Thanks Bhavesh for this…then it leaves the high crude prices as the culprit…the company plans to expand capacity and has passthru of the increase input prices to clients…its looking to further diversify in sepciality chems. 236/220/200 are good entry points.

2 Likes

Good set of numbers by Philips Carbon as expected -

- Sales - 12% growth QoQ and a 46% YoY.

- Gross Margin is absolutely flat at 36-37% with net margins settling at about 12% - its flat QoQ and improved by approximately 400 basis points YoY.

- Debt on books are reducing at a slow pace while the capital investment into the new plant is at about 125 Crore for the half year - the cash generated from operations is getting reinvested into the business.

The quality of balance sheet remains robust with really good management of debtors, inventory and Payable balances.

Link to result is below:

Disclosure: Invested and added during the recent fall.

AJ

1 Like

Phillips carbon has reported mixed set of numbers during the current quarter -

While the top line is growing steadily with a QoQ growth of 7%, gross margins has reduced by about 380 basis points. The full year EPS is expected to be in excess of Rs. 24. Current PE along with the dividend of Rs. 3.5 declared during the current quarter continues to give relatively good valuation comfort.

See the results: Q3 2018 Results

Disclosure: Invested and hold a positive outlook on the long term prospects.

AJ

1 Like

Why is the stock correcting by 20% with such good results ?

Results were ok, not good. Volumes didnt grow. EBITDA/tonne decline slightly qoq.

Stock falling as Fidelity Investments selling…they hold 2% in the company

3 Likes

Friends, I have a some basic question to understand this company and sector well

- Should we consider this business as a commodity business and hence cyclical?

- What is the fair valuation of this sector and this company in particular?

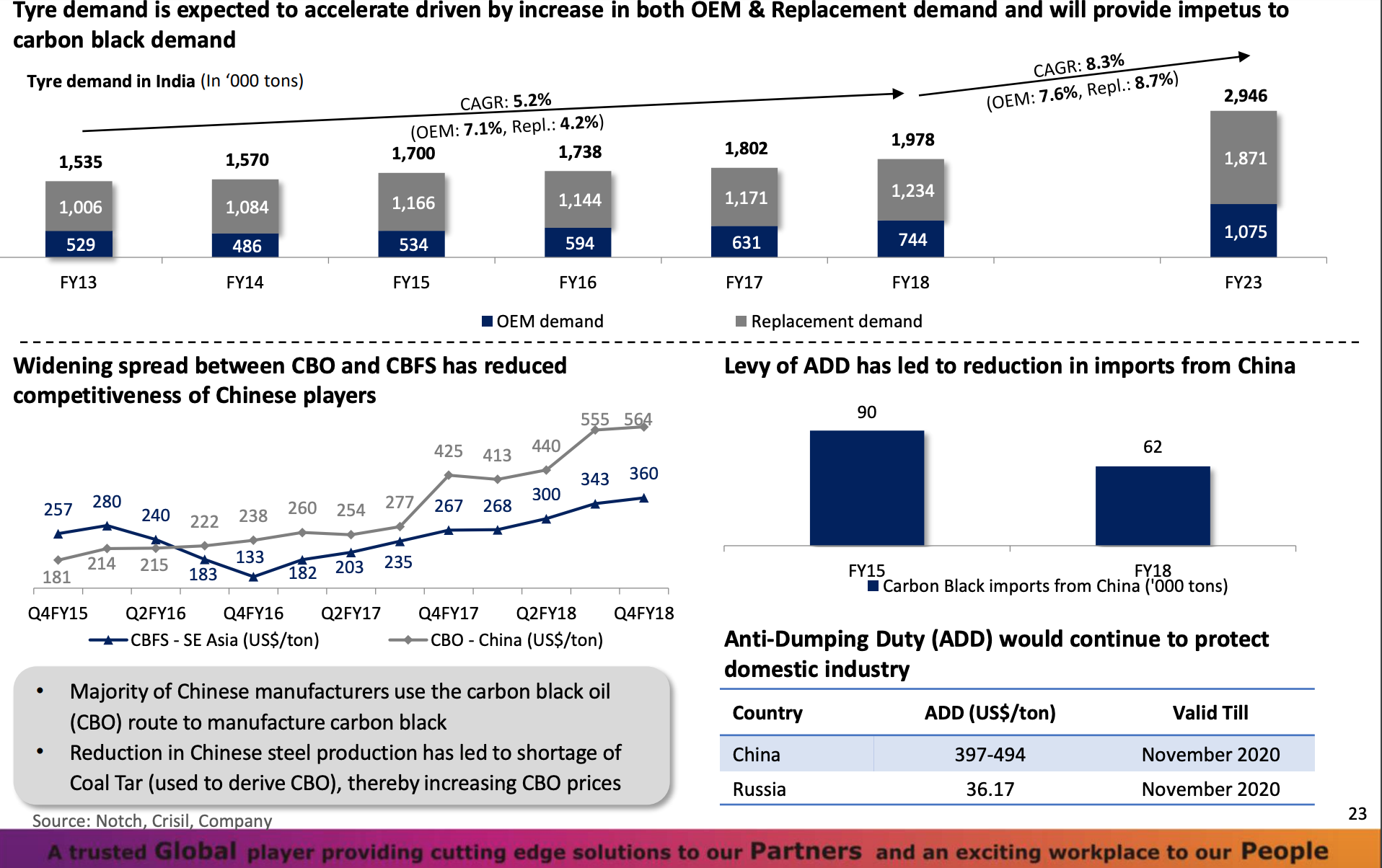

I was researching this sector and came across the anti-dumping duty on Carbon black

It looks like the dumping duty was extended for a period of 5 years in Oct 2015. Last year both tyre companies and rubber companies had kicked a fuss asking the govt. to remove the anti-dumping duty on carbon black

This duty has been in existence now for a long, long time and I think it will not be extended anymore.

