Hi @constantseeker_

If you look at slightly longer term, over last 5 years, each stream of their pharma business (pharma solutions, critical care and OTC) have grown @ 14-15% CAGR. This, though not exceptional, is decent enough in the context of the base from which they have grown (i.e they are among the larger players in CMO space in India).

Secondly, typically, the critical care business (inhalation anaesthesia) industry has been growing @ CAGR 5% on global level and PEL has outgrown the industry (and thus has increased market share) by a margin over last few years.

We should also keep in mind that, the growth in financial service business has been very high (of course due to small base effect!) and that may remain so for 3-4 years till they reach a scale from where the growth will moderate. Thus, on overall basis, the growth of pharma @ 13-15% and higher growth from financial services shall lead to 17-20% kind of growth, which seems decent to me. If they are able to drive the significant sales from Imaging business, that would be add further fillip to the growth

However, one concerning area is the information management business, where the growth has indeed slowed down in last 5 years (As can be seen from the numbers mentioned in AR, the growth is 7% CAGR). This may be result of the business reaching a saturation point. This year, they have articulated a vision whereby the target market is going to expand for that business and that may lead to higher growth in next few years. However, we still have to wait and watch how it unfolds.

So, all in all, I do see company growing at 17-20% CAGR over next 3-5 years. If we combine that with operating leverage and margin expansion (due to higher leverage for financial service business, lower R&D cost (due to recent cost rationalization) and generating revenue on recurring cost of imaging business), the bottom line growth can be higher than top line growth.

I quite agree with you on lack of information on financial service business. All the parameters that you mentioned and many more parameters specific to FS business should be made available for investors to help them understand the quality and sustainability of that business.In fact, I have in the past requested to their investment cell to disclose such parameters to help investor understand the dynamics of their FS business better. He had promised to take that up with the management, but at least for now, it has not been given attention to.

On Pharma profitability, I am not able to get your point clearly. If you can elaborate on your statement on “improve pharma profitability” with some number, it will be useful. My understanding from rough numbers is that their pharma business is generating around 25% EBIDTA margin, ex-R&D cost which from this year will come down significantly. We shall also keep in mind that Imaging is part of pharma business and that expenditure, as of now, does not have corresponding revenue. So, if and when the revenue comes (From Nuraceq or any other compound) the profitability may improve.

a. in 2014, on sales of 2877 crores, they had a loss of 162 crores. At this time they were investing in NCE as well.

b. in 2015, on sales of 3165 crores, they had loss of 497 crores. 300 of this can be attributed to NCE as a result of the write off. Even if you exclude this, segment profits (EBIT by their definition) is down from (5.8)% to (6.3)% which is worrying.

Am I missing something here? Can you please help me understand the 25% EBITDA margin? Thanks in advance.

There are two things that is factored into the loss numbers

Piramal Imaging, which is part of the pharma business is making EBIDTA level loss of around 100 odd crores (Pg. no. 96 AR FY 15). Now, Piramal acquired this business from Bayer at undisclosed sum. This acquisition premium (over book value) would have been amortized and will be part of the reported EBIT number. Thus EBIT number will be higher than 100 Crore and closer to 150 Crore (as it is the net loss of the company)

As you mentioned, its EBIT number hence depreciation and amortization charges are included.

on EBIDTA margin, my calculation had some mistake as I had added back R&D cost and depreciation to the standalone EBIDTA number (356+89+183) = 628 and had divided the same with revenue 2400 Crores giving me margin of 26.1%. However, I did not separate out the FS business as Standalone business also contained some part of FS business.

The revised calculation is as below

In 2015, the total revenue from this business was 2400 odd crores. We know from AR that net of Associate income and dividend from Shriram (Refer to Chart on page no 53 of AR FY 15) 800 odd crores. From FS subsidiaries, the contribution is around 240 odd crores ( Refer Pg.96 , AR FY15). Thus the total contribution in standalone number from FS business is 550 odd crores. Thus, in standalone numbers, Pharma contribution is 1850 Crores.

Now going back to stand alone numbers, subtract following from 1850 Crores

RM+Stock in purchase and trade

proportionate share of employee benefit expenses (70%)

Proportionate share of other expenses (net of R&D cost) (70%)

You will get around 350 odd crores of EBIDTA i.e around 19% EBIDTA margin.

As I mentioned, this is very rough calculation (back of the envelope). Going to the more granularity may give us more accurate numbers. However these numbers may give good inference

Well established pharma businesses (Pharma solutions, Critical Care and OTC), on operating level, are not as bad as it looks on face of it.

