One more thing- the amount held as fixed deposits in bank is being used as collateral for borrowings. How will the company borrow after the entire amount is used?

Regards

They claim to have realized 400 odd crores after the results. If you look at the mgmt presentation, this is what it says:

Cash and Bank Balance as on 31.03.2018 = 1491.47

Add : Subsequent realisation of export receivables= 416.91

Less: reserves for Buy back =424.00

Less : Amount required for margin money for leased gold= 300.00

Balance amount to be utilized for reducing liabilities and debt= 1187.38

1 Like

They also have inventory of Rs. 5161cr against which are the trade payables (gold loan?, as I understand)

Something is twrribly wrong somewhere… they have given clarifications. The auditor is good and has not resigned…at least not yet  The buy back process has commenced and the auditor has certified the creditworthiness of the company to undertake buy back. The promoters have said they will not participate in the buy back. The buy back price is like 275% of the current market price but the stock keeps falling. My guess is that with the reservation for retail investors (<2 Lac) the acceptance ration should come to around 15% for them. So if you were to buy 1000 shares today at the market price of 138 you will make money till 95. Ideally it should not go below that. But the way the thing is falling every day looks like it would reach two digit number in a matter of weeks. May the market is convinced that the Buy back thing is a ruse and will not be done and the numbers are just wrong and these guys will go out of business soon and promoters will run away. God knows…big mystery…this one!

The buy back process has commenced and the auditor has certified the creditworthiness of the company to undertake buy back. The promoters have said they will not participate in the buy back. The buy back price is like 275% of the current market price but the stock keeps falling. My guess is that with the reservation for retail investors (<2 Lac) the acceptance ration should come to around 15% for them. So if you were to buy 1000 shares today at the market price of 138 you will make money till 95. Ideally it should not go below that. But the way the thing is falling every day looks like it would reach two digit number in a matter of weeks. May the market is convinced that the Buy back thing is a ruse and will not be done and the numbers are just wrong and these guys will go out of business soon and promoters will run away. God knows…big mystery…this one!

2 Likes

may be a naive question but would like to know what is Balram Garg mean when he said " the gold on lease is around Rs.3,384 crores…" in the conf call?

Does it mean they have a debt of 3384 Cr along with regular bank loan of around 1000 cr?

Could anyone clarify please ? “Gold on lease”

