You may want to look at the number of branches of PNBHF and its Loan book. If my memory serves me right, it used to be something like ~900crs per branch. How is that possible unless the book understates builder loans, or PNB has transferred its home loans to PNBHF. If true, this questions the sustainability of the growth in asset book of PNBHF.

Thanks Amitayu for the thread. The biggest short term risk for PNB in my opinion are as follows:

a. Gross NPA being the lowest- could creep up in this environment

b. Loan to real estate developers is another potential trouble spot.

c. Competition is increasing in HFC

But Track record is excellent.So if they deliver it is a good bet. I am closely watching it now.

Dear Yogesh

Excellent comparison. To understand better what is inside credit costs.?

India bulls is scoring on many KPIs still considered very risky. Why. Is it because of their risky loans ? I guess NPAs comparison is missing.

IPO proceeds need to be added to Networth of FY16 to arrive at book value. Here is the working

PNB Housing Ltd

P/BV FY17E Working Rs. Cr

Net worth FY16 2144

PAT FY17E (20% growth) 409

Issue Money 3000

Total Networth FY17 E 5554

Pre-issue shares 12.69

of Shares issued IPO 3.87

Total No.of shares (cr) 16.56

BV FY17E 335

CMP 830

P/BV FY17 E 2.48

1 Like

@pranav_pratap It is due to their Unique Operation Model , After stake acquisition by Destimony (Carlyle Group’s entity) The managment initiated a restructuring program titled ‘Project Kshitij’ in 2011. The intent was to centralize and standardize business processes, sourcing strategies and credit policies. They made changes to the organization structure, developed a robust IT platform and introduced a fresh marketing initiative. As per this restructuring, 47 branches were positioned to act as the primary points of sale and assist with the origination of loans, various collection processes ,sourcing public deposit service etc while the processing hubs were positioned to provide support functions such as such as loan processing, credit appraisal and monitoring etc. Most Importantly they have more than 7000 channel partners (in house team + external hire ) which helped them to grow their business in rapid pace. This is the reason also their OPRX is higher than other HFCs but will decrease gradually once the business scaled up.

Thanks for clarifying Amitayu!

Their business model must be unique to manage such large volumes with few branches. I will look into this when I can devote some time.

I remember that when PNBHF was growing its loan book at a frenetic pace, PNB’s loan book of small ticket HF loans did not grow. That made me a bit suspicious whether PNB was shifting its home loan book to PNBHF. I had written about it on CanFin board about two years earlier, but afterward, I stopped tracking PNBHF.

2 Likes

Unnati is PNB HSGFN small ticket loan unit.up till 25lacs

What’s the effect on PNBHF of banks reducing lending rates aggressively? Can this reduce the growth rate or growth with relatively lesser margins?

Credit costs are all income statement expense items related to NPAs like provisions, write offs, etc. This give an indication how much NPAs are actually costing the company. Not all NPAs result in default a large number of loans are recovered so the ones that do default are either provided for and written off later from balance sheet or written off right away (write off expense in income statement).

NPA comparison is useful but I think credit cost comparison gives the same information especially credit costs as a % of loans two years ago. Since home loans begin to go bad two to three years after disbursal this metric gives correct picture than NPA. PNB scores bad here. Their NPA ratio is good because they are growing denominator rapidly to keep the ratio low but bad loans will come back to bite later if they are not paying attention to credit quality in pursuit of growth. With almost doubling of capital they now have to grow their asset book and I am afraid they will lend money to anyone and everyone over the next two years.

3 Likes

Headwinds for valuations

- Banks are flush with cash post demonetization

- New HFCs like Piramal are entering the space

- To add to more intense competition, interest rates are about the drop, as inflation cools and economy sags due to demonetization

Would you like to buy an HFC as a whole business today? If not, why its shares?