Revenue from imaging business, is critical for improvement in overall profitability of pharma business and remain major risk (like for R&D cost incurred, if PEL is not able to monetize investment made in imaging business)

Looking at the acquisitive growth of businesses, where eventually the acquisition cost above book value is amortized, OPBIDTA/EBIDTA may be a better and consistent indicator of company performance.

Notes:

• Strong revenue growth during the quarter :

• Up 25% at Rs.1,474 Crores during Q1 FY2016

• Growth across all three business segments during the quarter

• Operating profits were 93% higher at Rs.300 Crores during Q1 FY2016

• Net Profit (excluding exceptional item) increased to Rs.205 Crores in Q1 FY2016 from Rs.55

Crores during Q1 FY2015

• Pharma Solutions revenues grew 27% during the quarter, primarily driven by growth in its

Formulation business

• Total Loan Book increased to Rs.7,611 Crores as on 30 Jun 2015 as compared with Rs.3,193

Crores as on 30 Jun 2014. Total Gross Assets under Management grew to Rs.8,676 crores.

• Real Estate lending saw highest ever disbursements during the quarter

• Carried out two Special Situation investments worth Rs.1,175 Crores

• Information Management business continue to expand geographically – Post establishing

presence in China, moving ahead towards establishing presence in India as well

Inference:

• Operating profits higher due to major reduction in R&D expenses. It was mentioned earlier also that the company would scale down on R&D as it considers it a high risk. I am not in a position to evaluate this, as I do not understand the dynamics of the same. Best to keep it with the management, who have been in the same and doing it (capital allocation) correctly over the years.

• Pharma solution business’ revenue increases. I guess it is due to launch of florabetaben. @desaidhwanil kindly confirm if you have any idea.

• Loan book and real estate lending have increased. This is a good sign, as the capital is now allocated to a high return product/service. Also, PEL will get higher management fee.

According to me, it proves Mr. Piramal’s point, made during last presentation, that the company is at an inflection point now and growth will now be witnessed.

Disclosure:

I am not trying to view the company deeply over Q on Q basis, but as a streaming movie which unfolds beautifully, Mr. Ajay Piramal being a master allocator of capital.

Invested since more than a year now.

Thanks!

The real story which will shortly unfold is the demerger of Piramal Capital and Piramal Healthcare from Piramal Enterprises. Company website has named the separate businesses thus under the Piramal Enterprises umbrella. Could be that the mother company will hold the information management businesses until it achieves some maturity.

At the AGM Ajay Piramal neatly evaded questions. But all presentations and communications from the company show that Piramal Capital and Piramal Healthcare have been decked up like potential brides to be given away in marriage.

Piramal Enterprises likely to sell of its Critical Care business.

Critical Care business clocked a turnover of around Rs. 750 crore in FY 14-15.

It is growing at 18% over the last five years.

In your annual reports revenue part of the Pharma business has been explained in very

detailed manner. But profitability is not very clear. As per segmental results

pharma business seems to have incurred loss 136crs after excluding extraordinary

losses [300crs]. Is my understanding correct this is mainly lead by OTC

business and Imaging? Can you elaborate more on the profitability of all the

four division in pharma business?

CRAMS & Critical care in profits. OTC EBITDA breakeven… Imaging business still in

development stage. NCE research activity is shutdown, this should lead to

better profits of this segment going forward.

As per the standalone accounts, CRAMS EBITDA margins appear to be in single digits. Some

of the foreign subsidiaries seems to be incurring losses. When can we expect the consolidated EBITDA margins to reach the double digit?

CRAMS EBITDA margin 15%

In the CRAMs business we are growing at 14% CAGR for last three years. Over next 3-5

yrs should be expect similar rate of growth or can we expect 20-25% CAGR. ?

Growth rate of 15% over next 3-5 years

Revenue Growth in information management is only 9% CAGR for last five years which

includes acquisitions. Under financial results of subsidiaries, Decision resource inc, consolidated shows Loss before tax of 105crs. Can you please explain the reasons for loss and what sort of growth can we expect over next

3-5 yrs?

DRG revenue growth of 15% over next few yrs – half of this growth will be through acquisitions. DRG EBITDA margins at 25%

In the annual report it’s mentioned that “the Company plans to increase leverage by targeting a diversified liability mix”. What’s the maximum & minimum cap you want to put on leverage?

4:1

Over next 3-5 yrs will NBFC division will continue to focus on real estate financing or

diversify into new areas? Once the distress situation is over in infrastructure

and real estate financing, then it may not be possible to get high yields?

No Clear answer

Investment in Shriram Group is now approximately 20-25% of our market value. What are the

plans going forward? Will the company continue to hold investment passively or will get involve in Shriram group more actively?

