Repco Canfin, PNBHF - Uncanny similarities.

So true Yatharth.Public Sector Tag and for some reason market does not trust them.I made money in two of them but now sitting on a loss with PNB. The only hope is Gupta will turn it around in 1 or 2 years time

1 Like

Guys… PNB HF is a very different animal from Repco and Canfin Both.

While all HFC’s are commoditized businesses, PNB HF differs in DNA from both.

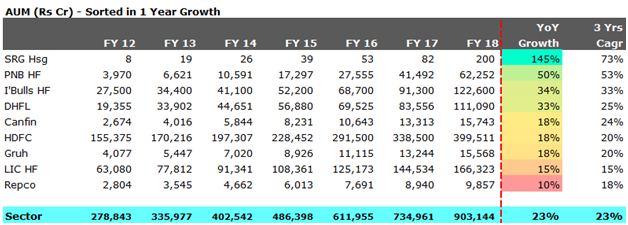

- Primary differences being - Much more growth hungry than Repco and Canfin. Differences can be seen in dibursements as well AUM

-

PAN India presence and not overyl dependent on regional markets (Both Canfin and Repco are South based)

-

High level of Non-Housing Loans - but excellent asset quality. Canfin is predominantly into plain vanilla Housing Finance. Repco has a high proportion of Non-Housing loans but their avg. ticket size is half that of PNB HF. So PNB HF focusses more on higher networth non-salaried individuals.

4 Likes

Now, the debate we should be discussing here is,

A. Why is Market ignoring all the good numbers of PNB HF. Is it not trusting such high growth. To answer that, lets look at actual disbursement numbers

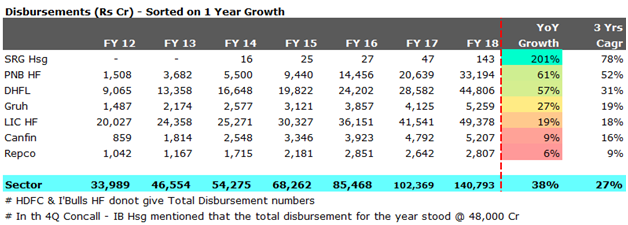

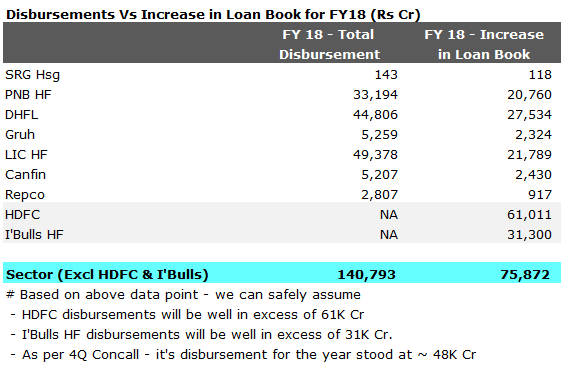

The table above shows that Actual disbursements are higher than incremental loan book - as loan book would be reduced by the repayments / securitisation. Point I am trying to make is disbursements are higher than incremental loan book.

-

HDFC (which does not provide absolute disbursement no) has increased it’s loan book by 61K Cr. So disbursement will be atleast if not larger than 61K Cr

-

I"bulls in it’s concall said it has disbursed 48K cr

-

DHLF has disbursed 44K Cr

-

LIC HF has disbursed 49K Cr

-

PNB HF has disbursed 33K Cr

Hence - PNB HF growth numbers, while in % terms look daunting and non-believable, are realistic as other HFC’s are disbursing much higher than them. It is more due to base effect.

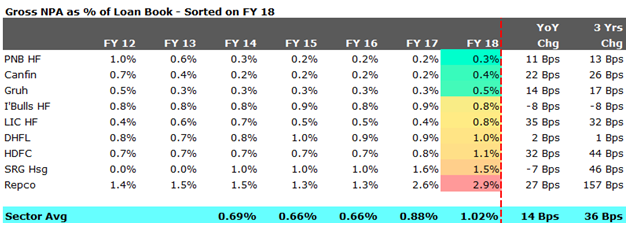

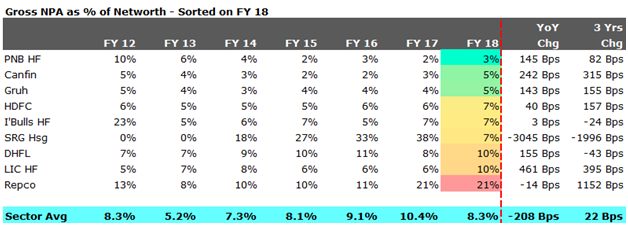

B. Gross NPA of PNB HF is the lowest. Then why is Credit Rating still AA+.

The reasons cited in all of the CRISIL rating reports is that the book is not seasoned and hence NPA’s are likely to creep up. Well this can be verified only with time - and hence one has to wait.

