Worse part is the attitude of the PE firm Rabo Bank - When asked for comment on the audit, Rabo Equity managing director Rajesh Srivastava said: “No special issue for us as it relates to all minority shareholders.”

A good lesson learned for me is to completely stay away from companies having PE stake. They are short term oriented and care only for their exit irrespective whether the company is drowned in debt or does fraud or goes belly up in the future. As a big shareholder if they cannot keep the promoter in check then what can us minority shareholders do. PNB Housing finance is another such company where carlyle is a big shareholder - IPO price was around 1000/- and now its 360/-

Anyways I am stuck with part of my holding and let’s see how the forensic audit goes through. Hope the promoters of Prabhat are severely punished by SEBI for delaying sharing the proceeds and reducing value by booking fictitious losses, high transaction charges etc. My reading of the promoter was completely wrong and all their justification of sharing the proceeds in a tax efficient way, bringing independent shareholders to board, keeping the proceeds in escrow, multiple stock exchange filings re-iterating their intent to share the proceeds etc was a complete hogwash.

Had requested Moneylife to do an article on Prabhat and had given my inputs, they have come up with a good article - https://www.moneylife.in/article/sebi-hauls-up-prabhat-dairy-for-not-co-operating-with-forensic-auditor/61854.html

Good action taken by SEBI

Very detailed order given by SEBI - https://www.bseindia.com/xml-data/corpfiling/AttachLive/dd3a6793-3c8d-41f0-8897-c6752eee413c.pdf

It starts by listing down the history of the case, the company’s multiple filings to distribute the proceeds to shareholders. SEBI started looking into this issue on Sept 23,2019. (Note - Company did not inform this to the exchanges. SEBI should have directed company inform the exchanges) Out of 1700 cr, 1316 cr was received. After indemnity provisions of 204 cr and transaction cost,tax figure of 234 cr, a figure of 854cr which has grown to 872 cr due to interest is given by the promoters. SEBI asked both BSE and NSE to look into this and both concluded on the need for forensic audit. One good thing from the order is that institutional investors also have complained to SEBI. The escrow account money was transferred out and it’s not clear where it moved.

Based on the promoters conduct in not sharing any information with the forensic audtior, SEBI has directed to deposit 1292 crore (which is the balance sale amount after repayment of debt and advisor fees) in 7 days. Also they are to furnish all the documents asked by the auditor in 7 days.

If we go by promoter’s numbers and assume 872 cr is available. Assuming 50% is paid out to public shareholders since public shareholding is approx 50%, we get minimum delisting price of Rs 88/-

If we do this for 1292 cr, assuming 50% is paid out, then price comes to Rs 131/- Of course this includes waiting opportunity cost and we don’t know if it will happen, forget about when it happens. But good to see SEBI being pro-active in this case so far.

Hi,

I have been following this case with interest from a distance. When I was a fund manager at a PMS firm earlier, I had once set up a meeting with the MD, and then when I was about to travel from my office at Nariman Point in Mumbai to faraway Navi Mumbai (where the MD was supposed to meet) on the day of the meeting, he canceled at the last minute citing some non-sensical reason. After that, he didn’t even bother to set it up again with me. This is when I was a fund-manager at a large enough firm for a company of this size and when we had reached out through a personal connect and had his direct mobile number.

Fortunately having spent enough time with Indian promoters in my decade-plus buy-side experience, this behavior was a major deal-breaker and I never bothered to take a serious look into it although I track the branded foods sector with a lot of interest.

Given this background, it was fun reading the entire 31 pages of the SEBI order last night. I am not surprised that even GT which is the forensic auditor appointed by SEBI is not able to reach the promoters mostly and most of the queries which were asked on 17th July 2020 have been unanswered even now. Equally surprising was that the company tried to delay the appointment of the forensic auditor itself citing some random conflict of interest issue which has been well explained in the report.

And @bhaskarjain I think you may have missed the biggest and the most revealing part of the order on Page 23 of the order which is as below:

