I think Premco started the plant in Vietnam because its main customer Hanes and a lot of other textile co’s set up a plant there. These textile companies set up their plan because of the competitive labour costs and also in anticipation of the pact.( for the duty benefit )

Now since Hanes already has an operational plant in Vietnam and since the labour costs are competitive , i dont see much of an issue for Premco

Also as per the article Vietnam has signed several two-way free trade agreements with several other countries which should help Hanes (i guess)

Also Premco with its new manufacturing facility in Vietnam is only catering to a certain percentage of Hanes requirement. So even if Hanes does not increase capacity because of the scrapping of the TPP , Premco would not need to downsize.

This is my understanding.

Premco in previous annual general management did said that plant of Hanes more due to cost competitive ness of Vietnam then only TPP. Even TPP was under discussion, Hanes plant was already operational. TPP would have reduced cost of import from Vietnam for Hanes. Hence, there would not be any impact on Capex plant of Premco Global. Only if Hanes decide to downsize Vietnam operations and move to another market, then only Premco may consider not to invest in Phase II of expansion. Phase I of expansion is already complete and started supplying the material to the clients. In my opinion, TPP or No TPP, Vietnam facility of Hanes would continue to operate and hence no impact on Premco Global Vietnam operations.

Please refer to my note after AGM 2016 which cover TPP point and management view on same.

Without TPP, it will be tough for any textile manufacturer in Vietnam to compete, especially in the USA market. Contrary to popular belief, Vietnam is no longer very competitive. Wage rate there is already more than India and growing in excess of 20% p.a due to acute shortage of labour (roughly only 90 million population). If TPP doesnt come, I see a big opportunity for manufacturers in India, Bangladesh and Pakistan, its possible a lot of trade migration from China to Vietnam will now come to these countries. I think its worthwhile monitoring results of the Vietnam plant, there may be more challenges than we are expecting.

here we are missing one point. whatever amount invested by premco is not that big for company. 10 cr even if company writes of is just one year earning for company.

main point is very low equity and floating stock in mkt. slightest improvement in earning can bring fantastic effects

click below links they also have recommended the PREMCO

I read somewhere but can’t recall now where, that Hanes and many others, as it’s quite obvious, established their base in Vietnam in anticipation of benefits to be accrued due to TPP and now with Trump that to be gone IMO Hanes & others with bases in Vietnam stand to lose that advantage which may negatively affect their suppliers like Premco as well.

IMO, net net, without TPP Premco stands to lose and this is not at all positive development for the co.

Hanes already has an operational plant in Vietnam.

So how will Premco stand to lose? Unless ofcourse Hanes downsize their operation or close their plant , both of which seems unlikely. These points have been discussed in the above posts…

Corporate governance is always a key concern while investing in small companies. But even with red flags, some companies have gone on to become multibaggers.

And the next trigger for the stock is revenue generation from the new plant.

From Money Life magazine:

Promoter helping themselves to loans?

Premco Global is a company manufacturing narrow fabric, including elastic and non elastic ribbons, straps, bands and packing tapes used in inner wear, packaging, sports, medical, furnishing and the automotive industry.

Premco’s focus is on exports and a new plant in Vietnam which can give it an edge. There are a lot of positives going for the stock. However, the annual report discloses strikingly large ‘related party transactions’.

The long term borrowings for 2016 were just Rs. 92.82 lakhs and the short term borrowings were 293.76 lakhs. In sharp contrast, loans given out to related parties total 1281.75 lakhs in 2016 (promoter and his family).

The interest paid by the related parties on loans taken amounts to Rs. 67.5 lakhs, that is, 5.2% on the total loans of Rs. 1,281.75 lakhs taken by them. The interest at 5% is low and should be a red flag for investors.

We also looked at the percentage increase in the remuneration of related parties and found that promoter compensation has jumped last year. Premco has created enormous value for shareholders and may continue to do well business wise. But these practices are not fair on minority shareholders. The company needs to keep related-party transactions to the minimum, if not nil, if it has to get much higher valuation multiples.

these loans were not there for entire year and hence moneylife is not right in assuming interest is 5%. year end loans to RPTs is negligible. It is not known when loans were advanced and when repaid. Moreover, these may not be concurrent to the three RPTs.

Loans have been given by the promoters to the company. Not the other way around. The title is misleading. Please find snapshot from Page 80 of Annual report:

Loans have been taken by the company from the related parties and repaid them as well, as closing balance is nil. This indicates promoters are infusing short term funds to take care of working capital requirements, and company is repaying them back, both of which are positive.