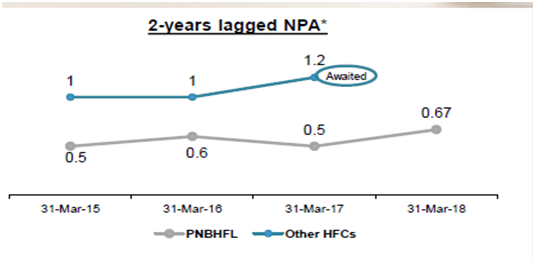

But the 2 year lag NPA for PNB HF is still below the industry.

The issues we need to discuss is

-

Is PNB HF different in terms of it’s DNA, as numbers suggest. If so, why is the market not responding to them. Is the market erring in analyzing these numbers or is it a value trap (growth trap as numbers are stupendous)

-

I understand parent wanting to divest it’s stake (owing to the issues in their own Balance Sheet), but why is Carlyle wishing to divest the stake at the same time as PNB. This will clearly hurt the price - as they together own more than 60% of the o/s shares. Are these numbers not good enough for them to stay invested,if not increase their holding? Are they aware of other business reasons, which is making them sell their stake.

Guys, if we can address these issues - we would have done a great job in analyzing stuff. Lets dig deep and address these issues.

-

We can skim through the reports of various broking houses to check if there are some red flags they have unearthed.

-

We can get hold of Morgan Stanley report, giving price target of 1,100/- (lowest amongst peers) and Carlyle appointing Morgan Stanley for their stake sale in PNB HF. They would obviously know something more.

12 Likes

Check out @ETNOWlive’s Tweet: https://twitter.com/ETNOWlive/status/1008618559176445952?s=09

Check out Basant Maheswari’s interview on ET Now. He is willing to wait out 5 years for PNB housing as he sees a long term story.

As far as I know, Carlyle is still on the board of PNB, and they will be forced to review their decision on selling, if PNB HFC keeps growing the way it does.They already have a multibagger. Sanjaya Gupta himself mentioned in the last concall, that PNB housing is an excellent investment for his promoters and he doesn’t expect them to leave.

1 Like

The biggest reason they would now sell is that the federal reserve is now raising interest rates which will cause tightening of government bond yields in developing markets.

This is definitely not good for HFCs in the short run. Since they invest for 3-5 years Carylyle can’t afford to wait out as some are saying. This makes sense for long term investors only and won’t be moving higher till the next government is sworn in in May next year. It’s overvalued as it is.

Invested

1 Like

Hi Rushil / All,

Lets dig deeper and not jump to opinions.

Fed raising rates would be a global macro, impacting all FII and PE investors. Fed raising rates will therefore impact a host of companies. HDFC recently raised 13,000 Cr. HDFC Bank got approval for hike in FII limits - all these suggest that good companies will continue to find investors.

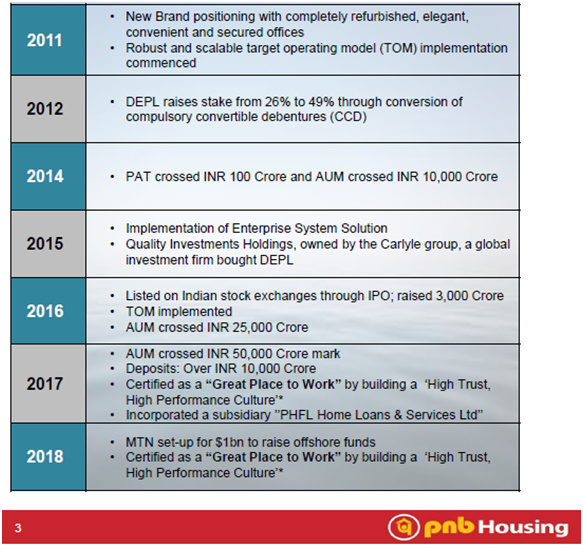

Carlyle bought DEPL in 2015, which had a 49% stake in PNB Hsg. Standing today they have 33% Stake, and it has been 3 years, so they have periodically monetised their stakes. Do they need to exit all in a go. I am not too sure. Especially if there is a business rationale to move out. If there are no red flags, it would be a wonderful opportunity for value investors to accumulate the stock as price will remain under pressure for huge stake sale reasons.

Another contrast to Canfin - When it announced a stake sale, price rose sharply, which is complete contrast to PNB HF.

Lets think a little more deep

3 Likes

Good work Ronak. Keep it up. The low gross and net NPA, is not surprising that the loans are appraised by employees, the majority of whom are Chartered Accountants, which is a moat, the business plan of private equity, fantastic growth and all this led by the Alexander of Housing Finance himself, who has skin in the game, and a veteran with decades of experience in mortgage financing. The departure of PNB will be good as the company should not be stifled by PSU culture. The departure of Carlyle will also be good no doubt, as they are too greedy for growth, which in fact is affecting the ROE. Sanjaya Gupta himself admitted that the high growth was affecting the ROE. Can they grow by internal accruals? Not while Carlyle is on the board.

