Company Overview

Business Model & Segments: Parag Milk Foods Ltd is one of India’s largest private dairy-FMCG companies, operating an integrated model from owning dairy farms to processing and branding consumer products. The company exclusively sources 100% cow milk (no buffalo milk), which it processes into a diverse portfolio of value-added dairy products. Parag’s flagship brands include Gowardhan (ghee, paneer, etc.), Go (cheese, UHT milk, etc.), Pride of Cows (premium farm-to-home milk), and Avvatar (whey protein and nutrition products). Its key product segments are Ghee and Cheese, which contributed ~31% and ~24% of revenue respectively in FY23. Together with other value-added products like curd and paneer, these core categories accounted for ~68% of revenue in FY24. The remaining revenues come from liquid milk (~9-10%) and skimmed milk powder (SMP) or other commodities. This emphasis on value-added products (VAP) is a crucial differentiator – about 68% of Parag’s FY24 revenue came from VAP, much higher than dairy peers (~30%).

Competitive Edge / Moats : Parag has carved out strong market leadership in its focus categories. Its Gowardhan brand commands 22% share of the organized cow ghee market (No.1 position) and “Go” is a dominant player in cheese with 35% share (No.2 overall in Indian cheese, and a leader in the institutional cheese segment). These brands enjoy high recall and customer loyalty. The company’s fully integrated supply chain is another moat – Parag operates India’s largest automated dairy farm (with 3,000+ Holstein Friesian cows) and has built a robust milk procurement network of 500,000+ farmers across key milk-producing regions. This ensures consistent raw milk quality and supply (100% cow milk). On the distribution side, Parag boasts a pan-India network of 29 depots, 6,200+ distributors, ~682 super-stockists and ~460,000 retail touchpoints, allowing its products to reach consumers nationwide. Such scale in procurement and distribution creates a high barrier to entry. Moreover, Parag’s heavy tilt toward value-added branded products (cheese, ghee, whey, etc.) gives it pricing power and higher margins than commoditized liquid milk players, creating a brand moat. Its investments in R&D (e.g. developing a 75-day shelf life paneer and India’s first native whey protein) also indicate innovation capability.

Revenue Breakdown: As noted, ghee and cheese are the largest contributors (together ~55% of sales in FY23). Curd and paneer add another ~13% (making VAP ~68%). Liquid milk is under 10%, while SMP and others make up the rest. Geographically, Parag began with a strong presence in West and South India (its manufacturing plants are in Maharashtra, Andhra Pradesh, and Haryana), but it has expanded into North and East. The company has significantly grown its footprint in Delhi/NCR, Rajasthan, Uttar Pradesh, and Madhya Pradesh in recent years. Exports have been a small portion historically, though the focus is largely domestic consumption.

Industry Tailwinds & Headwinds: Industry-wise, the organized dairy sector in India is benefiting from multiple tailwinds: rising per-capita dairy consumption, shift to branded dairy products (for safety and quality), and consumers’ increasing protein and health food intake. Analysts expect India’s dairy demand to grow steadily given population growth and westernization of diets (e.g. higher cheese use in fast food). Parag, with its niche in cheese (pizza chains, burger QSRs) and health products, stands to gain from these trends. Additionally, government support like the PLI scheme and export opportunities for high-value dairy (like ghee to Middle East) are positives.

However, headwinds persist: The biggest is raw milk price volatility, which is influenced by monsoons, fodder costs, and cattle health. In late 2022 and early 2023, a lumpy skin disease outbreak in cows and high feed inflation tightened milk supply, forcing procurement prices up ~20% and pressuring margins across the industry. Parag navigated this by raising product prices and was aided by its high VAP mix (premium product consumers are less price-sensitive), but a prolonged milk inflation could hurt volumes. Another headwind is competition from both organized players (e.g. Amul’s dominant brand presence, newer regional dairies) and emerging plant-based dairy alternatives in urban markets (almond/soy milk, vegan cheese), though these are niche currently. Lastly, macro factors like any regulatory price controls on milk (e.g. government interventions to curb inflation) or export/import restrictions can impact the business. In 2023, the Indian government considered importing dairy fat to cool prices – such moves can affect domestic dairy pricing. Overall, Parag’s strategy to focus on value-added premium products and build brand loyalty provides some insulation against commoditized competition and input swings.

