A fellow investor Manish Parikh of Vibrant Securities has done some wonderful work on Pix. He attended the last AGM at Nagpur and also interacted with the mgt. Manish has been generous enough to share his notes with me. I found the notes very useful & it helped me build conviction in the story. Attaching the notes pertaining to both the AGM as well as the mgt. interaction. Vibrant has recommended Pix to their clients first in October '17 & then again in Oct '18. Also attaching them with permission from Manish. Hope its useful.

Hi Rajeev, Pix is operating at 80-85% capacity utilisation…What are the expansion plans?Where is the growth in revenues coming from after 90-95% utilisation? Are they setting up new capacities?

These reports and notes are pretty useful. I hope you had taken the authors permission to publicly share the same?

Its interesting to see that the company is selling belts of such a huge amount and even more interesting thing to see is that the same is being sold in replacement market and that also through a wide dealer/distribution network.

But given that this would already be a highly penetrated area, won’t the growth potential be limited?

Yes, As mentioned earlier, I have taken permission from Vibrant Securities for using their notes for the benefit of other investors.

As regards growth potential is concerned, for starters there are only a couple of serious players in the non-auto sector where Pix is operating. The other being Fenner. As mentioned in the notes, the fact that all belts are periodically replaced on a regular to avoid unnecessary shut downs makes the business somewhat recession proof. So all large plants, be it power, cement, steel etc. etc. need the belts to be replaced on a regular basis. This itself is huge. Besides, India will continue to grow rapidly at 7-8% a year over the next decade at least, so the opportunity going forward is also big. I also gather that the mgt. is very bullish on the agricultural sector where Pix is the market leader &. the opportunity size is huge given the low base

The fact that for any new player it would take at least 3-5 years to make a mark (details given in the notes), gives the business a moat as there are barriers to entry. To my mind, Pix is clearly a market leader in a specialized business & I am unable to figure out why the valuation are what they are. Either I am missing something or the market is still to appreciate the story.

Agree on your analysis of Pix but concerned about whether these positives will translate to better shareholder gains ?

Even before announcement of the result, pix was down 10% even though it was expected to give good results due to softening of crude prices. How can one explain this ?

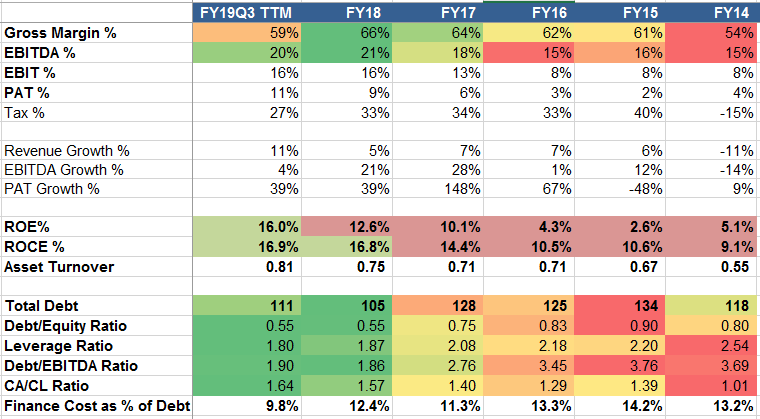

As mentioned in an earlier post, the “Other Income” in Pix cannot consists of a) Interest & Dividend and b) Forex gains. Since Forex gains / loses cannot be predicted with any degree of certainty, I decided to ignore other income altogether, even though one part (Int / Div) of it is regular and somewhat predictable. The idea being to better understand / compare the numbers. One interesting point that emerged was pertaining to the operating margins which have been steadily improving from 14.61% in 15-16, to 18.41% in 16-17 to finally 21.25% in 17-18. This should logically mean that any growth in Sales should lead to a dis-proportionate increase in profitability.

The Sales itself have grown @ 25% in the nine months of the current year over the same period last year. This is in contrast to the Sales growth of about 25% achieved over the last 3-4 years!

Being invested in Pix, I do all the scuttle butt I possibly can. I understand that Pix is in the final stages of their current capex, & there is no meaningful capex due for the next couple of years. The Co. hopes to grow @ 20% top line for the next few years. With all the cash expected to be generated in this period, one can expect achhe din going forward! Logically, a hefty dividend or a buyback, or both become a possibility…

The Pix Mgt. is smart & capable. The markets tend to be myopic at times. Nobody seems to remember that Pix sold its Hose division to Parker, a Co. 100 times bigger that itself for about 250 crs. only in the year 12-13, when its own market cap was a mere 90 crs!

I have also checked from multiple sources & can confirm that the notes posted on the AGM & the mgt meet, courtesy Manish Parikh of Vibrant Securities are largely accurate & his efforts are truly commendable!

This video on the Co. website throws some light on its activities.

Could you please provide the source.

I In the year 2012 the company sold part of its businss for Rs.856 million.

Afterwards I have not come across any such deal.