Management said they will have more active involvement going forward

Going ahead can we expect more capital allocation towards strategic bets like Shriram

capital or given a chance company will again do opportunistic bets like Vodafone?

No more capital needed for Shriram Capital.

Not looking to enter new sectors. For some time had plans to enter defence, now the

plans are shelved

IBM Watson which also does analytics and DRG are different products and DRG do not compete

with Watson?

162 crs on incurred on advertisement. Out of this 112 crs on OTC, 20crs on DRG and

30crs on Pharma solutions

Most imp. question which I forgot to ask : Currently excluding extraordinary income ROE is in high single digit. When can be expect to see high double digit ROE?

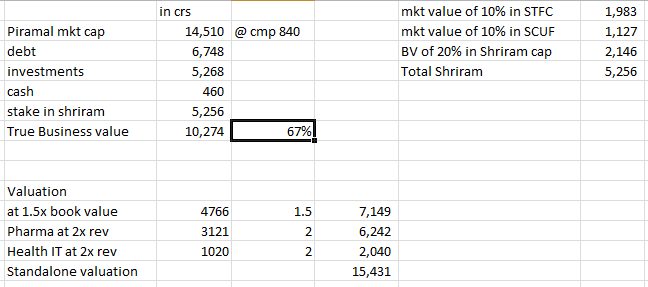

Thanks for your valuable inputs to this thread and to the forum. I have been invested in Piramal for few years and I use a rough back of envelope valuation. Very glad to know it is in lines of senior investors like your’s.

Query - I am backing out investments (non Shriram) to arrive at true business value and comparing it against standalone valuation that includes NBFC book.

Are these investments different (via Piramal Realty) or they are part of NBFC books leading to double counting.

Will appreciate if you could share your views. Thanks for your time.

First of all, we all are students of investing and try to learn from each other hence shall call each other by first name without any suffixes like sir. I no way deserve it so request you to address me with first name.

To answer your question, you need to look at the Investment entries in AR and see which ones are overlapping and exclude them. Rest of them you can deduct. Many of the Investment entries are already part of NBFC business and hence leads to double counting. Though, it is slightly tedious exercise, one must do it to arrive at true picture.

Also, have you also counted the value of its alternative asset management business in the valuation as I am not able to see it anywhere. Typically asset management companies are to be valued at 6-10% of AUM. Since piramal operates in niche and high yield areas, the valuation will nearer to the ceiling than floor.

I took the investments from Balance sheet schedules, both current and long

term. I couldn’t find a way of sorting them into pure investments vs part

of nbfc book. If a transaction is part of nbfc business, should it appear

as investment at all or it will be treated as an advanve. Eg, sbi will not

classify my home loan with them as investment but rather as an advance. In

essence can a transaction be a part of loan book as well as investment.

Second, i didnt include alt asset mgmt/piramal realty because i was not

clear of their ownership pattern. Are they held by Piramal enterprise or a

group holding company. So conservatively avoided them.

Ajay Piramal is shrewd businessman who knows how to buy out-of-fashion business cheaply and how to sell them high after turning them around. He has done that with pharmaceuticals and now he is trying his hand at Financials.

Due to his interests in pharma, financials and IT, analysts have always struggled to value his company. Since research firms have analysts dedicated to one area, they need to put 3 analysts to track Piramal Enterprise. . Also you would not see AP or his deputies coming on air and explaining their numbers or proving guidance on future plans. Hence IMHO Piramal would never be a stock market darling.

I came across interesting article in Mint on AP’s and hence felt like sharing with fellow Valuepickr’s

Disc - invested for last one year so my views could be biased

I am extra bullish on Piramal Enterprises today as a real estate and Over the counter products and pill distributor. I think with this kind of dividend pay out and high cash flows and new investments into company it can rock

Piramal Pharma’s CEO Vivek Sharma got awarded CEO of the year for 2015 at CPhI Worldwide convention held at Madrid Spain on 14 Oct 2015.

As per the news, Piramal Pharma got voted among top 10% contract manufacturing organizations (CMO) for both 2014 and 2015 due to its focus on customer centricity, quality and reliability and have become partner of choice for pharma as well as biotech firm. Their efforts in antibody drug conjugates (ADCs) got recognized when Piramal Pharma was awarded “Best contract provider for ADC” in 2014.

This clearly goes to show AP’s efforts are paying off. Please see the link to complete news item below -

. Also you would not see AP or his deputies coming on air and explaining their numbers or proving guidance on future plans. Hence IMHO Piramal would never be a stock market darling.

. Also you would not see AP or his deputies coming on air and explaining their numbers or proving guidance on future plans. Hence IMHO Piramal would never be a stock market darling.