This is such a well discovered company that the fundamentals aren’t being discussed here anymore. Here are some things I noticed with how this company has been evolving.

- RoE/RoCE has been improving dramatically of late. From the 40-ish levels in FY17, RoE is now nearing 50% and RoCE is in the mid 60s.

Even more amazing is RoE minus Investments + Cash which is over 60% in FY18 and I think it would be even higher in FY19.

This shows a what/if scenario when the company returns all the cash back to the shareholders. This is the best-case scenario of course, as the company will need to fund its growth as well. So the actual figure might lie between the RoE and this figure.

- In the recent quarter, the results were very interesting with the topline growing about 17% and the bottomline rising 46%. How did this happen?

I expected expansion in gross margins but that’s not the case here. What has happened is the employee costs are reducing and is at an all time low as a % of Sales.

Apparently the company is now outsourcing its manufacturing and that is showing great results to the return ratios pointed in #1.

- Capital turnover ratio is improving and is at all-time highs, again the reasons being outsourcing and better product mix and efficiency.

- Inventory turns are improving as well and at all time highs.

- Working Capital management is improving. Look at WC turnover ratio. I think it’s going to improve further in FY19 going by Q1.

- Company is throwing out cash like never before. Look at the changes in Working Capital in the cash flow of +68.96 Cr, for a company growing at a good rate. WC is reducing presumably due to outsourcing.

FCF is improving due to efficient management of WC

- Consequently, the balance sheet now has 285 Cr of Cash + Investments vs 73 Cr of the same in FY17.

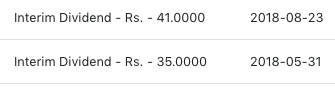

- The company has had a steady dividend paying history and has paid 141 Cr (42% payout) last year.

The build up in cash and investments is despite this payout. I get the feeling that the company needs to invest even lesser of its cash to keep its growth, because of improvements in its return ratios. That could explain the Special Dividend consideration coming up.

They have currently paid 84 Cr as dividend in this FY and there is possibility that this special dividend could get rid of a large part of the cash sitting on their balance sheet as they simply don’t need it. I think Rs.35 Interim Dividend and another Rs.50-70 Special Dividend is a possibility based on my assumptions on their payout history and the amount of cash they are going to need to grow.

- Recent entry into Athleisure and Kids segments is a big plus and expands the target market.

It looks like the company is setting itself up for continuing the good growth going forward, on an even more asset-light model, with even better products and distribution, all this on such a small equity base.

Risks:

-

Can they maintain the same quality with outsourcing?

-

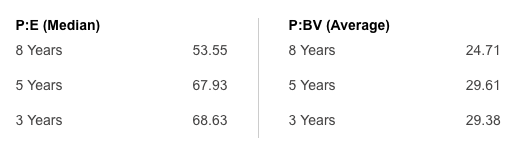

Valuations - This is the median P/E and P/B

Current P/E and P/B as of today is 86 and 39 and way, way above any of those numbers above. I think based on FY19E valuations, it is trading at around recent historic median valuations. The recent changes I presume are the reasons for this.

-

Myntra, Jabong and Amazon put brands that have non-existent distribution alongside established players which reduces the brand barrier.

-

Promoters have reduced stake slightly (49.01% to 48.32%) around Q1. This is a bit of a concern. FPI have however increased stake during the same period from 35.18% to 37.27%.

Disc: I have been building a decent position here in the recent fall after the run-up post Q1 results. The thesis is laid out above but if things change, I will change my mind.