One who bought at that mentioned price must be walking to bank on empty truck.

Stock is going strong at Rs 254 near to 52 week high and have very long way to go.

Cheers

One who bought at that mentioned price must be walking to bank on empty truck.

Stock is going strong at Rs 254 near to 52 week high and have very long way to go.

Cheers

This stock is mostly driven by high operating leverage. The reports doesn’t mention much about risks.

Yes, agree. Basically, few catalysts working in syc for the company:

I would consider the following key risks & -ves for the long term

Potential increase in Crude prices - Going by the current global trend, I expect a good ramp-up in crude oil production, while demand growth may be muted. Crude prices would probably remain low at least for the next 12-18months which should aid the BL

Chinese Imports - Considering the current Anti-dumping duties are in place till 2020, no issues till then

Capacity Bottlenecks - Volume growth will be constrained by capacity bottlenecks and any stock upside would primarily be driven by BL growth. Current expansion plans don’t seem to very aggressive

Pls note that the article is grossly incorrect and misrepresents Philip Carbon’s PE; 25.3 is the PE on 12 month TTM basis as per EPS; Readers wud do well to conduct their own due diligence also rather then just relying on such articles,

Disc: Holding from 220 levels and 12.5% of portfilio

Dear Tarun, Current PE on TTM basis is around 26, but if I understood it correctly, the article refers the PE of 13 only to the FY19 estimated earnings. I am giving the relevant portion below. Please let me know, if my understanding is correct:

“We maintain a buy and assign a target price of Rs 868 with PE of 13 times FY19 estimated earnings.”

Disc: Invested

Dear Madhavi, You are absolutely correct. However the snapshot is not correct as it shows 40 as PE…the brokerage is giving 13 PE expecting EPS to double from current levels…my aplogies if i have misunderstood

Regards

Tarun

Thanks Tarun for the clarification. You are right, the snapshot mentions it as 40. Sorry, I did not notice that earlier.

The Investor Presentation says that their capacity utilisation is at 94%. They also mention that a brownfield expansion would increase capacity by 15% but I don’t see any timeline for it. Does anyone know when this capacity will be available? Without this capacity, won’t it be difficult for Philips Carbon Black to justify the current P/E?

Disc: Invested in Himadri Specialty Chemicals Ltd. which also manufactures Carbon Black.

These might be of help…I dont intend to sell the share anytime soon.

Thanks. The first link says that the capacity will be available in FY19 which is what I wanted to know. Btw, curiously enough, more people have clicked the RJ blog link than the first one (16 vs 2 as of now). Didn’t expect that sort of skew towards a stock recommendation site here on VP.

Sure np, Just to give you a tech perspective for investment, the share tends to hold out between 20/50 day EMA and 45 RSI over a 2 year chart…I am very basic investor and not remotely close to an advisor…pls use my pseudo bullish comments with a pinch of salt. Update further to 9/22- RSI 45 and 20 SMA would coincide with 770 as entry levels given markets doesn’t sell off significantly

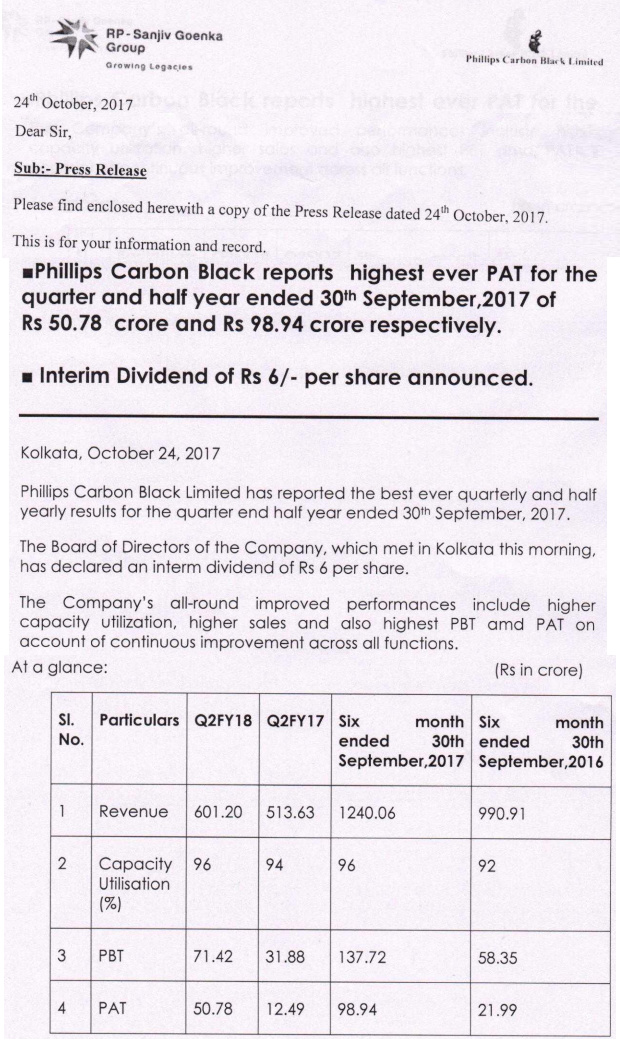

Phillips Carbon

Q2 FY18

Net Profit: 51 cr vs 12.5 cr (![]() 300%)

300%)

Revenue: 597.6 cr vs 460.7 cr (![]() 29.7%)

29.7%)

EBITDA: 94.6 cr vs 57.8 cr (![]() 64%)

64%)

argin (%): 15.8% vs 12.5% ( 330 bps)

EPS: 14.73 vs 3.62 (![]() 307%)

307%)

H1 EPS at 28.7 vs 6.38 (![]() 350%)

350%)

http://www.bseindia.com/xml-data/corpfiling/AttachLive/ba92e148-f7cb-4bdf-bc28-7dd8c8a50069.pdf

Strong results. Coal tar shortage in China currently given that it is diverted to make graphite. Now graphite is used in making lithiun ion batteries used in Electric vehicles. Chinese companies expanding lithium ion big time. Hence, carbon black prices on a structural uptick. Company well-poised to improve margins as it is also focusing on improving product mix in favour of speciality blacks. Lastly, FY19-only 11x PE.

Hi @bhavveshh

As per my understanding, coal Tar distillation process produces both coal tar pitch/CTP (used for graphite) & carbon black feedstock/CBFS (used for carbon black production). Not sure how more demand of graphite (and hence more production of coal tar pitch) will cause carbon black prices to rise since both CTP and CBFS will be produced more in simultaneously once more and more coat tar is distilled.

Can you please help in clarifying.

Coal tar distillation uses coal tar oil to produce Coal tar pitch and other chemicals

Now, there are two methods to produce carbon black - one which China uses is from coal tar oil and Rest or world uses carbon black feed stock (a derivative of crude oil distillation).

Now coal tar oil is also used to make needle coke (a raw material for graphite electrodes). So, lot of coal tar in China is also diverted towards making the needle coke given high demand and prices.

I hope i make myself clear