1 Like

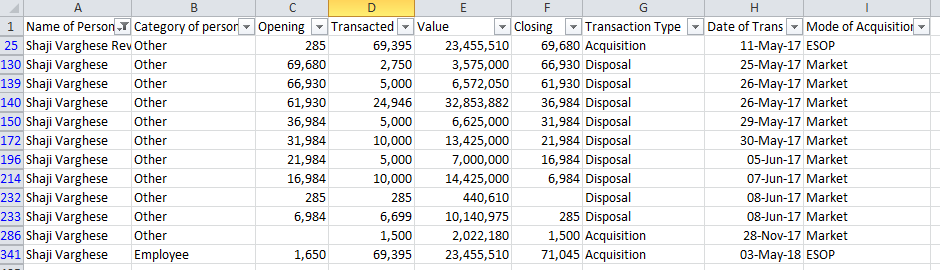

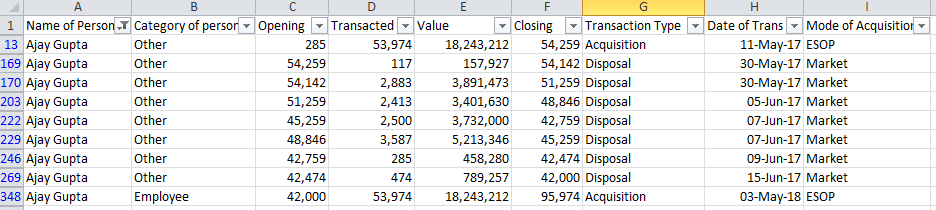

To look at it from the “Skin in the Game” angle, I just looked at the holdings of Mr. Sajaya Gupta, MD and his transactions. Appears he is not interested to hold on to the shares he gets.

As for Mr. Shaji Varghese, ED, Business Development, the story is similar.

Mr. Ajay Gupta, ED, Risk Management, he is mostly holding on to the shares except for some minor sales. For a Risk Management person, this may mean something.

Others are not directors and have lesser holdings so I have ignored them. I could not arrive at any definite conclusions from this data.

8 Likes

Generally employees tend not to think like “owners/shareholders” and cash out their ESOPs which are issued regularly. You will see similar trend in HDFC bank. I would not read too much into this.

If the directors/employees are thinking like shareholders, that you can figure out and use it to your advantage. And some do.

1 Like

Why can’t all HFC’s be like Gruh?

- No equity dilution/equity raising for growth

- payout 30% of profits as dividends

- provide 100% for all NPA’s (zero NPA)

- grow steadily at around 20% p.a. Highway of growth is so so long.

Do the above year after year after year…

3 Likes

Parentage Effect:

-

Whenever Punjab National Bank gets downgraded, PNB Housing Finance also will get down graded.

-

Daughter can not have higher credit rating than it’s parent

This is what management has to say in earnings call:

Sanjay Gupta: Before you ask questions, I would like to mention that the Company, promoted by Punjab National Bank (PNB), shares a common brand yet as per the regulatory stipulation maintains an arm’s length relationship with PNB and does not leverage the promoter for any business or resource mobilization. This is further validated by the rating agencies post the recent fraud issue reported by PNB in February 2018. The rating agencies reposed their confidence in us both CRISIL and ICRA have come out with a credit bulletin within a week stating that the incidence has no impact on the Company’s business and financial risk profile. Further, we feel that the recent development at PNB are unlikely to impact the credit profile of the Company.

1 Like

#CNBCTV18Exclusive | PNB Housing Fin rating may be downgraded as rating agencies are uncomfortable with LAP & developer loan exposures, sources tell @kothariabhishek pic.twitter.com/Ak21tfw5dH

— CNBC-TV18 (@CNBCTV18Live) June 19, 2018

Is share price of PNB Housing FIn justified ??? sharing a good article regarding this

Disc: Entered the scripe with small exposure this is not a stock recomendation

1 Like

For next 5-15 years, housing demand in India will grow unabated: Keki Mistry, HDFC

Here it is amply assured that they target ROE for inorganic growth.

Hence I don’t think they would want to buy pnbhfl

this looks like a spam link. They are in the business of increasing page views by providing generic stufff. I keep getting 100s of these on different stocks through google alerts. Is there any way we could block these?

1 Like

I have seen many people with home loans in urban Inida…PNB housing mentions maximum exposure is in Urban? but I hardly notice anyone having home loan with them. DO they have seperate offices or operate via PNB branches only? Is it more developer loans? It is very very difficult to beat HDFC and ICICI in urban india for a retail home loan i believe…in developer loan yes you can…

Some say market is worried about LAP exposure… pnb’s LAP is ~15% and LtV is hardly even 50% (from their presentation), so unless we have property prices crashing that badly why is that so worrisome?

Disc. Invested but conviction being tested