Pokarna will lag till ADD issue resolved…there is an overhang of ADD given USA is the market for its business

Stock is up 15% today, are the results of ADD out? If yes, can anyone post the source of it? I am not able to find it.

No. They’ll be out post Oct 24. Today’s move is likely due to impeachment of the US president.

2 Likes

Thank you for your reply. The stock is languishing at such low valuations due to this issue.

US Dings Indian, Turkish Quartz With Early Duties

By Alex Lawson

Law360 (October 8, 2019, 6:48 PM EDT) – The U.S. Department of Commerce rolled out early-stage duties on imports of Indian and Turkish quartz used in countertops and backsplashes on Tuesday after finding that the products received a boost from government subsidies.

Commerce’s International Trade Administration handed down preliminary countervailing duties on the quartz surface products ranging up to 4.32% for India and 3.81% for Turkey in response to petitions filed earlier this year by U.S. producer Cambria Co. LLC.

“Commerce will instruct U.S. Customs and Border Protection to collect cash deposits from importers of quartz surface products from India and Turkey based on these preliminary rates,” the agency said in a brief statement.

Cambria has been aggressively pursuing trade cases against its foreign competitors, securing duties as high as 340% on imports of Chinese quartz in June.

Tuesday’s preliminary ruling saw Commerce hand out a 4.32% preliminary countervailing duty for Indian quartz, including for named respondent Pokarna Engineered Stone Ltd. One Indian producer, Antique Marbonite Private Ltd., was found to have received only minimal subsidy assistance, and will not be assessed any duty.

In the Turkish prong of the case, Commerce handed out a 3.81% preliminary rate, including to named respondent Belenco Dis Ticaret A.S.

The quartz surface products at issue in Cambria’s case are used to make countertops, vanities, backsplashes, flooring and mantles, among other items. Imports of quartz from India and Turkey were estimated at $69.5 million and $28 million, respectively, in 2018, according to Commerce.

Alongside its subsidy investigation, Commerce is also carrying out an anti-dumping investigation to determine whether the quartz has been sold at unfairly low prices in the U.S. market.

Attorneys for the companies did not immediately respond to requests for comment Tuesday.

Cambria is represented by Luke A. Meisner, Christopher T. Cloutier, Elizabeth J. Drake, Geert De Prest, Kelsey M. Rule, Nicholas J. Birch, Paul Wright Jameson, Roger B. Schagrin and William A. Fennell of Schagrin Associates.

Belenco is represented by Alexander H. Schaefer, Brian McGrath, Daniel Cannistra and Robert L. LaFrankie of Crowell & Moring LLP.

U.S. importers Cimstone, MS International Inc., Bedrosians Tile & Stone and Arizona Tile LLC are represented Jonathan T. Stoel, Craig A. Lewis, Jared Wessel, Michael Jacobson, Nicholas Laneville and Nicholas Sparks of Hogan Lovells.

Pokarna is represented by Ronald M. Wisla, Brittney Powell and Lizbeth R. Levinson of Fox Rothschild LLP.

The cases are Certain Quartz Surface Products from India and Turkey, investigation numbers C-533-890 and C-489-838, in the U.S. Department of Commerce’s International Trade Administration.

–Editing by Haylee Pearl.

8 Likes

Compared to initial fear, duty looks really less…

Maybe that’s why the stock rose today, given that these duties can be absorbed. With reduced corporate tax, they might be able to offset these duties (although I accept they already pay around 15-18% tax so it might not benefit much). Thoughts?

This case is not closed yet, we need to wait for Final One. May be management will be able to give some more light.

Is there any person here, who gives more light on ADD , between Initial and Final for other products in general…

Duty recommended seems to be much lower than what was feared. Even though it’s not a final decision, it’s a good indication IMHO. At PE of 5, this seems to be a good buy provided current favorable situation continues. I had sold out my position when this case was filed and have entered again now. Will have to monitor the development closely and if tailwinds in USA slows down then earnings might reduce resulting in price correction to even maintain similar PE level.

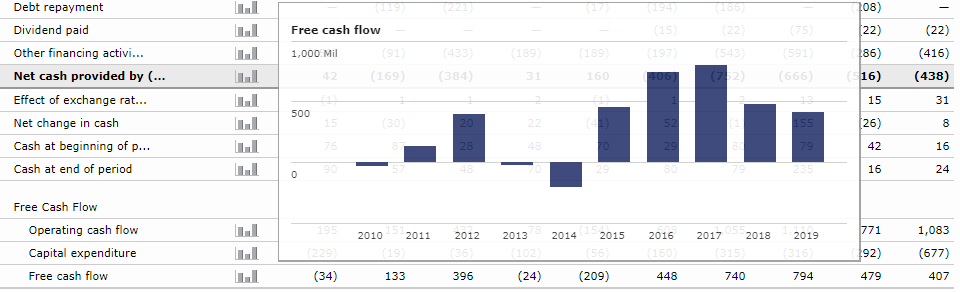

Cash flow of the company has been good in last 10 years. If company doesn’t face more tailwinds in USA then it can regain its long term PE multiple of around 10.

Disclosure

Invested.

4 Likes

AR19

Loans & advances from related parties

Loans from directors 3619.76 Lakhs (consolidate BS)

Does anyone know interest rate of this loan?

