DIVI MURALI and ADITYA PURI are some of names that come to my mind when i think of level 5 leadeship based on what i have read

3 Likes

This is for how many years?

Problem with these big three, as I see and have heard from ICICI wealth bank reps, is that they dont lend in small quantities; their loan books are hollow. They prefer to lend to institutions which is not in single digit crores; something akin to, now defunct, KFA loans. A simple search shows ADAG, Adani group and others have enormous debts, which they continue to kick (the can) down the road, and these big three continue to assist them by not calling their loans nor placing them under NPA. Who else will lend to these big-wig companies other than these institutions; our bond market is still in nappy-stage.

These three are too-big-to-fail and in any eventuality, they will be bailed-out and we (tax payers) will bail-in.

Yes, it may sound like speculation, but they are no saints either, till 12 months ago, they had no NPA and suddenly they have an ‘akshaya patra’ of bad assets.

3 Likes

Talking about 25% CAGR portfolios -need some feedback from esteemed members. As we speak when the market has sharply corrected how many of you have portfolios which has appreciated 25% or more in the last 2 years as of Nov 2016. I am trying to get a sense of my own portfolio which is flat YOY and also in the last two years due to the recent correction. Need some motivation

Old Stocks:

Pidilite

Asian Paints

Colgate- Palmolive

Hot Stocks:

Prozone Intu Properties

Delta Corp

Advani Hotels

Next few Stocks?:

Fiberweb

Ludlow Jute

Vivimed Labs

IFB Agro

Talwalkars

3 Likes

That was Jan 2016. Time to revisit this exercise, once again :), right?

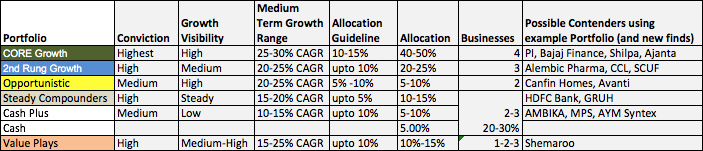

Last time round, we had focused on

A. Growth Visibility (also using the very tangible EPA measure) to develop conviction on holding onto the Winners in a Portfolio

B. Replacing a few who don’t measure up and finding couple of new candidates to restructure the above Portfolio for a more well-balanced, more resilient should we say quest for that elusive “All-Weather” Portfolio

I worked out something that helps me think in a more structured way about Portfolio Risks - and how to do something about it - and so even though it’s not a finished job - am making bold to present something that’s still work-in-progress, so don’t kill me for it ![]() .

.

Inviting folks to help me take the discussion forward - folks having the same quest - probably folks with Concentrated Portfolios?

16 Likes

Sir

Can you please share latest all wearher portfolio. Is it same as posted?

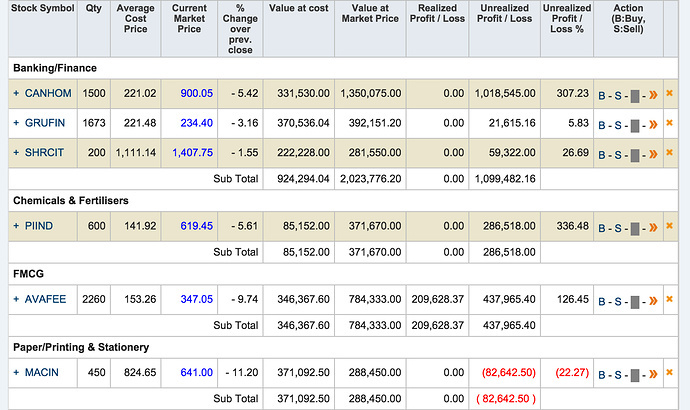

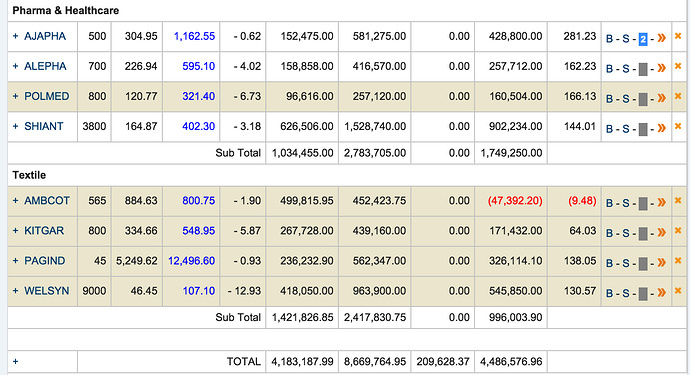

A casual look at the above Example Portfolio - and comparing current valuations versus Jan 2016 - would have told us that the Example Portfolio wouldn’t have done too badly. Most have rebounded handsomely - indicating resilience. And one or two had not, even underperformed!