Thanks in advance

A closer scrutiny of the 12-13 Annual Report reveals that there was an exceptional gain (Sale proceeds less book value of asset) of 133.96 crs. This pertains to sale of the Hose division to Parker Hannifin.

However, the larger point that I was trying to make was that the Pix mgt. have the wherewithal & bandwidth to scale up operations as well as to sell out should the opportunity present itself.

hi

as per the research rep Fenner is mostly in auto belts supplying to OEMs and not into non-auto belts. Most auto belt mfg cos suffer sue to competition from global suppliers as a result Fenner gets most of the auto sector orders.

Also that Pix shies away from low margin high volume auto-belts business is heart warming as there is no dearth of business and Co can focus only on high margin business. That’s something that cannot be said for many companies across the auto sector.

I recently obtained the list of the top 100 share holders of the Co. One Foreign Investment Co. by the name of Cresta Fund Ltd. has recently picked up One lakh shares in the Co. A google search of Cresta Fund’s other holdings makes interesting reading!

Pix, to my mind is standing at an inflection point. With all the cash expected to be generated in the next couple of years and no more planned capex, one can expect a major de-leverage of the balance sheet. Increased Sales will bring in operating leverage & higher profitability will get a further boost with lessor interest outgo. If the story unfolds the way I envisage, than it is more than likely to get re-rated in the coming months. The March quarter results will be keenly tracked.

However, to me, the biggest question is: Do we see this business growing well (say >15%) in the next few years? If yes, why?

Vibrant report also only talks about macro things e.g. Capex cycle for industrial sector, mechanization in agriculture etc.

But there is no quantification directly related to Pix e.g. Order book size, Volume growth trend etc.

@django

I understand from reliable sources that the mgt. is aiming for about a 20% Sales growth per annum for the next couple of years. The last few years have been spent in adding capacities / plant modernization with includes the use of robotics as well! (The Co. has actually been reducing its labour force each year). If you notice, the Sales growth in the first nine months of 18-19 is in excess of 25%. The main reason for growth is that with the advent of GST, the unorganized sector is facing severe headwinds & business is gradually shifting to players like Pix. Exports too are growing well with the Co. entering newer geographies. US is the mother of all markets & the Co. has been pursuing it relentlessly for some time now. That said, the proof of the pudding is in the eating! The coming few qtrs. will help us understand whether this 20% growth is sustainable or not.

My hunch is that in two to three years the Co. should have gathered the scale, & with it a higher valuation & perhaps be ready for the picking! Don’t be surprised if an American suitor comes calling!!

Promoters remuneration is around 7.19 Cr on a profit of 21.5 Cr (33%).

2 Cr interest payments on a 16 Cr loan from Promoters (@12% ROI). Same highlighted by Dr. Malik in his analysis.

Additional 1.75 Cr Rent paid to the Promoters Enterprises.

As per March 2018 , They have 6.75 Cr in Bank , 2.5 Cr in Hand and 11.25 Cr of Current Investments. When secured loans are much cheaper than Unsecured from promoters , an investor friendly promoter would have retired the unsecured debt in first place.

Promoters does not look that friendly but if other growth factors played out , it can definitely provide decent returns in 2-3 years time.

Pix came out with a mixed set of numbers for Q4. The biggest disappointment was the de-growth in Sales of 5.67% to 75 Crs bringing the Sales growth for the year 18-19 down to about 15%.

The good news is that the raw material pricing woes are done & over with & the Co. is back to its earlier higher operating margins. The results look worse than they are also because of the “other income” component which came in at 1.07 crs. as against 3.63 crs. in Q4 of last year. As mentioned in an earlier post, perhaps it makes sense to disregard other income altogether & focus on the core business.

The current valuations are what makes Pix attractive. At 176 it trades at a trailing multiple of of 8.4 & this is for the stand alone entity. The two marketing subsidiaries could easily add another 2 crs. to the bottom line. It’s possible that the stock corrects in the immediate short run as the results suffer in comparison with Q4 of 17-18, but if that were to happen, then it would make the stock that much more attractive.

All said & done, if Pix is to create wealth for its share holders, it will have to grow its top line by 15-20% a year. Is that a big IF?!!

I recently attended the AGM & came back pretty satisfied. The Co. has been consistently modernizing its plants which are now state of the art & largely automated, besides being backward integrated with a fully automated rubber mixing plant to ensure product consistency. As a result the belts produced by the Co. are comparable with the best in the world. In fact, Pix is exporting to over 50 countries under its own brand. The US market is huge & Pix has made some meaningful inroads there. Currently the Co.'s sales are divided equally between domestic & exports, but going by the size of the global market, the exports may grow & become dominant going forward.

There is a misconception about belts being largely a commodity product. Each kind of belt has a different rubber constitution & require a high degree of engineering. With Pix almost not supplying to the auto OEM’s, its belts are largely used by the end user directly. It’s only a matter of time before the markets appreciate its full potential & the stock gets re-rated.