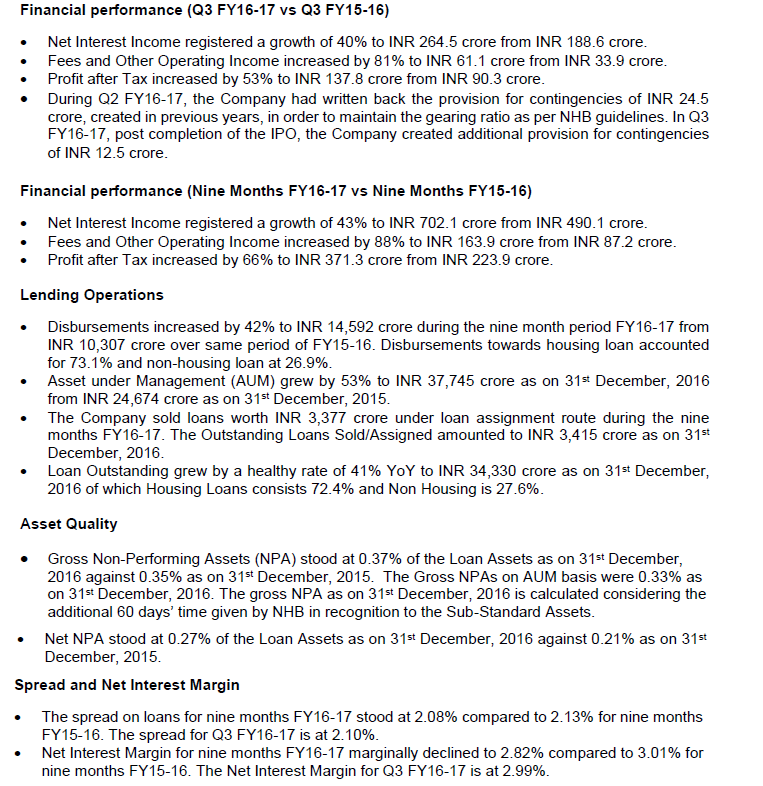

Q3 Results declared for PNB Housing Finance.

Q3 Investor Presentation http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/EC89502A_BA99_41E6_B557_3F88314A228D_161251.pdf

4 Likes

did anybody attended pnb housing concall today?

Basant Maheshwari disclosing his investments on PNB Housing, CanFin and small finance banks.

http://economictimes.indiatimes.com/markets/expert-view/it-is-not-market-led-bull-run-but-a-selective-rally-basant-maheshwari/articleshow/57056100.cms

2 Likes

Any guess on “small finance bank” which Basant Maheshwari mentioned in the interview? RBL Bank, Karnataka Bank, Federal Bank etc.

Regards,

Vinoth

I think its Ujjivan. Not so sure, but watch his old interviews to be sure.

1 Like

PNB planning to reduce stake in FY 18

Disc-Invested recently

so will they be selling the housing subsidiary?

disclosure: on my watchlist

What differentiates PNB Housing finance from its competitors? Where does the Company stand nationally?

PNB Housing Finance is the fifth largest player amongst housing finance companies in India, with 58 branches spread across 35 cities in India.

I’d say that our main advantage, when compared to our competitors is our unique target operating model empowered with a robust technology platform. We have implemented wing-to-wing enterprise system solution, which cuts across all functions and all geographies. Our target operating model brings in efficiency of scale in the system. Further, our people with extensive experience in the mortgage industry and work towards faster and seamless execution, in compliance with the regulation.

Back in 2015, PNB Housing successfully implemented a comprehensive business transformation and reengineering exercise ‘Kshitij’, led by Mr. Sanjaya Gupta, the MD of PNB Housing Finance. The transformation included revamping of our business processes, organisational restructuring, relook at policies and most importantly, creating and implementing a strong and scalable target operating model, which I believe brings in high productivity of our people. Our branches are the primary point of sale/service, focused on origination of loans, various collection processes, sourcing deposits and enhancing customer service, while our processing hubs and zonal offices provide support functions, such as loan processing, credit appraisal and monitoring, and our Central Support Office (CSO) supervises our operations nationally. Our enterprise system solution (“ESS”) integrates all the activities and functions within our organisation under a single technology and data platform, bringing efficiencies to our back-end processes and enabling us to focus our resources on delivering quality services to our customers. Our branches, processing hubs, zonal offices and CSO are supported by our centralised operations (“COPS”) and central processing centre (“CPC”), which provides centralised and standardised backend administrative activities, payments and processing for our business, relying in turn on the ESS. These processes are to date resulting in significant improvement in PNB Housing’s competitive position and scale of operations. All backend process are ISO certified which lends a lot of productivity in our service standards and turnaround time.

Last but not least, I believe that a major strength of ours is our brand. We are promoted by Punjab National Bank –the second largest Indian public sector bank. The public reposes lot of confidence in our brand; which stands for trust, service and fair play.