However we were meant to restructure for more solidity, right?

Didn’t find it easy to get friends to discuss restructuring Concentrated Portfolios in a structured manner. So I had just gone ahead and worked out something that appealed to me and implemented something similar for me in phases - first in Feb 2016, and again in late Oct/Nov 2016.

Would be glad to see if this resonates with some of you concentrated folks!

As we can see some new names were added - CCL Products, Shemaroo, and HDFC Bank.

Names that dropped out - Kitex, Polymed (diluted goals/next level for business), Page Industries (growth inconsistency)

And we can also see some clear attempts at Categorisation - to force us to think more clearly about how we/Mr Market perceive such businesses.

Now for the all important rationale ![]()

18 Likes

The Rationale?

1.Remain convinced - in the very uncertain global economy and India’s unique growth positioning (medium to long term  ) - and the fact that our markets are mostly driven by FII money - Indian Markets will continue to have its mood swings - flashes of big optimism, consolidation, and pessimism - on a regular basis.

) - and the fact that our markets are mostly driven by FII money - Indian Markets will continue to have its mood swings - flashes of big optimism, consolidation, and pessimism - on a regular basis.

2.We have watched varying reactions from friends we respect - in their bid to handle the same. Some went to 40-50% CASH as early as Oct 2015. And they were hailed as genius in Jan/Feb 2016 after the 3 month mayhem. From Mar 2016 onwards, when the Markets started rebounding, many of these friends were left sitting out, and most haven’t been able to get in, most of them have missed some big gains in the interim. Again the jury is split!

3.We have also seen some other friends we respect - remain fully invested, all through. Some of them did a few odd switches, but mostly rued the fact that being fully invested, they couldn’t take advantage of some bargains they would have taken real advantage of - if they had CASH !!

Mr D had instilled this early in us - (instructive to go back and check the 2011 Capital Allocation thread) - We must have at least 20% CASH in ALL STAGES of the Market. Otherwise we will NOT be able to take advantage of the bargains that Mr Market offers - every year - sometimes, 2-3 times a year !!

Those who have followed the Capital Allocation discussion then with some thoroughness - might remember the discussion around the Opportunistic bets - that allowed us to be in some sort of quasi-cash all the time - since being opportunistic bets, we wouldn’t mind trading some/all of that in for a CORE bargain!!

Think it is the same robust underlying philosophy of holding/handing quasi-cash that sort of morphed in 2-3 additional avatars - Steady Compounders, Cash Plus, Cash.

What does that do? It allows us 2 things:

- Greater flexibility to remain (almost) fully invested

- Take full advantage of REAL BARGAINS, when we KNOW them (prior or new homework)

Sure, we sacrifice some of that core growth possibility, for the sake of more STABILITY. Why is that?

- because inherently quasi-cash candidates - perception (valuations) are mostly in-line with performance - steady or subdued, as the case may be

19 Likes

Some more explainatory Notes - exposing my Assumptions behind the Structuring.

Over to you guys. Views invited !

Just 1 Caveat - for better perspective.

A well-diversified portfolio with over 25-30 businesses has much more resilience in-built for carrying “apparent” non-performers (where Earnings Quality and BS remains pristine, even as Growth may be flattish!) for longer periods of time.

A Concentrated portfolio - the style that suits me - with 10-15 businesses at most - has much less space/luxury to carry such “apparent” non-performers - may not be more than a couple at any point of time? Gotta be more ruthless there!

17 Likes

Why Can fin is bracketed in Opportunistic box.At least in the medium term (3 years) -I guess it should deliver 25% CAGR.

Hi Donald

What is cash plus means. Easily convertible to cash without losses.When bargains are available in the market like Nov 16 everything goes down so how cash plus scrips will save us.Your thoughts pls.

2 Likes

@Peabody

We had defined “Opportunistic” bets - as essentially mispriced bets, that stood a very good chance of a 50% upside in 6-9 months. Accent was much on Undervaluation, than on Conviction.

Which meant once the performance-perception gap got nullified you should start booking profits - unless the business kept upping in Conviction - i.e. consistent noticeable improvements in performance - kept making the case for a higher slot for the business

- so we had businesses like Avanti Feeds, Atul Auto, Oriental Carbon, Canfin in those slots.

Re: Canfin specifically

Think most of our friends slotted Canfin as opportunistic - and probably still do that today - Of late consistency in maintaining/upping performance has been great, but perhaps is not taken for granted - jockey continuance related, and doubts on pervasiveness of systems & process culture needed. So despite growth and good metrics - it is probably not slotted in the same league as other growers in portfolio

To be seen in context of medium to longer term outlook in a Concentrated portfolio. Maybe slotted differently in a well-diversified Portfolio

2 Likes

@Peabody

There you got me

Life cannot be that simple right!