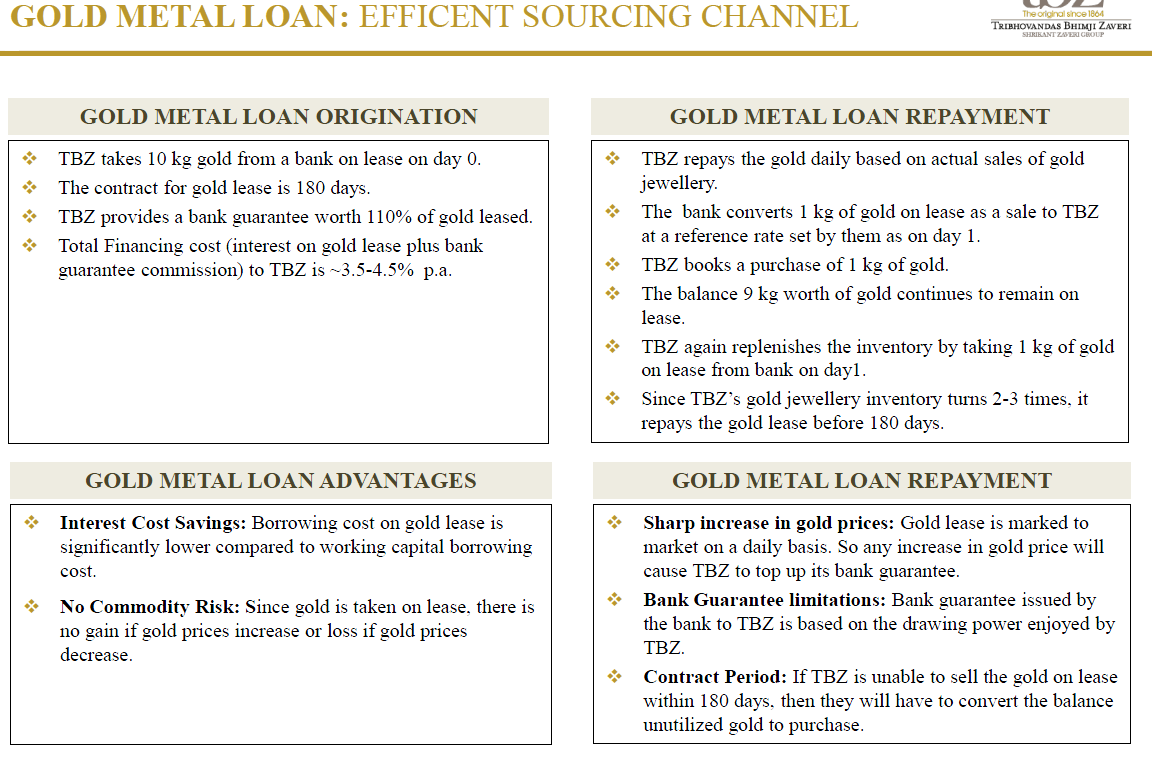

Yes- this is also a loan albeit with a lower interest rate (approximately half) as compared to a standard corporate loan. Through Gold on Lease the jeweler need not hold the inventory. This provides a natural hedge and of course the funding costs come down. You can find more here https://www.business-standard.com/article/markets/revival-of-gold-on-lease-to-benefit-titan-pc-jewellers-more-115021900888_1.html

1 Like

It must be reflected as inventories on the asset side. Else how do you balance. What are the 5161cr of inventories?

Not holding inventory here means that the Jeweler does not need to have the “physical inventory” as in the actual gold metal. And hence is not exposed to the vagaries of fluctuating gold price with the associated currency risk and the corresponding gain or loss on inventory valuation .They get access to gold (for their needs) but they do not need to own it- Own Vs Lease. As per them they need to provide like 10% as margin money as collateral for this access- so about 300 Cr for this 3384 Cr of “Gold on Lease” plus the interest at lease rates

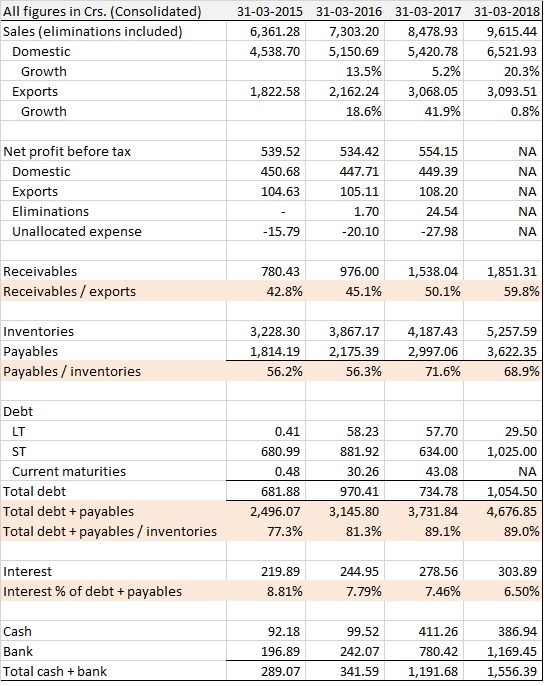

Updating my earlier sheet. Nothing much to note except export growth has fallen substantially which as per management is because of tax in UAE and business will degrow further. Receivables have shot up to 60% of export sales but management has noted that 417crs have been received. So adjusted for that % is ~47%.

If you go through the presentation which is quite exhaustive and the call which sounded genuine to me, the stock is at more than mouth watering levels. Just need to see the buyback executed and debt repaid. There is double to be safely taken home here.