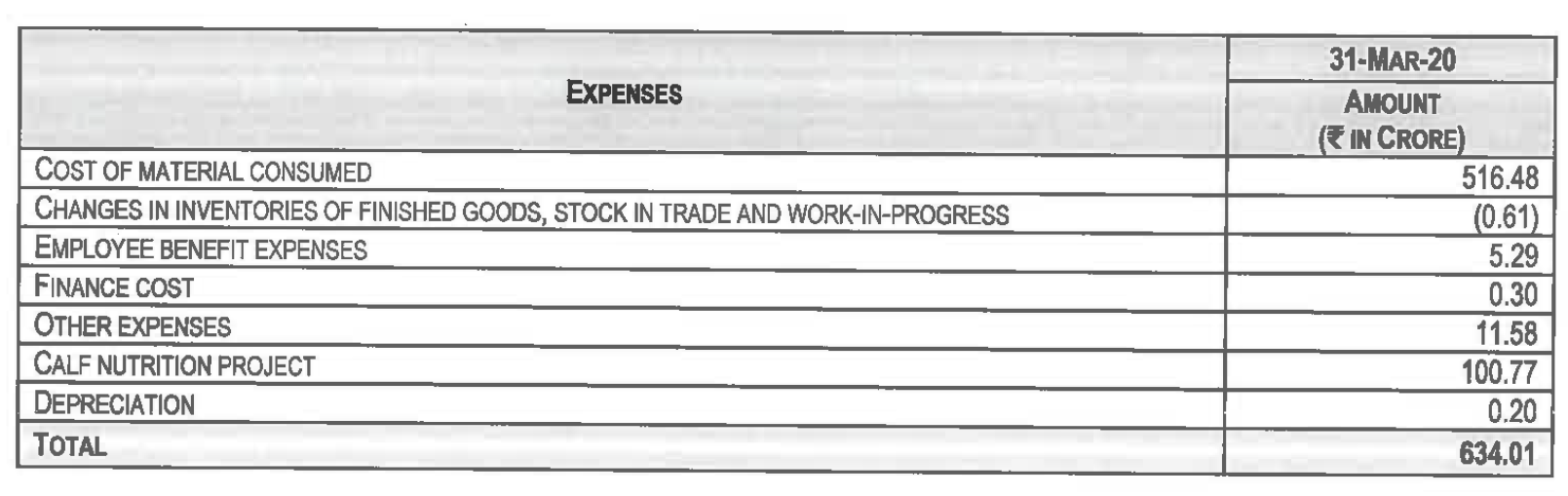

While the audited numbers are not surprisingly not yet done (citing Covid conveniently by the promoters) and GT has said in the report that they are unable to ascertain if cash from the sale has been used for the cattle feed business, I suspect most of the cash is already siphoned off. I do not understand how else the company would have funded 634 cr of expenses if not by the 872 cr which was supposedly left for the shareholders. Since the sale happened in FY19 itself with the transaction amount being received on April 10th, 2019 I do not what explains the cost of material consumed of more than 500 crores in FY20!!

Hence, it remains to be seen that even the 872 cr (which is far less than the gross amount received by the company to the tune of 1880 cr originally received by the company) can be paid and by when. Litigations between SEBI and company promoters will also happen, regardless of the final outcome.

Overall, it is not worth the headache to deal with such companies and promoters. If someone has it in small quantities then it may make sense to hold in the hope of some strict action by SEBI. But overall this remains more of a hope trade than dependent on sound analysis as there are too many unknowns and even the timelines are too uncertain. Nevertheless, this case creates a fresh understanding of the behavior of some promoters which is very useful IMHO.

As an after thought I feel strict laws should be made by SEBI for Indian Listed companies wherein companies should be mandated to distribute 100% of net amount received as buybacks/dividends/delisting within 6 months if more than 75% of the entities business by market value is sold. The allowable expenses for the transaction should also have a ceiling. This is the only way promoters will not shortchange minority investors. I had following similar delisting of Claris Lifesciences where in the end promoters ended up delisting the company at 400 per share even though the company was sold at more than 600 Rs per share - in their case they even had the guts to declare a 300 crore bonus for the employees as part of transaction expenses!!

All the best,

Sarvesh Gupta

PS - I run my own investment advisory firm. Views are personal.

Thanks Sarvesh. Agree with you completely that it’s a hope trade because outcome and timeline both are unknowns. What makes this case unique compared to LEEL and others in my opinion is in this case they went ahead with exchange filings that max proceeds will be distributed, won’t be diverted to any other business etc. I think they tried to play smart and are now caught in their own game.