Invested

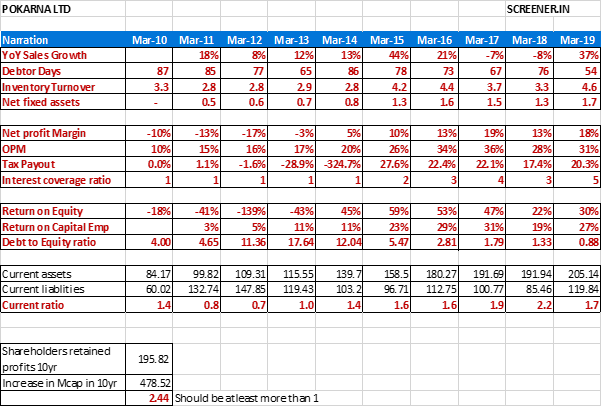

Debtor days are under control

Overall Operating efficiency improving

Interest coverage & DE ratio improving

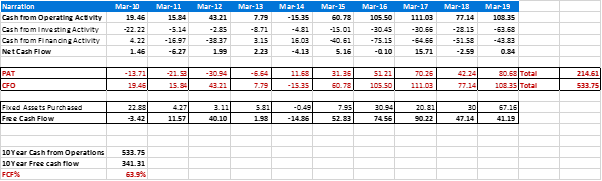

cCFO>cPAT mainly due to improving operating efficiencies

FCF is very good

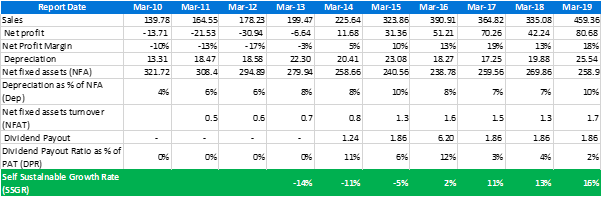

SSGR consistently improving, even if companies sales grows 15%-20% debt levels should be constant/decreasing.

available at very reasonable PE

Disc. : Invested

The only issue i feel are,

- Rent given to directors which is high

- Loans taken from directors (interest rate not disclosed in AR)

- US ADD Uncertainty

Senior investors - request you to guide anyone have information on above issues.

Hello Kalpesh,

I have been tracking the company from last 4 years now. Let me answer the questions you have asked

- If I recall correctly, in one of the conference calls they had mentioned that interest paid to directors were closer to 13%. At that point of time, even the bank borrowing was at similar rate however due to improving financial conditions, their bank borrowing rate has come down. As per AR FY19, their total related party loan is closer to 100 cr and they have paid 12 cr as interest which is not exorbitant. The company is going for expansion and I guess this might be the greed of the promoter or the need to have this loan. Basically promoter is getting more returns than any debt instrument out there.

- Rent given to directors is I think less than 2% of the profits. This is a corporate governance issue along with the Pokarna fabrics biz that they are running. I guess these issues are related to the archaic mind set of Indian promoters where they want to take equity shareholders for a ride. I am hoping that this thing will get resolved as and when company becomes bigger in size.

- ADD is the biggest issue for Pokarna. Given the large Capex that they are undertaking, high ADD may even threaten the survival of Pokarna. Due to this reason, one needs to recognize the risks associated with investing in this company.

It used to be one of my largest holdings but I had to sell it off due to these reasons. I have taken a fresh position at 150 odd levels but PF allocation is 1.5%.In my opinion, if the ADD imposed remains at current preliminary levels, the stock can become a multibaggar.

Regards

Kanv

3 Likes

The preliminary findings for Countervailing Duties have been declared but the same for Anti Dumping Duty is due by December 4th so even at Preliminary level, the threat is not over.

One thing to note is that in case of China, Preliminary findings had declared up to 178% CVD and more than 300% ADD. So ADD can be much more than CVD.

Disc

Have a tracking investment, watching closely

1 Like

Thank you for sharing this important information

Let us examine worst case scenario,

suppose US Imposes 300% ADD what will happen is sales in US will go down sharply,

but company still has standalone business - out of which apparel business not making profit, Raw granite blocks export to china & other countries is still there.

For some years sales & profit will go down significantly, company may have to sell some of its assets to reduce debt.

but eventually sales will come up as company will focus on Europe & Asian countries. It will take time to penetrate to those geographies say 3 to 4yrs.

In that 3-4 years if i get business sub Rs80 per share, i’ll invest heavily.

Senior members plz correct me if anything seems wrong.

Disc: invested, reduced holding significantly.

It is currently trading at a PE of 5 (maybe should be closer to 10) given the ADD overhang. So maybe if the US business goes bust, it might not fall by 50% given that the valuations are already depressed.

On the contrary, if the ADD is lesser than 300% or much lesser than the street anticipates, could it rerate to 10-plus PE levels?

I wonder whether this is going to help keep Pokarna and other companies away from ADD. This is very good news, any way:

It depends on how you look at this news. ADD on China had resulted in super normal profits for Pokarna and with new capacity coming on stream, it would have helped improving the IRR of the project given India doesn’t get any ADD imposed in December hearing.

Coming 2 months will be very important months for Pokarna and its investors.

Kanv

1 Like

Great set of numbers as expected. Granite division has taken a big hit. Management should clarify on what is happening on that front.

Inventory has gone down, possibly due to pre shipping before ADD announcement.

Key risk remains

a) Imposition of ADD

b) Resolution of US and China trade dispute which would lead to heightened competition and lesser margins.

Kanv

1 Like

Impact of granite business is more than offset by improvement in quartz business. Trailing PE of less than 5. My guess, just a guess, is that there won’t be much impact of the ruling in Dec, if the existing ruling is anything to go by. Capex numbers look good.