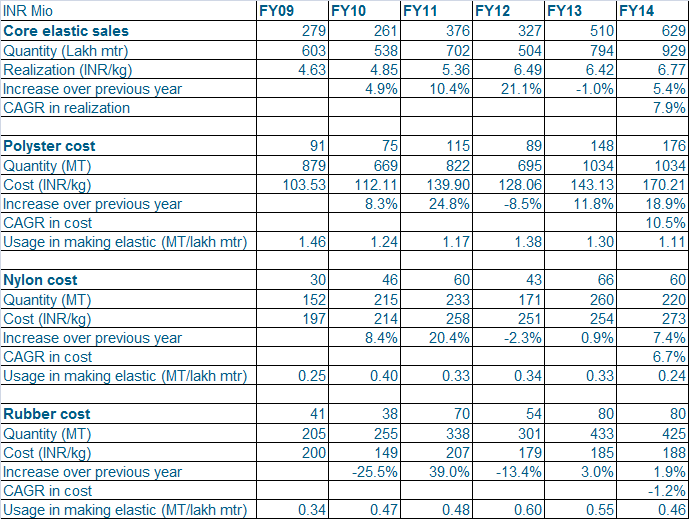

If you look at last 6 years, polyster (which forms more than 50% of RM costs) has increased at a CAGR of 10.5%, where realizations have only increased at a CAGR of 7.9%. Here is the data to back it up:

So whats driving margins and return ratios?:

Clearly, pricing power is not enough for increasing margins (realizations have increased at the same rate as raw material prices). So whats driving margins?

-

From the above data, it seems that the company might be moving towards more efficient production. For example, for every lakh meter of elastic produced, the company was using 1.46 MT of polyster in FY09, a figure which came down to 1.11 MT in FY14. This implies either better machines being used, or lesser wastages due to better processes being implemented or a change in product mix

-

Other expenses, including electricity and processing coming down. This clearly points to more efficient processes/machinery in place.

-

Better absorption of fixed charges like admin expenses due to higher sales turnover

Clearly, this has happened with a graduation of the next generation of management into the company (as has been established in this thread already). In textile business, management plays a more important role than most other businesses (Hence, you find most textile companies in the hands of families and less of professionalism). In this regards, I think its important to get some sense from the management on what processes/machines have been implemented to improve efficiencies in the production processes.

That was something I could not establish, and hence the lower conviction.

). Also, its because of these reasons (spinners/weavers/processors have very low bargaining power), and the importance of judging management, it is difficult to invest in spinning/weaving/processing companies (which do not have brands) with true conviction.

). Also, its because of these reasons (spinners/weavers/processors have very low bargaining power), and the importance of judging management, it is difficult to invest in spinning/weaving/processing companies (which do not have brands) with true conviction.