Always making closing balance nil may be construed as “cleaning” up the balance sheet for year end, but is not a severe red flag in my view. But because closing balance is nil, the company need not have disclosed these transactions at all. This is an additional disclosure, which should be appreciated. In fact, promoters should not be taking any interest of the funds advanced by them. But if the amount of interest paid is small, it indicates either of 2 things - either that interest rate charged by them is low, or that the funds are given to the company for really short periods, and interest is calculated only for that time.

The observation regarding salary paid to promoters is valid. It increased from 1.08cr to 1.81 cr - ie 9% to 14.6% of net profit, and is open to debate.

At times, even good reporter make some error. While concern of Moneylife of high growth of promoter salary is valid, in my opinion, the promoter has another infinte way to get money from business and salary is the most honest way the promoter can take money, as any money as salary would attract 33% pay (with promoter getting into higher tax bracket). So, level of salary growth is debatable, but I personally like when promoter take salary as same is subject to higher income tax at promoter end and also give genuineness of earning of business.

Secondly, whole argument about favourable terms to promoters by the company, turns 180 degree when actually it is loan extended by the promoter to Premco. So in a way, Premco has gain by favourable terms from promoter, but no way one can consider that promoter has gain from company. It is actually Premco which has taken loan from promoter and paid interest to the promoter. The valid concern on this point shall be why shall company pay interest on loan to promoter when It has larege investment in Mutual funds, which I had presonally raised in 2016 AGM. Please refer to my note about AGM on same thread. Vinay has clarify the point in detail in discussion.

I have put forward my comments even on Moneylife thread about some error at their end. Find enclosed link for same.

Not sure whether all members would be able to view the link and comment, as I am subscriber to the magazine, I am representing my comments on this article on moneylife magazine website. Other members may give their view, particularly in case of any factual error.

“Comment 1: Please check the content. I believe, these are loan given by director to the company. The word is loan taken from the company perspective. While point on Director remuneration is valid, still same is subject to tax and shall be link to profit.

Comment 2: In August 2015, the company management was specifically asked about loan taken from promoter group and they give explanation that same was done to provide working capital to fulfill the large order reeived by the company during FY15. During FY16 also promoter extended loan to the company and interest is actually paid by the company to promoter and not received by the company as suggested in Article in my opinion. I hold this stock and has attended past two AGM. I would request you to check and confirm.

Comment 3: Refer to Note 22 (Other income schedule) in Annual report of FY16. Total interest income earned is Rs 4.35 Lakhs during FY16 and Rs 2.76 lakhs during FY15. While the interest paid figure in above article is Rs 67.44 Lakhs. So if the related party paid Rs 67.44 Lakhs as interest on loan taken from the company, how come Interest income is only 4 Lakhs? Interest cost for the company is around Rs 85.64 Lakhs during FY16 (Note 26 in FY16 AR) which is higher than Rs 67.44 Lakhs interest paid to related party.”

Disclosure: I hold share of the company and hence my view may be biased. An investor shall do its own due diligence before investing in the company.

Trump withdraws from Trans-Pacific Partnership. Trump’s decision not to join the Trans-Pacific Partnership (TPP) came as little surprise. During his election campaign he railed against international trade deals, blaming them for job losses and focusing anger in the industrial heartland.

So Trump walks the talk and If he continues doing the same, could be a big disruptor. Can’t underestimate him. Though this is a positive and welcome development for home grown textiles companies esp. home textiles pack which is already having good time.

Disc: No Investment in Premco. Invested in Home Textiles companies.

While TPP implementation would have been good for Hanes (hence in turn for Premco) due to lower custom duty on exports from Vietnam to US, personally I do not see major issue as far as Premco concern. In case TPP would have implemented, the major gain would have been for Hanes and not sure whether same would have been passed on to the Premco. Hanes already have operational plant in Vietnam of large scale. Further, while TPP was one consideration, it was not the only factor for Hanes to set up plant in Vietnam. Real consideration in my view were reducing dependence on China Sourcing and lower labour cost with potential of benefit for TPP.

With TPP going, Hanes would have to consider other competitive manufacturing place. Despite all favours from president, US is unlikely to be least cost garment production hub for Hanes, at least in next 3-5 years. Hence, Hanes would contniue to manufacture from Vietnam and so business as usual for Premco, in my opinion.