3 Likes

I was thinking as the end date (July 13) for BuyBack offer acceptance by shareholders is approaching the stock would start moving up- the record date should hopefully be soon thereafter.

But the stock price is only going down and now CRISIL has downgraded the long term rating to ‘CRISIL A/Negative’ https://www.crisil.com/mnt/winshare/Ratings/RatingList/RatingDocs/PC_Jeweller_Limited_June_29_2018_RR.html

May be this is going to touch double digit soon

Disc: Invested and buying in SIP mode

Could you pls clarify how did you arrive this date ? I’m not finding any related sources w.r.t buyback date.

From the Postal Ballot Notice seeking approval of Members for the Buyback of Equity Shares. https://www.bseindia.com/xml-data/corpfiling/AttachHis/a0e5bc08-a04a-4c59-be4e-5e4a620f0f65.pdf

"Based on the Scrutinizer’s report, the result of Postal Ballot will be

announced by the Chairman or in his absence by the Company Secretary

on or before 5:00 P.M. (IST), on July 14, 2018 at the Registered Office of

the Company. The resolution, if passed by the requisite majority, shall be

deemed to have been passed on the last date for receipt of duly completed

Postal Ballot Forms or e-voting i.e. July 13, 2018"

Sorry! that’s not the buyback date. That is the date for announcing the result of ballot, seeking approval for buyback. Once the majority of shareholders votes for buyback, then the company will announce the date for buyback.

That is exactly what I had said- “the record date should hopefully be soon thereafter”. I never said Buyback date

Hi fellow boarders. Is this a good time to enter with all risks priced in?

Any buy back could further reduce purchase price to Rs110 assuming 10% acceptance ratio. Many of its competitors are knocked out such as Gitanjali, Nirav Modi and a number of regional players. There is a definite brand perception with gold jewels for purity and for PC Jewels this will only grow with its size and network effect. There is also GST effect and move to organized which could benefit listed players.

This is the only competitor to Titan at present.

My trigger for rerating will be:

1)a marked improvement in ROE

2) zero export sales as I have a feeling exports are just a means to launder money considering entities with high exports have always been shady like shree Ganesh and gitanjali

My current concerns with the stock in addition to the obvious CG issues are

- consistently reducing ROE every year

- reducing inventory turnover

- increasing debt

- reducing promoter holding

- high cash cycle of 150 days as compared to titan of just 50 days.

- some shady directors on board with no relevant expertise

The biggest risk I see here is the risk of fraud as the gold is taken on lease. They can easily sell the gold and pay 3% as interest every year for gold that they do not have. Only way this can be confirmed is by auditors doing a thorough job. So we have to have a lot of faith on the auditors.

Is anyone ready to risk an exposure at this low price? Why and why not?

Gold metal loan works in the manner as stated in one of the TBZ investor presentation:

As per this if they are running the shop and selling gold jewellery then they wont be able to take on new gold to sell to customer unless the old gold payments have been done. So selling gold, dont payback the bank and keep paying 3% interest doesn’t seem to be feasible.

Disclosure: not invested neither interested.

2 Likes

Thanks for the useful info. It seems any gold that is remaining after the contract period needs to be purchased. So the company can’t pay only the interest and keep extending the lease.

Ratings update by CARE: http://www.careratings.com/upload/CompanyFiles/PR/PC%20Jeweller%20Limited-07-09-2018.pdf

Company posted some updates on Q1 performance.

Outlook: Negative

The outlook is ‘Negative’ on expectation of the liquidity pressure to continue which gets compounded with company’s

announcement of share buy back. The rating maybe revised downwards if the working capital requirement together with

the buy back plan put additional stress on the liquidity position. However, the outlook may be revised to stable in case

the company is able to ramp up its retail expansion primarily through franchisee route thereby, reducing overall reliance

on debt leading to an overall improvement in liquidity.