|

Market Concerns & Credibility: A key overhang until recently was whether Parag’s management can be trusted to “walk the talk.” In the past, some promises (like reducing debt or launching certain products) were delayed, which hurt credibility. However, in the last 2 years management has largely delivered on guidance: for instance, they had guided in FY23 that EBITDA margins would improve by FY25 once milk prices normalize – indeed margins rose from 4.1% in FY23 to 6.3% in FY24 and ~7-8% in Q1 FY25. They also promised to bring down debt and inventory – by FY24 debt/equity fell to ~0.7× (from 1.2× in FY22) and inventory days dropped significantly. These actions have started rebuilding investor confidence.

That said, concerns linger around debt and leverage. As of Sep 30, 2024, Parag’s total debt was ₹648.5 Cr, slightly higher YoY. Its leverage ratios (Debt/EBITDA ~3x, interest cover ~2.8x as of FY24) are higher than some peers, which rating agencies flagged. The company has taken a positive step by approving a ₹161 Cr equity fundraising in April 2025 via convertible warrants to delever the balance sheet and fund growth . Key marquee investors (including Utpal Sheth of RARE Enterprises and a few HNIs) and the promoters themselves are subscribing to these warrants at ₹179/share, reflecting confidence. This infusion will immediately bring ~₹40 Cr (25% upfront) and the rest on conversion, helping reduce debt. Still, investors will watch execution of expansion plans – a failure to generate expected returns on the ₹400 Cr capex could strain finances again.

Regulatory/Macro Risks: In concalls, management has mentioned being vigilant about any government policy changes. For example, the government’s stance on exporting SMP can impact Parag – in years of surplus, export incentives might help clear inventory, whereas in shortage years the government could ban exports (as happened in 2022–23). Parag’s strategy is to focus on domestic branded sales so it is not heavily reliant on volatile export markets. Another macro risk is the geopolitical import ban – India bans Chinese dairy imports (since melamine scandal) which has minimal direct effect on Parag (they import certain dairy machinery, not products). Parag is more concerned with inflation and consumer demand: high food inflation can dampen discretionary dairy (like premium cheese consumption). So far, demand for its products has remained resilient even as retail prices climbed – evidenced by growth in FY25 despite ~5-8% price hikes on ghee/cheese. Industry analysts believe this resilience is due to a structural shift towards branded dairy and the relatively low share of wallet dairy occupies.

Execution vs Promises: Analyzing concall transcripts and investor presentations over 3-5 years shows a mixed but improving track record. For instance, management had been talking about reducing the commodity part of business and focusing on VAP since around 2018 – they achieved this (SMP went from 20% of sales to <5% now). They also spoke of expanding cheese capacity and launching whey protein in 2017-18, which they executed (whey plant commissioned, Avvatar launched in 2017, now ramping up). However, some targets were delayed: e.g. a few years ago, they envisaged crossing ₹3,000 Cr revenue earlier, but due to Covid and setbacks, that happened only in FY24. The good sign is in the last two years, guidance has generally been met or exceeded. In early FY24 concalls, management guided for double-digit revenue growth and margin improvement, which FY25 results delivered (9% revenue growth, margins up ~100 bps). They also promised to bring down debt/EBITDA below 3x – post the FY25 equity raise, this is on track.

