@ chirag bhai , 1.5 lakh shares?

lets hope phenix, kirby india etc goes public someday .

@ chirag bhai , 1.5 lakh shares?

lets hope phenix, kirby india etc goes public someday .

I’ve been closely tracking the company for a month now. Following are my takeaways:

I am upbeat on their Railways and Solar business. Both these divisions, combined, should grow at 16-18% CAGR over next 3-4 years. The question that arises is what after that? One probable answer is that Management continuously looks for new products and industry, so

Tubes and Pipes industry is in a cyclical uptrend. The guys like Tata Metaliks, APL Apollo, Sri Kalahasthi have had a good run and they are still expected to do well. So even Pennar will cash in on this opportunity. They are also increasing their addressable market by introducing stainless steel pipes.

The Pre-Engg buildings (PEBs) division can be a dark horse. It has potential to grow at 13-15% CAGR for 10 years, that’s the type of opportunity we are talking about. In India only 3-4% of commercial construction uses PEBs whereas in Western worlds nearly 70% of all new construction is via PEBs. So this can be a huge opportunity. And Pennar’s execution also seems good. While Everest Industries (Penar’s peer) did EBITDA Margins of 7-8% at its peak, Pennar did 13-15%. SO they are adding lots of value.

The Water Treatment and FUel Additive business also has gigantic opportunities. Both address the problems of pollution, which is a big focus area for the Govt.

All in all, I’m expecting strong performance from the company over next 3 years with sales growth of 14-15% CAGR and PAT growth of 25-28% CAGR. Valuing the company at conservative P/E of 14, I’m getting FY20 target of 120 which is 22% CAGR returns.

Key RIsk is that of increase in steel prices. In PEB business, company assumes the entire risk and price hikes are not pass through, that’s why we see so much volatility in their margins.

Another risk is that of cyclical nature of business. It is a proxy play on Infrastructure sector. SInce as of today we are in a recovery phase of capex cycle, it should perform well for 3-4 years, but post that exit should be timed well.

About the management: One of the key areas to look at. We met the management of the company ad they are really smar guys. They know their business in and out and try to stay ahead of the curve. They have a clear vision in their mind and despite so many divisions, they have not lost focus. Another credible part is that they are willing to face some loss if all the group companies are merged, since their combined stake will be coming down, but they are willing to take that.

SO I am positive on he stock with time horizon of 3 years.

Disc: Invested at 63-64 levels. 10% of Portfolio,

@chiragp @iamharsh does the management have plans to merge Pennar Inds and Pennar PEBS? From your post it does seems so. Can you please share the source of information. To me it seems odd. They hived off and listed PEBS couple of years back and now want to merge.

It’s been disclosed by the company itself that they want to merge the two entities . Check the announcements , I think it came out about 1-2 months back .

They even declared the swap ratios

@chiragp Thanks for the update. I missed it as am a shareholder of PEBS and didn’t find the announcement on BSE under PEBS.

@chiragp do you know why the promoter stake is reducing in the combined entity. Since the promoters own majority stake in PEBS (>60%, as per NSE) and PEL (51%), then how come the stake is reducing. Infact it should be increasing as majority of the new shares will be issued to the promoter(in proportion to shareholding). Seems I am missing something.

Also, can you please share if you know the date when shares of PEBS will stop trading and will get converted to PIL? Thanks for your help.

the date is not disclosed yet but they should complete it within a year.

yes, in the merged entity the promoter holding will get reduced due to cross holdings.

the promoter is aware of this fact and they are willing to go ahead with even though his holding is getting reduced. his view is that the synergies is far more greater than a little holding of his getting reduced.

Pennar is buy and forget compnay. It will do very well. Have some patience and faith in India

Pennar industries declared its results yesterday.

Each passing quarter we can see things improving.

Hold for long term to reap immense gains

Decent Q3 FY18 results by Pennar Industries.

Article on the Merger of its group companies

Thanks Niraj, can you share the pdf of the article, I am not able to access the entire article even after registering to the site.

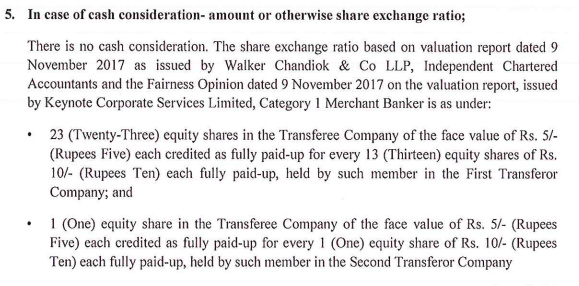

What is the swap ratio for PEBS with PIL. How much shares of PIL shall be received by shareholders of PEBS for each share held in PEBS.

@njain1983 Of the promoter stake of ~63% in PEBS, Pennar Industries (Parent Co) holds close to 54% and promoters directly own 9% in PEBS. Similarly in Pennar Enviro, promoters own 49% stake and the rest is owned by Pennar Industries. Hence after merger, the promoter stake in Pennar Industries is expected to reduce.

The record date for the merger isnt announced it and I guess will take a few months as the company needs to obtain approval from shareholders, NCLT etc.

Hope this answers your query:

The First Transferor is PEBS, the Second Transferor is Pennar Enviro and the Transferee is Pennar Industries

Please find the pdf of the same.

Pennar-Industries.pdf (65.5 KB)

I think Pennar industries has done well.If I look till operating margin level both standalone and consolidated level it has done well.standalone operating margin at 11.68% in q4 fy18 vs 9.97% q4 fy17.on consolidated front q4 fy18 operating marging at 16.94% vs 6.74%.There is exceptional gain in the quarterly result due to sell of pennar renewable. Intrest cost has increased, depreciation has increased ,capital work in progress is showing increased value. On standalone front other expense has increased a lot at 70.08 cr q4 fy18 vs 41.86 cr.Need to see if there is one off in other expenses.Tax incidence has almost doubled in standalone front. Remeber PEBS has performed badly on mar-2017 quarter.waiting for presentation and concall.interested on System projects,tubes,pebs and pennar enviro business rest are having great dependeny on steel price.All my ratio and stat from valuresearch or from earning release.

First the company did de-merger and than they merged the de-merged entity. I am somehow not comfortable with this… The company need a closed look and senior member in this forum are experienced enough to throw some light (on the foul play if any).

Disclosure : Not invested

Any updates from Concall if that has happened?

Disclosure: Invested at higher level.