The idea is of course as you said - greater ability to switch in market turmoil with “lesser” losses than other vaunted hands.

So it must have couple of essentials for Downside Protection

-

Undemanding Valuations vis-a-vis our Quality slotting

Central thought here is that valuations must be undemanding - actual operating performance though must be ahead of perception - with little signs of growth reverting in a hurry - Perhaps 4 quarters away - that is the primary reason for undemanding Valuations?? (Not iffy quality) -

Think we must also consider high dividend payout/yield also acting as a floor - as a better measure of downside protection. To that extent, MPS may be a fitting candidate too, including that back in.

Guess the key thought here is - we choose from among businesses wherein we have tremendous respect for the Management - achievement/turnaround from where they started in what timeframe. So we factor in that current flattish trajectory is temporary consolidation - while there is absence of real noticeable growth, “earnings quality” and BS are actually pristine and improving. We trust the Management to work things out on some fronts. So we should give a longer rope

That is really the thought process there. Mr Market may not always agree to that and may end up hammering these equally - but obviously there will be nuances we can learn from - and improve the selections - over time - for more (logical) resilience.

2 Likes

Hey Donald, It more skewed towards BFSI and Pharma, any particular reason !!!

Opportunity Size, long Runways versus current scale (so we can continue to hold through if they continue to execute), Demonstrated Track record, and more importantly our own close familiarity/information-analysis edge with such business/Mgmt over last 5 years are the probable reasons. Each one is a bottoms-up pick. Not any Sectoral top-down preference, for sure.

Specific choices reflect more on individual experience/and FEEL for next-level for the business. This is only a Live-Example Portfolio to spur constructive action!

We are pretty sure, there are other equally good (probably better) candidates hiding out there - especially in Value plays. That is the constructive take-forward from this exercise - while urging/influencing everyone to make more-informed, thought-through choices.

As always I have exposed my thought-process and assumptions behind the exercise. Waiting to see others do the same. That is the “secret” for Team progress !!

3 Likes

Just sharing some thoughts as felt the need to emphasize the importance of FLOOR in such purchases.

I follow this strategy as I am unable to hold cash and prefer being fully invested. During corrections I take out some money from these kind of stocks (even if it means booking a minor loss) to invest in something else that I find better and has corrected more as compared to my this holding.

Most important thing I find here is to have some sort of an idea as to what is the FLOOR. Good valuations in isolation need not always be the best indicator of a floor in such cases, as such stocks (without dividend yield protection) can always correct more due to growth being few quarters away. Hence one needs to ideally try to buy it near the floor so that when market corrects this one corrects relatively less (or doesn’t correct ideally ![]() ).

).

How does one identify that floor may depend upon each individual (one can only try as market hai and one never knows ![]() ). Some might purely do it on the basis of valuation, some might bring in technicals in it. I don’t know much about technicals and hence try to buy a stock which has stayed at a particular level for a long time or keeps bouncing back from that level or even if goes down from that level then goes down for a very short time and attains the level back very quickly (one might call this as technicals itself

). Some might purely do it on the basis of valuation, some might bring in technicals in it. I don’t know much about technicals and hence try to buy a stock which has stayed at a particular level for a long time or keeps bouncing back from that level or even if goes down from that level then goes down for a very short time and attains the level back very quickly (one might call this as technicals itself ![]() )

)

For similar reasons like above, I had started buying Camlin Fine Sciences at 83-84 and also started buying AYM Syntex from 77-78 levels (this was majorly 'coz it corrected from already decent valuation levels due to Welspun issue), although I expected Camlin to go up first. And divested some amount of both (with minor profits in Camlin and minor loss in AYM) to start building position in couple of other names.

Cheers.

4 Likes

As you exited some of earlier stockso, which are the stock which got replaced in your portfolio

What are the replaced stocks against you exited from your portfolio

@Donald sir, there seems to be no FMCG stock in your portfolio. With Indian middle class expected to be around 400 million families strong, each having higher disposable income and increasing urge for consumption. This will be a huge opportunity - one of the examples of value migration in my view - with lower income group moving towards higher income group with higher income to spend. (a crude analogy will be - if one considers this set of families as one company, then higher disposable income will mean high FCF for the company ;)). So with this in mind, should not be there couple of FMCG stocks - HUL, Marico, ITC (largely moving to FMCG now), Nestle etc in portfolio? Agreed some of them are richly priced - but if one is patient, Mr Market gives enough opportunities to stock them. Pls let us know your thoughts