Future Guidance: The leadership has set an aspirational goal of ₹10,000 Cr revenue in 4-5 years, implying ~25% CAGR. They plan to achieve this via the new capex (doubling cheese, expanding distribution from 4.6 lakh outlets to ~13-15 lakh by 2027, and new product launches in high-growth categories). While ambitious, this goal underscores a growth mindset. In assessing realism: a 25% CAGR is high for a dairy business, but Parag’s new categories (whey, premium milk) could indeed grow 25-30%, and cheese/ghee still have headroom in under-penetrated markets. The key will be execution and maintaining balance sheet health to support this growth. Most analysts view the ₹10k Cr target as aggressive but not impossible if everything goes right; they project slightly lower growth with FY26 revenues ~₹3,864 Cr as a base case. Management has not formally given numeric guidance for FY26, but commentary suggests expectations of mid-teens growth and margin improvement to ~8-9%.

Competitive Analysis

Parag Milk Foods operates in a highly competitive Indian dairy landscape. Key competitors include both cooperative giants and private firms:

- Amul (GCMMF) – the market leader (cooperative federation) with a multi-category dominance (milk, butter, cheese, ice cream, etc.). Though not listed, Amul’s scale (~₹55,000+ Cr turnover) dwarfs all others, and it holds the #1 spot in many segments (e.g. overall cheese >40% share, butter ~market leader). Amul is Parag’s main rival in cheese (Amul is #1, Parag #2 by share) and ghee (#2 after Parag in cow ghee, though Amul’s total ghee including buffalo ghee is larger). Amul’s strengths are an expansive milk procurement base and unbeatable cost advantages as a coop. However, Parag differentiates by focusing only on cow milk products (Amul sells buffalo milk products too) and by premium branding (e.g. Pride of Cows has no direct Amul equivalent). Competing with Amul requires niche positioning – Parag has done this in whey protein (Amul has none) and super-premium milk.

- Hatsun Agro Products – India’s largest private dairy company, focused mainly in South India (brands Arokya, Arun Ice Cream). Hatsun’s revenue (~₹8,667 Cr) is about 2.5x Parag’s, and it has an extensive distribution in South. Hatsun’s portfolio is more mass-market (fluid milk, curd, ice cream, cattle feed). It competes less directly in cheese or whey (a smaller player there). Hatsun’s strength is its vast chilling infrastructure and daily touchpoints (it collects ~3 million liters milk/day, similar order as Parag). Financially, Hatsun has been richly valued – it trades at ~70-75 P/E – reflecting steady growth and investor trust. However, its EBITDA margins (~8%) are not far above Parag’s, and its value-added mix is lower (Hatsun still derives a lot from commoditized milk). In fact, Parag’s 68% revenue from VAP is much higher than Hatsun’s ~30%, as noted. This suggests Parag, if it executes well, could potentially command better margins in future. Hatsun’s weakness could be its high valuation (not as much fundamental downside, but stock is expensive) and relatively higher debt. Parag’s weakness against Hatsun is geographic – Parag is under-penetrated in the deep south (Hatsun’s backyard), though Parag is making some inroads via modern trade.

- Heritage Foods – A prominent private dairy in South India (Andhra/Telangana base) with ~₹4,135 Cr sales. Heritage’s product mix includes milk, curd (they are a leader in packaged curd in South), ice cream, and value-added products (they exited the retail grocery business to focus on dairy). Promoter is the family of Chandrababu Naidu (CM of AP). Heritage competes indirectly; they are strong in curd and liquid milk in their region, while Parag is stronger in cheese/ghee nationally. Financially, Heritage has solid metrics: FY24 PAT ~₹188 Cr, ROE 20%, and P/E ~25-26, similar to Parag’s. Heritage’s EBITDA margins in FY23 were low (~4.3% due to high milk prices) but bounced back to ~7-8% by FY24 as prices were hiked (the company’s Q3 FY25 profit jumped 60% YoY). Relative strengths: Heritage has low debt and a focus on efficiency (they’ve consistently generated positive cash flows and pay dividends ~25% payout). Its distribution is strong in South but limited elsewhere. Parag versus Heritage: Parag has a broader national reach and more diversified product range (whey, cheese where Heritage has little presence), whereas Heritage has a deeper penetration in fluid milk/curd in its home market. Parag can be seen as taking a more FMCG-like branding approach, while Heritage, despite being listed in FMCG category, is closer to a pure dairy play.