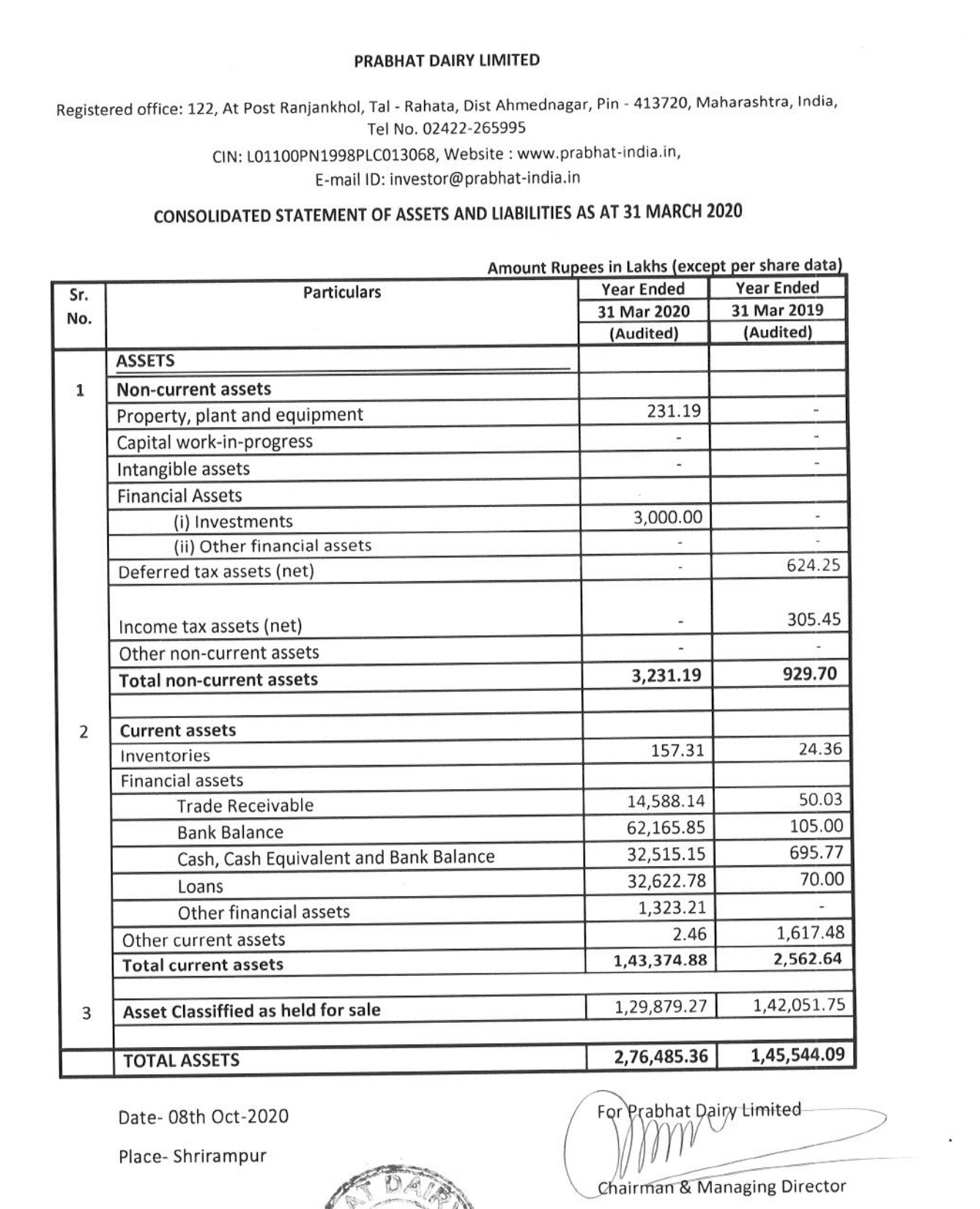

In the audited results for the year 2019-2020, they are showing some 946 cr as cash & bank balance in the consolidated results.

Company is going to SAT against the SEBI order. No end to their crookedness. After SAT, only option is SC and likely will be taken up to keep on delaying.

The SAT has passed their final order on this case on 9th November, 2020. It is available through the Company Website or their BSE / NSE page.

While I may sound optimistic, it seems to me that one too many cases of impropriety in the cases of delisting in the very recent past (LEEL, Vedanta et al) has finally broken the Camel’s (SEBI’s) back. Their action and reactions to the Promoters highhandedness in this case have been swift and objective - to the point of being overdone, as the SAT order noted.

Case in point - the Promoters Bank Accounts and Demat Accounts have actually been attached by SEBI. That is way more than the customary “slap on the wrist” which we are used to in India. This is some seriously medieval stuff. Someone at SEBI has made this personal

In any case, the SAT - much more reasonably and calmly - has given the Promoters till the 19th November, 2020 to both deposit a more reasonable INR 500Cr in an Escrow account (that is about INR 100 per minority shareholder - a figure which, by the way, the Promoters have stated in front of the Tribunal they are willing to pay). Plus this is also the deadline for the Company to submit all the required financials to the Forensic Auditor. Their accounts will continue to remain attached unless they do.

Further, very defined timelines for the Delisting proposal vetting (to SEBI) and the Forensic Report (to Grant Thornton) have also been given.

Could the Promoters appeal yet again in the Supreme Court - I am not a Lawyer but it seems reasonably certain that they could. That would push things along for at least a few quarters. Even if they don’t - could they continue playing the fool through the Delisting process and cause delays. Of course they could.

