In May 2023, The Promoter Group Members agreed to sell approx 24.2778% of their stake to AGP Holdco Limited (Investor) and informed that they were in the course to obtain necessary regulatory approvals. AGP Group is Dubai based Group and have several businesses including Packaging.

The consideration has been revised downwards to Rs 1,188.9 crore, compared with Rs 1,379.47 crore announced in May.

The September Shareholding pattern publshed shows that the Promoters have pledged 100% so a vital question arises how will they sell 24.3% if they have pledged full100% ?

Having read through the thread, I see there is no serious discussion on the pledge by the promoters. If fellow boarders following this company can throw some light on the pledge issue.

Just entered this stock today based on two factors. Firstly, there are indications of a reversal on price chart, suggesting that the bottom has been reached. Secondly, a new investor from Dubai recently purchased a stake at a price of approximately 1500/share. This implies that they see value in the company and may have some revival plans in mind.

Pledge is in favor of AGP Holdco (Alghurair group, UAE) who will eventually become the promoter of the company. This is part of agreement between the 2 parties that Sanjay Shroff will not sell his stake without approval of AGP.

This is not a financial pledge, hence, investors should not consider this as an issue.

Promoter Sanjeev Saraf (founder of Urdu poetry platform Rekhta) had been trying to sell the company for last 2yrs as next generation is not interested. Dubai based AL Ghurair group is buying into the company in a 2 part deal, 25% now at 1,600/share and balance via call/put option over next 3 years.

Al Ghurair group owns Taghleef industries which has BOPP capacity (500k TPA) similar to the size of Polyplex (435k TPA)

CEO of the group will soon come on board of Polyplex

I think this is a special situation, where the company could get a boost from new promoter/management.

There is also the opportunity for enhanced distribution network if Polyplex can leverage AGPs distribution network.

Disc: Have a tracking position.

Edit: Promoter name is Sanjiv Saraf, had typed Sanjay Shroff erroneously.

I can’t find any track record of polyplex conducting earnings call. Will lookout for earnings call for peers like Jindal Poly, Cosmo First, Uflex & Ester - in case they can guide about BOPET industry margins going ahead.

Recently looked at the company and below are my first impressions.

The company has short term debt of 383cr and receivables of 882cr. The long term debt is 216Cr and investments are worth 230 Cr. Based on these I am guessing the debt position is pretty comfortable.

The cash available is 935Cr. Mcap is approx. 2700Cr. taking the difference the business is available for approx 1800Cr. Assuming that the FY24 sales will be 6000Cr, thats 0.3x P/S. That seems to be very cheap.

Further, the pain of lower realizations can persist for another year or 2, cant say for sure though, but in any case the current levels of OPMs are on the lower side compared to 10yr history.

Additionally, stake sale by promoter took place recently at around 1500/share, so anyone buying now is entering at much lower price, so that could also be a comforting factor.

So, there is a change in ownership in the offing, reversal of margins after couple of years is a good possibility, the share price can further correct for sometime which gives the buyer time to accumulate slowly and monitor the performance of the industry and company. Lastly there is some value left in terms of the valuation of the Thai subsidiary, but that also would keep going down as long as the pain in the industry continues, so not ascribing any value there.

Overall, looks like a value buy, and will demand lots of patience.

This company is in a cyclical industry. Money is made by investing while PE is high, margins are low and selling when PE is low and margins are high.