- Dodla Dairy – A newer listed dairy (IPO in 2021) focusing on South India and some operations in Africa. FY24 revenue ~₹3,720 Cr, net profit ₹260 Cr. Dodla’s product mix is largely liquid milk, curd, value-added like flavored milk and ice creams in certain areas. It’s comparable in size to Parag and has impressed investors with high return ratios (ROE ~18%) and sound balance sheet (promoter holding ~60%, low debt). Dodla’s stock trades around 32-34 P/E, a premium to Parag’s, indicating the market’s view of Dodla as a stable growth play. Strength: Very strong procurement network in South, and they have managed milk price cycles well (maintaining decent margins even in tough times). Weakness: Less presence in high-margin products (cheese, ghee) – Dodla has mostly regional product lines and hasn’t built pan-India brands yet. For Parag, Dodla is more a regional competitor in southern markets for milk and curd; Parag’s opportunity is to tap those markets with its value-added products which Dodla doesn’t offer (like Parag could sell Go Cheese or Avvatar in South where Dodla’s presence is milk).

- Other Players: Mother Dairy (Delhi-based coop) is big in North for milk & ice cream, but not directly competing in Parag’s focus categories beyond dairy beverages. There are also smaller listed entities like Umang Dairies or KMG Milk but they are niche and far smaller (and KMG is primarily SMP focused). Internationally, multinationals like Nestlé and Danone have a presence in dairy segments (Nestlé sells Everyday dairy whitener, Milkmaid, etc., Danone had tried a yoghurt business) but Nestlé’s dairy plays are more in powders and infant nutrition, not direct competition to Parag’s cheese/ghee (except Nestlé’s Milkmaid vs Parag’s sweetened condensed milk, a small segment). Danone exited fluid dairy in India in 2018. New disruptors : there’s a surge of farm-to-consumer milk startups (Country Delight, etc.) in urban areas, and plant-based milk brands (e.g. Sofit, Oatly’s partners) catering to niche audiences. These collectively remain a tiny fraction of the $130+ billion Indian dairy market. Parag’s “Pride of Cows” is itself an answer to premium farm-fresh demand, and they have an early-mover advantage in that space with a loyal client base willing to pay ₹120/L for curated milk.

Competitive Positioning : Parag differentiates itself as a branded, value-added dairy foods company, often even labeling itself an “FMCG” company. It has more in common with an “innovation-driven dairy FMCG” like Nestlé or Amul, versus pure liquid milk companies. Its moats (high VAP mix, pan-India distribution, own farm) give it a niche that competitors are trying to build but haven’t fully replicated. For example, Heritage and Dodla now talk of increasing their value-added products and margins, something Parag started a decade ago. This is reflected in Parag’s revenue mix – 68% VAP vs ~25-30% for Heritage/Dodla. Even Amul, despite scale, derives a large chunk from liquid milk which is low margin; Parag’s 100% cow milk positioning also resonates with a segment that prefers cow ghee over buffalo ghee (Parag’s Gowardhan is purely cow ghee, giving it a marketing edge as “healthier”).

Market Share & Growth: In ghee, Parag is #1 in branded cow ghee (22% share), but if we include all ghee (including buffalo), it still competes with Amul and others in a fragmented market. In cheese, Parag’s ~35% share is substantial; only Amul is ahead. In fresh products (curd, milk) its share is small nationally, as those are dominated by local coops (like Nandini in Karnataka, Verka in Punjab, etc.). So Parag focuses on markets where organized share is rising – e.g. western paneer and cheese usage is growing at >15% CAGR in India. Parag’s strategic risk is relatively narrow breadth: it has bet big on a few categories (if, say, consumer preference shifted away from dairy ghee due to health fads, Parag would need to adapt quickly). But it is somewhat hedged by having a foot in emerging categories like whey protein and even exploring dairy alternatives via Pride of Cows’ organic play (though not plant-based, it caters to a similar health-conscious demographic).

