I think quartz was not sold because of heavy duty. CVD 83%, final hearing on that in feb.

2 Likes

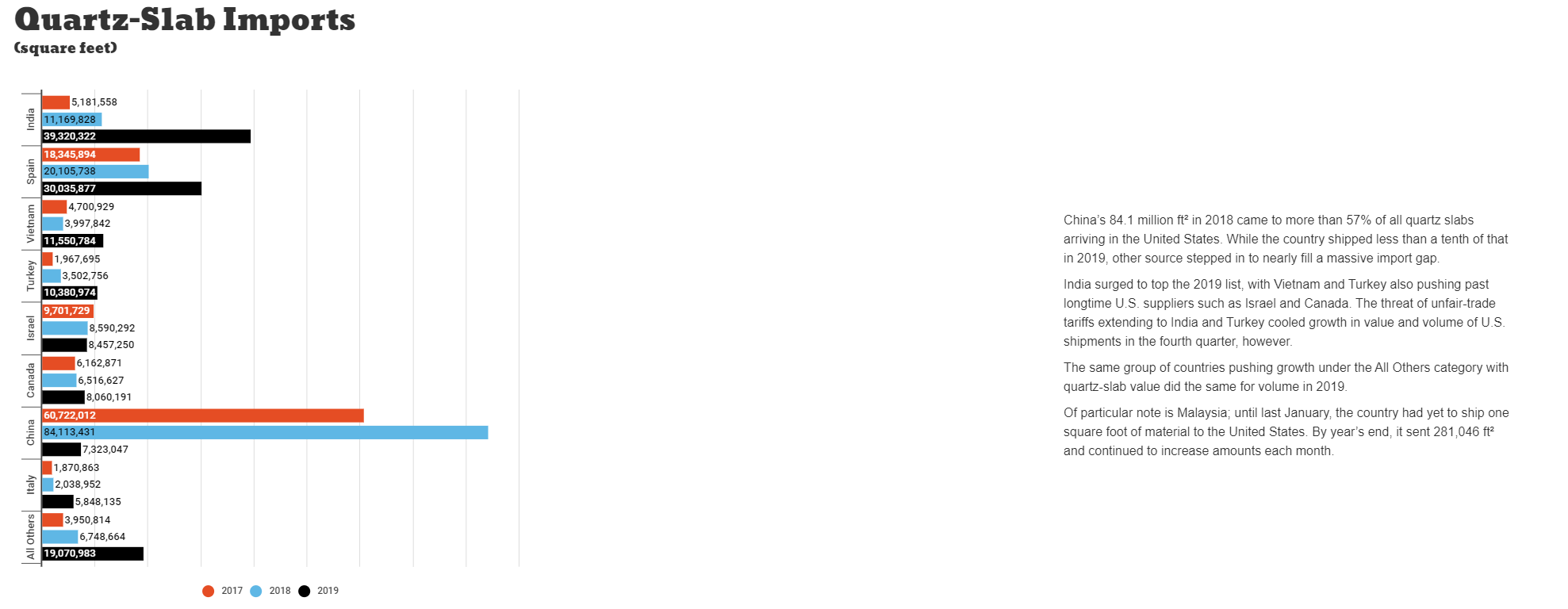

Anyone have country wise revenue breakup?

1 Like

What does this mean for pokarna?

It means that they can appeal after the investigation is done; not now.

2 Likes

2 Likes

1 Like

So the ~80% duty put in Nov 2019 is now reduced to 2%, is that correct? If so, it is a big positive for the company.

2 Likes

I think it has not been finalised. This is what they have written in the pdf :

This means that QSP from PESL will have combined AD/CVD cash deposit rate of 2.67%.

The definitive imposition of these duties is still subject to a final ruling by the US

International Trade Commission (ITC). ITC ruling is expected on or by June 11, 2020.

Yes. So I guess we have to wait till June to know the status.

Entered again yesterday. Hopefully this time the determination of ADD and CVD have no “ministerial errors”!

1 Like

As per the article for Pokarna AD : 2.67% and CVD : 2.34% so around 5% in total . Pls let me know if this is a correct understanding.

Also what is the difference between DOC Final Determinations and ITC Final Determination. Can the % drastically increase as only the DOC determinations have come for now

As per my understanding DOC makes all calculations for determination of duties and recommends to USITC. USITC is responsible to determine whether theres a material injury to domestic industry or not. Theoretically speaking, duties can change until the final hearing is over but what to expect practically is anyone’s call.

USDOC seems to have finally agreed with you ![]()

This is the growth of quartz import in dollar terms for India and China in US.

2017 2018 2019

India 4 7 24

Chi 46 58 5

crores USD

In terms of dollar value, the biggest beneficiary was in fact spain which might be because of its premium products. However. in terms of volume, India was the major beneficiary.

source : http://magazine.stonemag.com/2019-us-hard-surface-imports-report/2019-quartz-slabs/

Few things to note :

- Pokarna was running at 100% utilization for quartz for significant part of the year. Now, 130% new capacity has come online. As it was noted in court arguments, many importers have strategic long term partnerships with Pokarna.

- In last quarter of 2019, the imports had slowed down because of proposed duties.

- On the negative side, the overall import did not see any net reduction for the year which means that countries other than China filled out the gap. I don’t know if India has cost/quality advantage wrt other countries. If slowdown because of COVID is significant and overall imports fall significantly then it might actually result in reduction for Indian companies. Ultimately it depends on whether India offers any advantage wrt other countries or not, I will try to find that.

In terms of valuation, this is my simple (or simplistic!) thinking. After recent rise in stock price, the stock is trading at 40% discount to the valuation which was pre-covid and pre-high-duties-imposition. If we now discount 0 risk for the new higher duties then it would mean that discount for COVID slowdown risk is 40%. Smaller companies with such debts are easily trading at such discounts right now so it is debatable whether 40% discount is very high or low. I personally feel that while overall demand for industry might reduce in USA for Quartz slabs, Pokarna will have some tailwinds coming from lower duties wrt China. It will be interesting to see what will win between COVID slowdown vs tailwinds due to lower duties. Tailwinds due to lower duties are likely to last longer than COVID slowdown unless the later results in housing market collapse or so.

Disc

Invested@around 98 still evaluating

5 Likes

Hi Pratik,

Thanks for the analysis, I wanted to understand is basis of your valuation is new capacity, or the stock price or book value ?

What I mean to ask is how have you calculated its 40% discount to valuation ?

Disclousre @ invested prior to ADD imposition, try to taking a call between cutting loss v/s add to position.

The recent development is definitely a big relief for the company - given that a massive expansion was about to commercialize.

However, now the new worry would be on the demand side for atleast an year or more given that real estate would be the worst affected. It has been seen earlier that a new plant take few quarters to stabilize and may have a high fixed cost. So if co is not able to utilize the overall capacity to say 50%…how will they tide over?

There was an article in ref to Pokarna and granite industry talking about almost zero business in March itself as all of it was dependent on lot of foreign buyers and now that has come to a standstill.

Ayush

PS: Views maybe biased, exited the position I had earlier.

11 Likes

I was referring to the stock price which was prevailing before 80%+ duties were imposed and before COVID outbreak took place. At that time, the price was around 170 (nov 2019)

2 Likes

is final decision of US ITC out?

2 Likes

yes the final ruling came in favour of the company on 29th may.

3 Likes