What would you say are the biggest challenges facing housing finance companies in India?

I think one of the main challenges facing companies such as ours is the irrational pricing and intensified competition. There are many companies that offer products at very competitive prices. Another challenges that puts pressure on our profitability are business origination and high operating costs, coupled with balance transfers due to restriction by regulators on pre-payment charges. Under this kind of environment, it becomes quite challenging to deliver return on assets or return on equity and fulfil the expectations of the investors.

However, we remain positive, believing in the growth trajectory of the business. We continue doing our business efficiently and maintaining cost levels which shall help in our profitability.

What do you see as the biggest game changers for housing finance companies in 2017?

Back in November 2016, the Indian Government decided to ban the old INR 500 and INR 1,000 currency, which resulted in reducing the currency in circulation by more than 85%. I believe that this demonetization exercise undertaken by the Government is a positive step towards bringing transparency in the real estate sector in the long run. As a result, I foresee that valuations and transaction velocity will be more accurate and will gain pace, respectively, over time. The Mortgage to GDP ratio of our country is very low at approximately 9%, especially when compared to other countries such as China (18%), Hong Kong (45%), and the US (62%). Hence, we expect that there is a lot of growth potential to the overall housing finance/real estate industry in India.

Thrust of the Indian Government on the housing sector with the mission of Housing for All by 2022, subsidy on interest payment, under Pradhan Mantri Awas Yojna will most certainly give a boost to the housing finance industry too. Also, the Government’s smart cities mission to develop 100 cities all over the country making them citizen friendly and sustainable will help the industry growth.

What’s in store for PNB Housing Finance in the next year or so?

In the near future PNB Housing is expecting to see an expansion-led growth. As on 31st Dec 2016, we have 58 branches in 35 cities in India and we’re looking forward to increasing this number covering higher number of cities.

With majority of Investments behind us, we expect the operating leverage to play out. We expect that, over medium term, our Cost to Income ratio will be inching towards the Industry average (FY16-17.2%). At PNB Housing we continue to thrive to maintain our GNPA lower than the industry average (31st March 2016-0.87%).

As Chief Financial Officer, what motivates you most about your role?

For me, it’s about the long-term opportunity ahead of us. I’m passionate about what I do and about PNB Housing because I think we’re delivering exceptional service to our customers in respect of their requirements, and doing it in a way that puts both customers and employees first. As the CFO, I get involved in all business functions and I play an active role in developing and defining the overall strategy for the organisation. I act as the face of the Company on all issues related to overall financial performance, which motivates and excites me, while also providing me with a high level of career satisfaction.

How would you evaluate your role and its impact over the last year or so?

As a CFO, my role over the last year was very challenging and also critical from the organisation perspective. Firstly, the Company embarked on raising tier I Capital through Initial Public Offer (IPO) and I spearheaded the overall process. The IPO process involved several critical aspects, including regulatory approvals, appointment of intermediaries, Red Herring Prospectus and agreements to be in place, compliances under SEBI (Stock Exchange Board of India) regulation, Investor Roadshows etc. The IPO turned out to be the largest IPO by a HFC in India and the second largest IPO in 2016, which was oversubscribed by more than 30 times. It also met the largest QIB demand in the last 5 years, with participation from several quality long-only institutional investors, which is something that I am very proud of.

In the past twelve months, I was also, actively, involved in raising funds through securitization at a very critical time, when the gearing of the Company was very high and was close to the upper cap, as per the National Housing Bank (NHB) regulations.

We raised funds, valued at US$150 million from multilateral institution, i.e. ADB (Asian Development Bank). We also became the first HFC to raise funds under Green Bonds from IFC – valued at INR 500 Crores.

As the cost of borrowing is a key parameter for a mortgage company, over the years we also reworked the Borrowing mix, which reduced the cost of borrowing that resulted in improving the profitability of the Company during the year.

Additional assignments that I have been working towards have been improving the profitability and efficiency of our business strategy and providing insight and analysis to various functions.

7 Likes

I recently saw advertisements in Times of India, Noida where PNB Hosuing is offering housing loans at 8.5%. My question is - isn’t this a loss making proposition when their cost of funds is at or higher than 8.5%? Any guidance on this aspect is appreciated.

1 Like

Due to the expectation of rising NPAs in Q4 post demonetization for all the housing fin companies.

1 Like