Strengths vs Peers: To summarize: Parag’s strengths are high-margin product portfolio, strong brands in niche categories, integrated operations, and improving financial metrics. Peers like Hatsun and Heritage, while larger in milk, do not have the same dominance in cheese or whey. Parag’s R&D and product innovation (whey protein, long-shelf-life paneer, etc.) also set it apart from many traditional dairies that stick to basic products. Moreover, Parag’s national reach (especially in West, North, and parts of South) gives it a larger addressable market than say Dodla or Heritage which are region-specific (though Heritage is now selling ghee nationally through modern trade).

Weaknesses vs Peers : Parag’s weaknesses historically were financial discipline and consistency. It had higher debt and past losses, whereas a peer like Dodla has been consistently profitable and prudent (market rewards that with higher valuation). Also, Parag lacks the absolute scale of Amul/Hatsun in milk procurement, which can lead to higher input costs at times (coops have pricing advantages). Another area is ice cream and fresh products – Parag doesn’t have a big play in ice cream or flavored yogurt which are fast-growing segments some peers (like Hatsun’s Arun Ice Cream, Amul’s ice creams, Mother Dairy’s yogurts) are capturing. Parag may need to broaden its product basket or risk ceding those segments. Lastly, new entrants risk: While brand loyalty is a moat, the success of any new venture by bigger players (e.g. if Amul aggressively pushes whey protein or if a multinational introduces gourmet cheese at scale) could challenge Parag’s share. So far, Parag’s first-mover advantage in certain categories has held up.

Overall, Parag sits in a sweet spot of the market – not as large and stable as the cooperatives, but faster-growing and more innovative than many mid-sized peers. If it continues to execute well, it can capture a good chunk of the premiumization trend in India’s dairy sector. But it must also be wary of the cooperative behemoths expanding into value-added (Amul has announced plans for high-end cheese and whey in future) and ensure it maintains its quality and brand edge.

Valuation Analysis & Investment Perspective

Peer Comparison – Valuations: Parag appears cheap to fairly valued relative to peers, depending on which peer:

- Hatsun Agro (much larger): Trades at 70-75× P/E and ~12× P/B. Its EV/EBITDA is ~30×. Investors have historically accorded Hatsun a premium for its leadership and steady growth, but this gap is huge. Parag at <1/3rd the P/E of Hatsun looks inexpensive – albeit Hatsun has a longer consistent track record.

- Heritage Foods: P/E ~25.7×, P/B ~4.7×. So Parag’s P/E is similar, but Parag’s P/B is lower (Heritage has higher ROE ~20% vs Parag’s ~12%, hence higher P/B). EV/EBITDA for Heritage is ~14× (as per recent data), a bit above Parag’s ~12×. This indicates Parag is priced roughly in line with Heritage on earnings, despite Parag’s faster growth recently. Heritage’s advantage is a cleaner balance sheet (almost debt-free) and dividend payouts, which justify parity.

- Dodla Dairy: P/E ~33×, P/B ~6×, Mcap/Sales ~2.3×. Clearly, Dodla is valued at a premium to Parag. Dodla’s higher ROE (~18%) and consistent profits likely drive that. If Parag can reach similar ROE levels (which requires margin uptick and debt reduction), one could argue its P/E could move closer to Dodla’s. Currently, the market is giving Dodla a quality premium.

- Valuation summary: Parag is one of the cheapest in its peer set on sales and EBITDA multiples, and about average on P/E. This perhaps reflects that Parag’s earnings have just recovered – the market may be in “wait and see” mode before rerating it. For a long time, Parag traded at a discount due to governance concerns; that discount is narrowing as performance improves.

