I have been invested in PI Industries for many years now. The aspects which appealed to me first, continue to appeal to me even now. The company has, over the years, managed to strengthen its moat and scale greater heights. The way the company has scaled its CSM & CRAMS business along with strengthening domestic distribution has been exemplary.

Recently, during the Valuepickr conference in Goa, I was thinking about if PI’s business moat and whether it was widening or shrinking. So, I decided to see how they were placed and see if I can poke some holes in their story.

BEAR CASE

Move from contract research to manufacturing will mean additional capex, reduced asset turns and lesser ROE

Bayer, PI’s largest client, is forecasting poor agrochemical growth due to high inventory, farmer stress in Brazil and Europe, reduction in corn acreage in US

Excel Crop has applied for manufacturing registration of (Bispyribac Sodium) Nominee Gold

33% of the products in PI’s portfolio is in-licensed and faces a risk of import restrictions

Tax rates to go up substantially from 10% to 22-23%

With Bayer’s acquisition of Monsanto (if it gets completed), there may be some changes in the relationship with PI

BULL CASE

$6bn is going off-patent in next 6 years

Moving to Pharma CRAMS, a much larger market. Inducted a team from AstraZeneca over last 2 years. They have also inducted a Pharma veteran - Mr Balaganesh, ex-MD and Head of Research of AstraZeneca’s anti bacterial research facility - on their board as Additional Independent Director. Several other senior level recruitments to drive Pharma CSM.

Domestic market to grow substantially.

Imports made more stringent, hence more products to be made in India versus imported

Recent tie-up with Kumiai Chemicals for producing Nominee Gold in India and also partner on other new molecules

JV with Mitsui for providing registration services - pre-launch feasibility analysis, market research and feasibility analysis. Mitsui is a global major in performance materials, petro & basic chemicals and functional polymeric chemicals

JV with BASF to produce

Pendimethalin - Global sales US$325m - directly competing with Rallis in India

Saflufenacil - Global Sales US$180m

Dimethenamid - Global sales US$145m

Order book of $1 bn (June 2017) for 8-9 molecules

Improving margins due to better product mix and operating leverage

Jambusar facility capacity utilization is 65-60%, leaving a lot of room for operating leverage to kick in

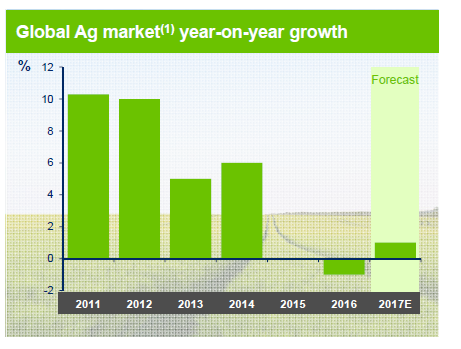

Global AgChem spending has been on a downswing and a recovery is supposed to pickup from 2018

From Bayer’s presentation - Jun 2016

Conclusion:

PI seems to be consciously changing themselves with JVs & partnerships to launch newer service offerings and product launches in India. Having done very well during the time AgroChem producers have struggled globally, they are poised for better times in FY19. The near term (1 year) may still remain a struggle due to the industry headwinds and revenue growth may not be very strong. The business seems to be on a very strong wicket specially given that agriculture as a sector is likely to be very strong with increased global population and need for more efficient & abundant farm production.

I have been invested in PI and following the developments esp of forming JVs with global majors. This seems to be a well thought out move in an attempt to strenghthen the business and enhance the run way. Govt’s focus on domestic production should provide the co with more orders from its foreign partners.

The domestic agrochem scene might be good atleast for the season with very good monsoon progress. How PI utilises this opportunity needs to be seen.

The order book of 1 billion USD inspite of consistent growth in the CSM business is quite encouraging. But management has guided for a soft h1 fy 18.

Capex announcement of close to 400 crores gives comfort about business prospects.

In the near term the key to watch out would be the first half results which the management has indicated would be soft. Any positive surprise on this front could be interesting.

Another risk factor could be pressure on its leading product nominee gold due to competition coming up. And the higher tax outgo during the year fy 18 would also affect earnings for the year on a comparative basis.

Regulatory risks remain for companies involved in exports and that applies to PI too.

Technically since past few weeks, levels of around 800 are offering support during declines. Another interesting level to watch out for is its earlier high of 787 posted back in April 2015. Here the change of polarity principle could come into play where the region of earlier resistance/top will act as a support once stock price crosses it convincingly and suffers subsequent mild declines. In this case, the stock price crossed earlier top level of 787 in Aug 2016 and has been consolidating above these levels barring the brief dip during the demonetisation time correction in Nov 2016 to levels of 730-750 from where it quickly bounced back. I would be keenly watching the levels of around 780-800 and how the stock prices behaves around these levels. Strength would be back once it closes consistently above 830-35 levels.

Respected VP members,

I came across this article that talks about the dismal situation in the Agricultural sector. Any views on what it may mean for PI?

I suggest you don’t read too much into the political articles and then use that as input for investing, especially in agriculture. This forum has majority leftist articles and anti-establishment. Believe them at your own expense for investing

Sure Sir. My decisions for investments are irrelevant. You seem to have dismissed the article as political, fair enough.