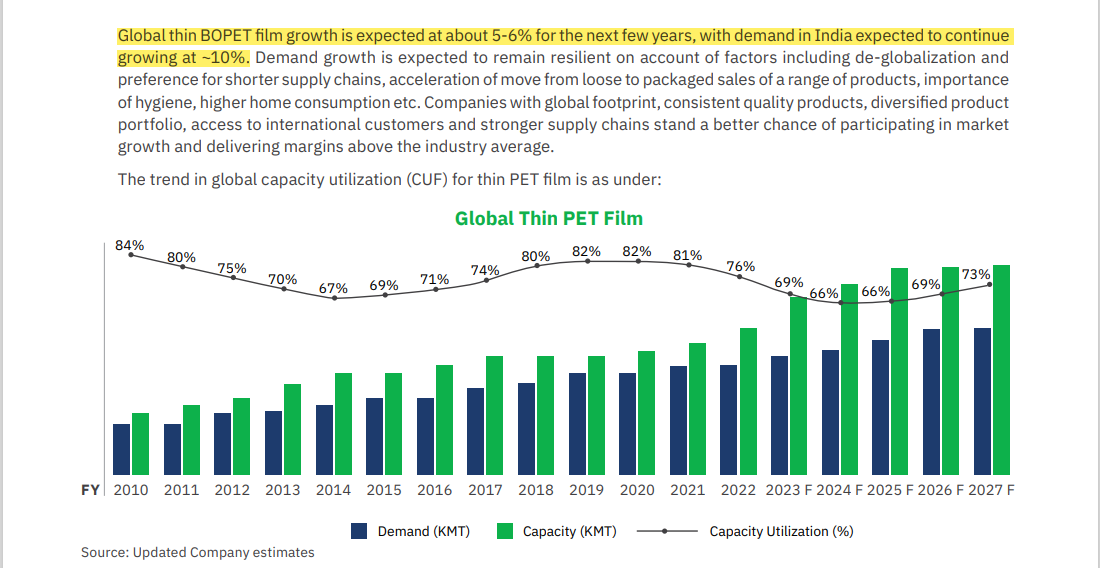

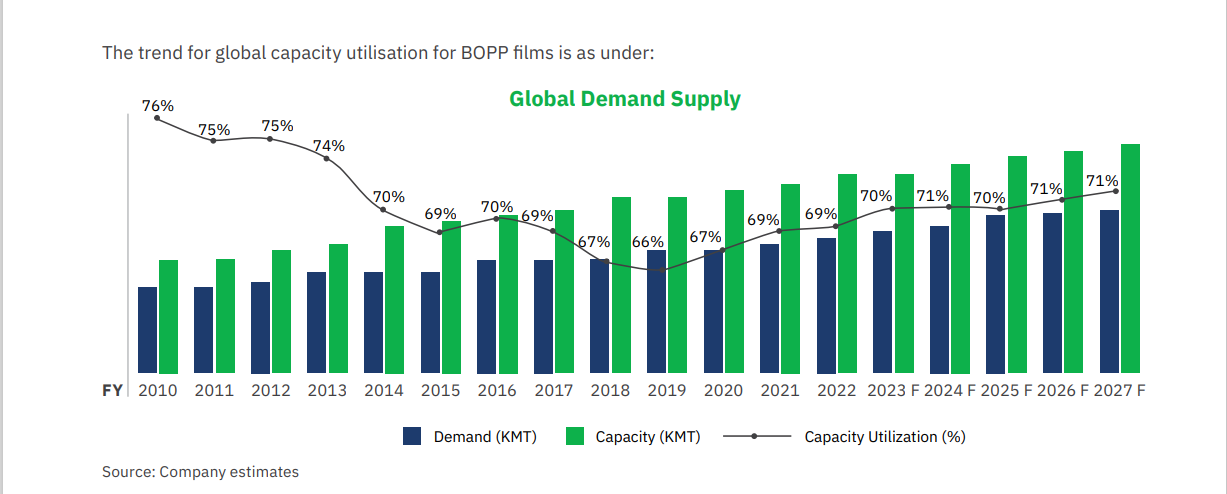

Dec 23 OPM is 3%, TTM OPM is 5%, where as at the peak of the cycle it was 25%. Did some basic google searches - Based on an article in TOI in Dec 22, in FY25 there will be an oversupply of both BOPP and BOPET. BOPP capacity would be 1300KT against demand of 1075KT. BOPET capacity would be 1200KT against demand of 940 KT.

Assuming above data is correct, there will be pain for another 4-8 quarters, however with most companies starting to report ~80% reduction or negative PAT, it will be interesting to see if companies will put the expansion on hold, or might run in to financial issues. If that were to happen, well run companies will be set for next up cycle.

The only thing that concerns (could be a gap in my understanding) is why does the company historically pay dividends even when it had significant borrowings and capex planned. Even last year it had a 80% payout ratio.

Also historically the company always has had a high cash balance thus should we already discount for that?

If we see the balance sheet, the cash has always been more than the debt…so we can say that its has been net debt free. From the cash flow we see that except for 2013 and 2014…the company has generated free cash flow.

For promoters, dividends is a way to take home some money from their business. Not saying whether it is right or wrong, prudent or not, but thats the reality. The company historically has not generated any great RoCE as such.

")