Valuation vs Growth Prospects: Does the current price factor in future growth? At ~24× earnings for ~30% PAT growth (FY25 vs FY24), the PEG is <1, which often signals that growth is not fully priced in. If Parag achieves even a 15-20% EPS CAGR over the next 2-3 years (conservative relative to its guidance), the forward P/E would drop quickly. For instance, brokers estimate FY26 EPS around ₹14; at current price, that’s forward P/E ~16-17×. That would be cheap given the sector. HDFC Securities in an Oct 2024 note had a Buy on Parag with base-case fair value of ₹251 (and bull case ₹273), when the stock was ₹227. They cited Parag’s dominant VAP share and new businesses growing ~25-30% as justification for multiple expansion. This indicates some analysts see upside from current levels as the market gains confidence.

However, it’s important to consider risks in valuation: The stock’s run-up (from ₹60 in mid-2022 to ₹230 now) means a lot of the “turnaround” is already reflected. The next leg (towards ₹250-300) likely requires proof of concept on expansions and margin enhancement. If, for instance, milk prices spike unexpectedly or the new capex yields lower ROI, Parag’s earnings could underwhelm, and the market may not reward it with a higher multiple.

EV/EBITDA vs Peers and History: Parag’s EV/EBITDA ~12× is reasonable given it’s around the industry average (Heritage ~14×, Dodla ~18-20×, Hatsun ~30×). Historically, when Parag was struggling (FY21-22), its EV/EBITDA was very high (due to low EBITDA). Now that EBITDA has normalized, 12× is not demanding for a company expected to grow EBITDA ~20% annually. As debt reduces (with warrant money) the EV will come down or EBITDA can be used more for growth than interest, both positive for this metric.

Margin of Safety : In assessing margin of safety, one can look at Parag’s asset values and book. Book Value per share is ~₹85.7. The stock is ~2.8× book, which on the surface isn’t “deep value” cheap. But consider that replacement cost for a company with three modern plants (cheese, UHT, whey facilities) and a large farm would be significant. Also, Parag’s brands (intangible assets) are not on the balance sheet. So book value likely understates intrinsic value if the business stays healthy. The margin of safety thus lies in the business quality improving: if Parag sustains profits, it should trade more like an FMCG brand company (which often trade 4-5× book, PEG >1). There is a sense that Parag’s current valuation does not fully price in its growth plans (like doubling cheese capacity, etc.), perhaps because the market is waiting to see execution. This provides potential upside if execution is on track. Conversely, if things go wrong, the stock could de-rate; but with the promoter/funds infusion, the downside is cushioned by improved fundamentals (e.g. bankruptcy risk is off the table now compared to 2020 when pledges were high and losses incurred).

Comparative Valuation – Cheap, Fair, or Expensive?: On a pure valuation basis, Parag appears reasonably valued to slightly cheap relative to its peer group and growth outlook. It is definitely not priced for perfection (unlike, say, Hatsun which is expensive). There is arguably a valuation gap between Parag and high-quality peers like Dodla/Hatsun – if Parag continues to prove itself, that gap could close (meaning upside). If one compares Parag’s EV/Sales (~0.9×) to FMCG companies of similar sales (~1x or more for even food companies with lower growth), Parag seems modestly valued. The market likely still factors in some risk premium (or rather, a lack of full confidence) – which can be an opportunity if one believes those risks are now lower than before.

In summary, at current levels Parag’s valuation multiples are in the mid-range – not a deep bargain like it was at ₹60 (when fear ruled), but not stretched either given its growth trajectory. The stock’s re-rating from a P/E of sub-10 in 2022 to ~24 now reflects improved fundamentals. Further re-rating to, say, 30x would hinge on delivering a couple more quarters of stable growth and hitting guidance. If that happens, current price could look cheap in hindsight. Conversely, any slip could keep it stuck at these multiples or lower. Thus, there appears to be a reasonable margin of safety as the business has momentum and the valuation does not overly reflect best-case scenarios.

** Conclusion & Investment Rationale**

Final Assessment – Buy, Hold or Avoid? Given the comprehensive analysis, Parag Milk Foods emerges as a cautiously optimistic BUY at current prices , with a medium-to-long term view. The company has navigated through a rough patch and is now on a stronger footing: profits are at all-time highs, debt is being pared down, and new growth engines (cheese expansion, whey, premium milk) are revving up. Its competitive advantages in value-added dairy and brand leadership in key categories provide a solid platform for continued growth. At ~23-25x earnings, the stock is not overpriced relative to peers and growth prospects; in fact, it trades at a discount to the sector leaders, offering scope for upside if execution stays on course.