Allow me to humbly elaborate:

I understand that rural indebtness is nothing new but the author points to the effects of demonitisation and cattle trade restrictions on the rural economy. These are relatively new variables in the mix. I felt they merit a deeper look as the fate of the rural economy and PI are joined at the hip. This esteemed forum is notoriously famous for brilliant minds paying attention to every detail, ergo the post.

true, whole noise about crisis in agri economy is motivated. Even during the best of times, some agri areas will have stress due to various factors not under the control of the govt. It is absolutely frivolous argument that cattle trade restrictions are aggravating the crisis. IMO, fair price of cattle is a safety net for many small and marginal farmers. I find it funny that all these same knowledgeable folks don’t prescribe free trade of agri produce so that farmers can get the market prices. Abolition of APMC is taking ever. I am absolutely against loan waivers since the problem is realisation of produce not the debt itself. PI as an agri input company will be hugely benefited from the movement towards market based prices which will incentivise farmers to look for productivity enhancing ways. This govt. is committed towards moving towards the same and hence the case for bullishness here but only in the medium to long term.

I believe we run a risk of distraction while reading too much news (already biased left or right) and noise. There have been excellent posts by Abhishek and Hitesh few days back in this thread highlighting the business prospects, risks etc. Suggest to go through them.

Thanks dada for good writeup. I went through investor presentations/AR of Bayer/BASF (global and Indian) and following are some additional interesting points ->

Total R&D spend is at 8bn$ in AgroChem space and it is lower compared to 150bn$ in Pharma space. Bayer spends 1bn euro on R&D crop science division and has 5600+ R&D employees in this segment. PI’s pharma initiative is at due diligence phase and I’m looking forward to more developments in this space.

Bayer states that research is carried out in few centrally located, dedicated sites - most of them in Germany. A lot of new partnerships with German universities are mentioned in AR. The development of products, plant breeding and trait development happens at numerous regional self and partner sites. This is the part where PI comes in I suppose.

Sale of crop protection products decreased worldwide in CY15, CY16 whereas high-value seed market increased in these years. Bayer is projecting growth of 1% in it’s crop science business. There seems to be very high channel inventory of crop protection products in Brazil and Bayer might take hit of 300-400mn Euros in CY17. PI’s conference call mentions that some of this inventory might be cleared in the second half of CY18 and global demand might increase.

In CY16, Bayer started field studies for 4 New Molecular Entities (NMEs) and 1 plant trait. The company aims to start field studies for 3 NMEs/Plant Traits/Biologics. It would be interesting to watch the order book size and number of molecules on PI’s side. (Current - 1bn$+, 8-9 molecules)

Regards,

Rupesh

Disc - I have been holding PI for 2 years and have increased my position in last 30 days. This is not a buy/sell recommendation. Investors are advised to do their own due diligence before investing.

What in God’s name is wrong with PIIND- the stock price? Why is it battered and bruised thus? Why is it singled out amongst other Agro chem companies, in the past 3-6 months? Despite positive developments and a good monsoon expectation, PIIND is just making new lows. And that too with low volumes. It is close to Nov 2016 lows, and that had happened when the entire market had plunged. But why now?

What do you make of this Mr. Hitesh. Please throw some light on this.

I am looking for a subjective answer here. I have all the financial nos. and development information, that is available, on google / AR or Con call transcript.

In the shorter term markets are obsessed with quarterly nos and immediate concerns. Once the management commentary about a soft h1 was out markets have been jittery about PI Inds and its immediate prospects. I guess some nervous investors are dumping the stock. When a lot of stocks in momentum are going up its very difficult for short to medium term investors to keep holding stocks like PI which are weak and dont move in tandem with markets. At some point long term investors would come around to support prices.

This is the reason why investors need patience and conviction to hold on to positions inspite of adverse price movement, more so when all other stocks are going up. I guess one has to take the portfolio approach where out of 10-15 stocks if one or two stocks dont move or go down and others go up. At least thats what I do. Bajaj Finance makes up for all other laggards in the portfolio. As long as the PF value goes up I dont worry about individual stocks going down or nowhere. For me as put before, the long term picture of PI remains clear and hence its a hold for me.

Brother in market stock has it’s own time to move.its nearly impossible to say why it’s not moving even though pi fundamental is rock solid . My observation its growth as slowed down from 30% + to 15-20%. So it’s not a hot stock now.Moreover it’s a huge winner for last few years and waiting for valuation to catch up with the earnings. It’s a time correction and it is painful. If u can’t bear the pain it’s better to run and buy a new stock .

It is indeed more frustrating to see PIIND languishing especially when the markets in general and other Agrochem stocks are making new highs.

You are spot on about the PF approach, provided all the 10-15 stocks have an almost equal weightage. The problem in my PF is over exposure of PI ( was 40% which has now been reduced to 30%). And it’s still not a healthy weightage. So despite all stocks doing well, my overall PF is not outstanding. To that add the frustration of so many good opportunities I let go, by clinging on to PI, for over a year and a half. I do have the conviction about a better future for PI,as all recent developments will only add in making PI an even better investment case, but erosion of profit since a year is making me jittery. And it seems extremely stupid to sell just because the stock price is going down.

If you’re referring to revenue growth…Well, just so you know, it has dropped from 30+ to 8 something levels.

And as for ,“it’s impossible to say why it’s not moving…”, I know that. But as Mr. Keynes has rightly said, " Successful investing is anticipating the anticipation of others", I was trying to get that idea from Mr. Hitesh Patel, as I felt he was the right person to approach.

In general I agree with Hitesh about PI. But it is still surprising that in a bull market like this it is simply not moving when every other stock is racing ahead. Market has its own whims and fancy. Stocks like Ajanta / PI are just not moving despite solid fundamentals. May be in 6-8 months time it will move

It is true that PI is not performing in this bull run. At the same time it may not go down much as those who are holding are doing so because of its future prospects and fundamentals. So I am using it for parking funds along with Gruh and HDFC bank!!

As long as the PF value goes up I dont worry about individual stocks going down or nowhere. For me as put before, the long term picture of PI remains clear and hence its a hold for me.

As long as the PF value goes up I dont worry about individual stocks going down or nowhere. For me as put before, the long term picture of PI remains clear and hence its a hold for me.