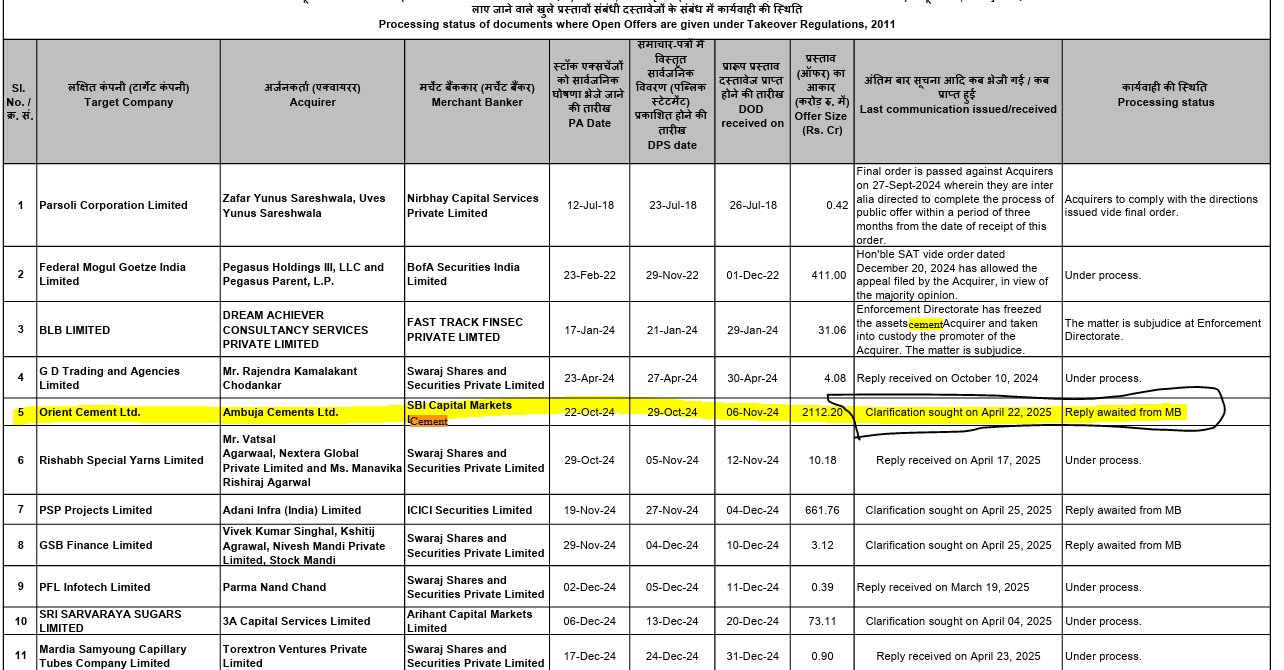

As of April 29, 2025, the status of the proposed transaction , Orient Cement Ltd., Ambuja Cements Ltd., and SBI Capital Markets Limited remains unchanged. A clarification was formally sought from SBI Capital Markets on April 22, 2025, and the matter is currently pending. The response from the Merchant Banker (MB) is still awaited, and no further updates have been provided on the SEBI platform as of today.

2 Likes