That said, this is not a risk-free story – thus the optimism is cautious. We recommend a Buy for investors who understand the dairy industry cyclicality and are willing to monitor the company’s quarterly progress. For those already invested from lower levels, it could be a Hold to ride the growth, as many positives are unfolding but one should keep an eye on risk factors discussed.

Key Upside Triggers: There are several potential catalysts for Parag’s stock in the coming quarters:

- Earnings Surprise: If Parag delivers higher-than-expected earnings growth (e.g. via margin expansion to ~8-9% EBITDA or >20% revenue growth from new products), the market could re-rate the stock upwards. The next few earnings releases (Q1 FY26 on July 17, 2025, and subsequent quarters) will be critical. A strong festive season in Q2 and successful pass-through of any milk price fluctuations in Q3 could boost confidence.

- Deleveraging and Interest Savings: As the ₹161 Cr warrant money comes in (25% already in, rest over 18 months on conversion), debt should reduce by a similar amount. This not only saves interest costs (improving net profit) but also improves net debt/EBITDA, potentially leading to credit rating upgrades. A better credit profile can reduce borrowing costs further and free up capital for growth. Any announcement of significant debt reduction could act as a positive trigger.

- New Product Launches or Partnerships: Successful launch of, say, a new high-protein snack line under Avvatar or expansion of Pride of Cows into new cities could drive incremental revenue and garner market enthusiasm (as it signals Parag tapping into health-food trends). Parag has hinted at new product categories – concrete news and traction on these will excite investors. Additionally, any strategic tie-up (domestic or export) – for example, a co-branding with an international cheese brand or a large QSR contract for supplying cheese – could provide upside surprise.

- Sector Tailwinds / Milk Price Softening: If India sees a strong flush (surplus milk production) in late 2025 leading to stable or lower milk procurement prices, it would expand dairy companies’ margins. The entire sector might rally on that news. Parag, now more efficient, would benefit disproportionately from a benign raw material scenario. Conversely, if milk prices unexpectedly cool down (e.g. due to a good monsoon and fodder supply), Parag’s margins could overshoot estimates.

- Market Re-rating of “FMCG” Dairy: Parag’s efforts to reposition as a branded foods company might eventually win it a higher multiple. If the market starts valuing Parag closer to an FMCG stock (on par with say Nestlé’s dairy business or even Hatsun’s premium), there is considerable upside. This would likely be triggered by a string of consistent results and perhaps achieving a ROE north of 15%.

Downside Risks & Triggers: On the flip side, a few developments could trigger downside:

- Spike in Milk Prices: Any supply shock (poor monsoon, disease outbreak) causing milk prices to spike significantly without immediate pass-through could compress margins and spook investors. A repeat of the situation in early 2023 (double-digit milk inflation) would be a short-term negative for all dairies including Parag.

- Execution Delays/Cost Overruns: If Parag’s capex projects (cheese plant expansion, new farm) face delays or come in over-budget, the expected growth might be deferred. For example, if doubling cheese capacity drags into 2026 instead of 2025, revenue targets could slip. Similarly, if Avvatar’s new product foray doesn’t gain consumer acceptance, the high growth forecast for that segment may not materialize – hurting credibility.

- Governance or Compliance Issues: While none are anticipated, any surprise like an accounting irregularity, large legal liability, or regulatory penalty can harm sentiment quickly. Investors will watch how the ongoing defamation suit and FSSAI appeal conclude – an unfavorable outcome (though unlikely to be material financially) could still modestly dent the company’s image.

- Macro Slowdown: Dairy is relatively resilient, but a broad economic slowdown reducing consumer spending could impact premium product growth. If consumers down-trade to cheaper local brands or loose milk in tough times, companies like Parag might see volume pressure in some categories.