Discl: I have investment in the company and my views may be biased.

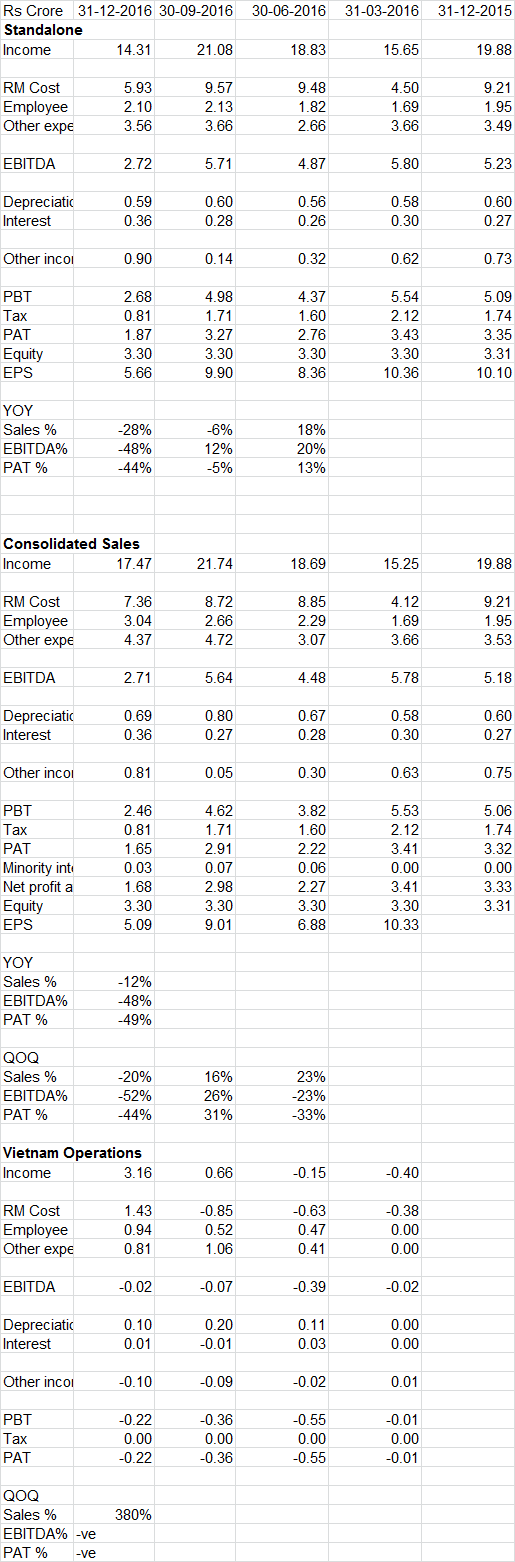

Poor Q3 numbers from Premco.

Consolidated revenue down 13% YOY… Profit almost 50% down.

Standalone sales down 25% YOY and profit down 35% YOY… It seems demonetisation has taken a severe hit on its top line. But bottom line Degrowth is a huge question to answer.

Employee expense 50% up YOY.

COGS has also gone up.

The results are bad. The standalone decline in topline with Vietnam plant operational, indicate that the company is not utilise capacity which have been servicing Vietnam demand previously or realisation are in pressure. We need to understand whether this decline is temperory (due to lower industrial actitity in domestic market) or structural. The company need to look at full utilisation of capacity. My assumption is that the company has not reduce selling price.

The raw material cost indicate significant increase in production (reflected in increased inventory of Rs 2.01 Cr during December 2016 quarter). Due to this fact, I assume that the company has not been able to market the capacity which was release from Vietnam plant operation and also suffected negative impact of operating leverage

Increase in non-operational income is in line with December 2015 quarters. Although same have given major boost to profit during the quarter as Other income/PBT is around 34% during December 2016 quarter vis 14% during December 2015 quarter.

I have assumed Difference between Consolidated financials and standalone financials as Vietnam operations. Only positive I take from December quarter is spurt in Vietnam sales from Rs 0.66 Cr in Sep 2016 quarter to Rs 3.16 Cr in December 2016 quarter. Further, employee cost also jumped from Rs 0.52 Cr during Sep 2016 to Rs 0.94 Cr.

While results are bad, I feel Vietnam increased activity shall be good for long term of the company.

Disclosure: I have investment in the company and my view may be biased. An investor shall do its own analysis before making any investment decision.