My notes from the Q2 FY17/18 concall. I have covered more from the overall business perspective rather than putting numbers, which we all know.

US Market -

USA’s construction market is buoyant. Shift is happening there from Granite/Laminates to Quartz. New growth that is happening is all in Quartz is in double digits, whereas Granite’s is in lower single digit. Everybody (all stone dealers who didn’t want to deal in Quartz earlier) now want to sell Quartz. But still US continues to be a very big market for Granite. US stone market isn’t matured (good runway). Granite business facing stiff competition from Brazil.

Players in US are trying to grab the lower end of the Quartz market as well (Chinese dominance currently). Will have to figure out right product mix across price spectrum. Price increases at will isn’t possible after product launching. So, despite higher RM prices (crude), they are unable to pass on the higher costs.

Caesarstone EBIT margins are close to 18-20%, while that of Pokarna is 35%+. Can this be a threat? Management answered that Caesarstone’s pricing points are even higher than that of Pokarna, but still if they are unable to make higher profits may be due to efficiency, lower labor costs, RM pricing, higher overheads, etc.

Quartz business -

Higher input price (crude) for Quartz and adverse currency movement impacts them. This is why Q2 was low on EBITDA despite full Quartz ramp up vis a vis last year.

At peak utilization (Quartz), they posted 58-60 cr revenue (last year), while in this qtr it is close to 51 cr at almost peak utilization due to the issues mentioned above. Throughput wouldn’t be higher in Quartz despite removing bottlenecks. What they are trying to achieve is increased realizations due to improved aesthetics (close to natural stone). They have pushed around 21 new products in the market. Takes 3-6 months for the verdict to be out. They expect results from this endeavor starting Q1 next year. These new products will replace some of the older products with lower realizations. These new products tend to attain 10-15% higher price, but mgmt wants to wait till q4 concall to give any concrete details.

Employee cost has been rising as they have already hired staff for the new plant. There is a big learning curve and takes time as employees are very critical for managing the operations of Quartz business. They want staff to be trained and ready for the new plant on time. They said employee expenses will be more or less the same going forward.

Increased sales and advertising expenses to improve visibility is one of the factors for lower PAT yoy in Quartz division. Will continue to advertise aggressively going forward.

Guidance for 35%+ EBITDA in any case.

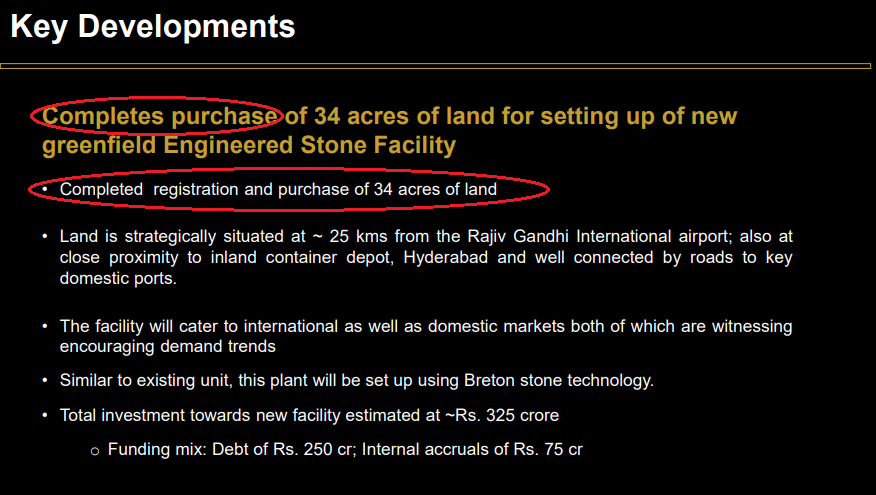

New Quartz plant -

Selected the location for new quartz facility. Legal due diligence underway. Plant will commence production post 18 months of the date of land finalization. Breton machine has been ordered but put on hold till land issue is resolved. Asset turns at peak utilization would be 1-1.25. Optimum utilization/stabilization from this new plant in itself will take 3-4 years from commencement. Ramp-up takes time.

Incremental 250 cr debt they will take for the new facility will not show up on the Balance Sheet even until next year. Moratorium period is 3 years.

On capital structure - debt vs equity for the new plant, they wanted to take the financial closure asap (route that was quicker). They can decide if equity route is needed later as well.

Granite vertical -

Improved performance in Granite vertical in Q2 comes from improved production from new quarry as well as value addition (cut to size i believe). Market remains extremely competitive. Mgmt hopes the market remains like this (doesn’t deteriorate further) in order for continued improvement in this vertical.

Miscellaneous -

Interest outgo is continuously improving. 7 cr for this qtr vis a vis 9 cr last year. This will further reduce due to credit rating improvement in this qtr for the company and its subsidiary. Also, regarding transfer of all debt to dollar denomination, management has given a deadline (Dec 31st) to the bank consortium to give a final answer. Mgmt expects 4-5% (on absolute basis) rate reduction from the current rates. This would be big savings.

Geographical expansion is on the cards. Have been looking at markets where they have not been traditionally present in a large way or not present at all. Europe, India, Australia (very small market).

GST reduced from 28% to 18% is good for the industry.

Total debt is 217 cr. Planning to pay 35 cr of outside debt (total outside debt is 117 cr) this year.

Revenue breakup - 99% of quartz revenue from exports. 61% of granite revenue from exports.

Breton gives them upper-hand vis a vis Chinese manufacturers. In India, it is a challenging task to educate users regarding difference between Breton and Chinese. Take for instance IKEA. IKEA has selected us as it doesn’t use Quartz from Chinese players worldover. Be it composition, technology involved, polishing, installation, staining, cracking…Breton is much better.

IKEA’s projections for India are very big. Though, can’t put a number on to it at the moment. Things are underway.