Margin of Safety Consideration: At the current price, we find there is a reasonable margin of safety built into Parag’s stock for a long-term investor. The downside appears protected to an extent by the company’s tangible progress (it’s unlikely to revisit the distress valuations of 2022 unless a severe negative event occurs). The promoter and insider actions – increasing stake, participating in fundraise – provide additional confidence. With promoters owning ~43% and new savvy investors on board, there’s alignment in driving the share value up. Moreover, Parag’s assets (brands, facilities, network) give it intrinsic worth; even in a worst-case scenario, one can argue those would attract a buyer (providing a floor value).

In valuation terms, assuming Parag achieves even 8% net margin on a projected ₹5,000 Cr revenue by FY28 (which is below their aspirational goal), that’s ₹400 Cr PAT. Assigning a moderate 20× P/E would yield an ₹8,000 Cr market cap, roughly 3x the current – indicating significant upside potential. Even haircutting those assumptions (say it only gets to ₹600 Cr EBITDA by then and stays at EV/EBITDA ~12×), the EV would be ₹7,200 Cr minus debt – still about double current. These back-of-envelope figures suggest that the current price is not baking in the full growth story, hence a margin of safety exists if one is patient and the company executes reasonably well.

Investment Rationale : In summary, Parag Milk Foods offers a compelling play on India’s increasing appetite for value-added dairy and nutritional products. The company’s right-to-win lies in its integrated model, strong brands, and distribution might. After weathering storms, it has emerged leaner and more focused. For investors, the stock provides exposure to a quasi-FMCG dairy business at a valuation that is still catching up with its peers. The risk-reward looks favorable: risks (input costs, execution) are real but manageable, and rewards could be significant if Parag even partially meets its growth ambitions. With improving governance and professional management in place, the execution risk is mitigated relative to past.

Thus, for an investor with a 2-3 year horizon, Parag Milk Foods appears to be a “Buy” (accumulate on dips) for a potential re-rating and earnings growth story. Near-term, one can watch upcoming triggers like the Q1 FY26 earnings (mid-July 2025) and the progress updates on capacity expansion (perhaps in the AGM or investor presentation). Barring unforeseen events, Parag is positioned to milk the opportunities in India’s dairy evolution, and its stock could reflect that in the years ahead.

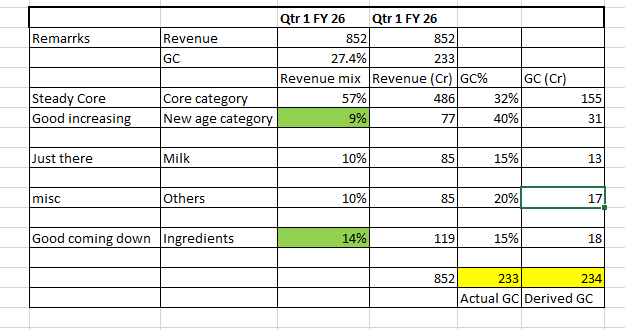

MOST IMPORTANT POINT : While like many FMCG companies Parag doesnt give financials for brand/category but given my FMCG experience and hearing their concalls my “guestimate” is as follows (I can be completely wrong )

If we think like owners or think like someone wanting to acquire their brands (remember they are No.1 & No 2 in respective core category of Cheese & Ghee ).Simply valuing these brands (Qtr 1 turnover 486 cr ) 1& New age brand (Qtr 1 turnover 77 cr ) ie 563 cr for Qtr1 ie annualized 2252 cr for CORE BRANDS and which are growing ,giving it multiple of 2-3 means 5630 cr Market cap only valuing brands WHICH DOESNT SIT ON BALANCE SHEET !!

If we further fine tune it and be technically right and use DCF calculation only for Core +New age category brands which is 2/3rd of the business and use the balance as Book value we arrive at valuation of 4281 cr which again is higher than market cap !

Discl.:Please do your own due dilgence .Views may be biased bcos of my investment .I am NOT sebi regsitered ,post is for educational purpose