But as an Investor, one must think in terms of probabilities and not just possibilities. Sooner than later, the reward seems to be at least INR 100 per share - that is a 53% upside.

If they do deposit the amount on the 19th - a week from now - then the game is all but over.

SEBI is out for blood this time around - and all things being considered, as an Investor this does seem like a tasty, tasty “Special Situation” Bet.

Get in touch if anyone finds out anything more.

Mohit Kumra

shrimohitkumra@gmail.com

Promoters have deposited the 500 crs in an escrow as instructed by SAT. Raises the probability of this getting to a share price of 100 quite significantly

They already declared INR 100 / share in court.

Standard negotiation tactics dictate that they understand that this is the lowest price they can get away with.

Now depending on who gets up to fight with them, the final price to end this sordid mess will be determined.

There is one “TVS Capital” who requested to be an Intervener in the SAT Hearing - claiming that they represented 30% of the Share Capital. They are not on the list of Shareholders to I am guessing that they represent the Big-3 (Vistara ITCL, India Agri, Societe de Promotion who collectively hold 30%).

So now it is essentially a negotiation on how much they can get on top of the INR 100 between these two. We can only watch.

Important Question : How much would you get out at in the secondary market in the short term itself taking into account “Cost of Carry” while this whole thing gets sorted out

Mohit Kumra

@mokumra - Good question. In my mind I think this should atleast get close to 100 in the short term. If u want to be safe I think thats a good price to exit.

If u buy at 71- current price- that still gives a potential 40% upside.

SEBI was also directed by SAT to process the delisting application within six weeks from the order date (09/11/20). So betting on this special situation has some fixed timeline. I think SAT was taking a view that delisting, transfer of sale proceeds and forensic investigations are all separate issues and can happen concurrently and need not block each other.

What I don’t understand is the company claiming in SAT that they have offered shareholders Rs 100/- which SEBI is not taking into account. When and where did the company declare Rs 100/- offer price to the shareholders ??

In any case, the appellants have offered to its shareholders Rs.100/ per share which comes

to Rs.490/ crore which fact has not been taken into consideration by the respondents. Thus, in our view the direction to deposit a sum of Rs. 1292.46 crore is patently erroneous and cannot be sustained.

I am sure that they cannot offer it “officially” - must be something they said in Court maybe to TVS Capital.

The fact of the matter is that they have said it in Open Court and it is noted in the Order - now they cannot offer anything below that.

I think this will end up at the IPO Price of INR 120 - no calculations…it’ll be a price anchored in everyone’s mind.

The Voluntary Delisting offer is finally here!

Things will move fast now. The game pretty much ends on 5th April, 2021.

I think that the Promoters will offer a generous price given that they are under scrutiny by multiple agencies - and that will only go away once the delisting happens.

I say - close to INR 140…INR 100 is already lying in cash, plus the remaining for PPE / going concern etc. Just a rough, subjective guess.

It just depends on the 3 big shareholders holding about 30% of the public shareholding.

Mohit

Please note this extract from Letter of Offer.

At the indicative price of ~ Rs 100, promoters will have to pay Rs 391 crores to acquire the minimum quantity of shares for delisting. They can always reject any price above the indicative price. So the question to ask is about the seriousness of delisting intent…

vh1,

My two cents :

-

30% plus of the remaining holding is with three major shareholders. I doubt they will agree at INR 100.

-

The Promoters would be very, very keen to get this delisting through for the following reasons -

a) INR 100 will as it is have to be distributed even if delisting does not go through to the Shareholders as they pledged to pay the receipts of their sale proceeds (which is this amount and already kept in an Escrow account on the orders of the SAT). So that is just their opening offer, the base price they are willing to offer. They will obviously be prepared to pay more.

b) If they don’t delist - and at a decent price - all of their shady transactions will be back in the limelight. And it is obvious that there has been some hanky-panky. The big shareholders will make sure that this happens. And I don’t think the Promoters would want that.

I have a strong feeling that the Promoters will want to dig themselves out of this hole they have dug themselves in and delisting is the only way out.

In any case, I am just speculating, but I am pretty sure that the Promoters and the 3 Major Shareholders may have already reached an agreement on the final price. And I will be very surprised if it is INR 100.

Mohit

Update on delisting.

Company has announced that delisting offer is successful. The exit price is Rs 101.

Promoters’ stake (current) = 50.1%

Minimum additional shares required for delisting (to reach 90% stake) = 3,89,72,934

Shares to be acquired by promoters after offer=4,42,83,727

Post the offer, promoters’ stake will increase to 95.44%

This means promoters will spend about Rs 447 crores for the additional stake for delisting

and get control of all cash and assets of the company.

Payment to successful bidders is expected on 06-Apr-21. Return of shares pertaining to rejected bids by 09-Apr-21.