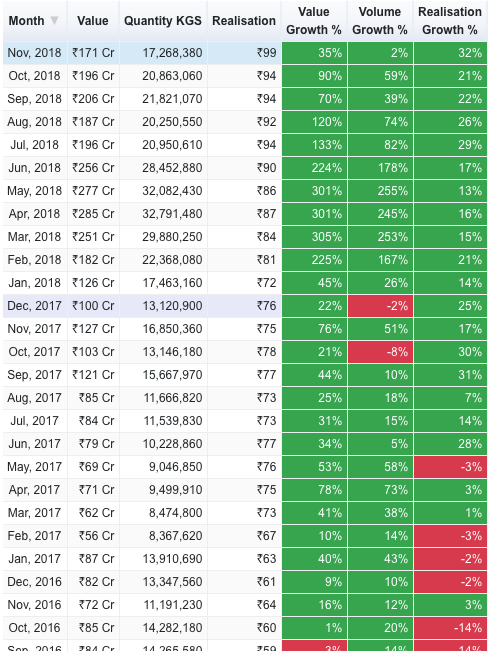

This is the import data for carbon black.

There appears to be reduction in growth in the volumes for the first time in several months. You can see the manic rise in volumes around the time the above two articles were published last year (Jan-Jun '18). Nov numbers could be indicating early signs of slowdown in tyre industry and this could be the reason for the de-rating in this cyclical commodity stock. The real slowdown will happen in Q4 and Q1 on the big base of Jan-Jun '18, coupled with the slowdown in tyre industries. I believe market is factoring all this in because the good times might have peaked as of Q3.

Disc: Just researching

5 Likes

Please help me understand this - aren’t volumes flat because he is running at peak capacity; with the addition of new capacities at Mundra we should see pickup in volumes - right?

1 Like

Volumes should have been higher by 2-5%. He has not met his volume guidance in last two quarters. Q4 likely to be better- over 110 kt. However, key to stock price performance is margin (EBITDA/t). If they dont grow, i expect stock to remain rangebound

Interesting question. Initially, i had a view that this business should be in between commodity and cyclicals and should trade at 10-12 times one year fwd. However, now i feel its more of a cyclical where margins can fluctuate with demand supply dynamics . It sells 65% to tyres on cost plus mark up. The rest is a combination of spot and specialty products where demand supply can change gross margin contribution. Also, if domestic suply rises in tyre carbon black, the tyre companies can negotiate for lower margins. In Q1FY19, they negotiated with tyre companies and margin improved Rs3000/t . Similarly, the tyre companies can someday negotiate it lower.

1 Like

While he may be a industry leader and pat for him to be bullish on his product line…sharing the article on his view of tyre demand going in fy20

Phillips Carbon has given very high profit compared to Dec 2017. Is this not enough to value this stock? Sales is also 50% up. What else should we look for when selecting a company. I was thinking high Crude Oil can hurt it but it is doing well. Should not we pick it for investment?

Little cyclicality is in every sector. If there is little slowness in Tyre sector and still this company can produce so good result then why not. I do not think because it is Cyclical so we should not buy. Even then it is a great buy as even then it is producing very good number. Waiting for something else from you guys to look convincing. See, we should not miss great company. There are few only every time.

Desc: Just checking

Any update on Greenfiled expansion…in which state mangement decided…to put greenfield expansion…

and would like t know if there is any info on brown field expansion details…is it done? is it on progress…

Please help

2 Likes

Any thoughts, how much bussiness would reduce if ADD is not extended ? Or is the market pricing in an ADD extension ?

The spot carbon black prices have come off led by new plant of Balkrishna Industries and weak demand in tyre markets given auto slowdown. I dont think ADD will have a role to play. Markets pricing in weak margins in coming quarters due to lower realization, particularly in non-tyre cataegory

3 Likes

I think this stock has recently got re-rated and rightly so because of following reasons.

- Global and more importantly the Indian market headwinds in auto sector.

- This has started reflecting into the financials of the company with the PAT reduced to 64Cr. in Q1-2020. Though this is mainly due to inventory costs, it will be interesting to see how the financials pan out in coming quarters due to slowdown in industry.

- FY2019 Balance Sheet shows the steep increase in non-current borrowings from 164 Cr in 2018 to 270 Cr in 2019. Not sure what is this due to since Company has not yet started investing into new Greenfield Project and the recent de-bottlenecking was not supposed to have this effect.

- Cash component on FY 2019 BL has also gone down despite the strong performance in FY.

Further, I have few questions on how the Company is planning to fund the new Greenfield Capacity Expansion Project? This may further stress the BL.

Having said this, I see few positives:

- Dominant position of company in the Industry.

- Capable and experienced management to maneuver the Company through the upcoming challenges.

Any comments welcome.

3 Likes

Auto industry slowdown is because of 2 factors.

First and biggest is the liquidity crunch and NBFC crisis which mean Commercial vehicle, construction equipment, other vehicles bought with finance/lease is down in a big way.

Second, BS-6 due now in 5 months means inventory is being cleared.

This will pick up. Margins will remain under pressure for perhaps a few more quarters.

Finances may be stretched, plans may be delayed.