Promoter group, SUREMI Trading has Released pledge of 4,65,000 Shares of NOCIL in this tough liquidity situation in India, which is as a big positive.

7 Likes

2 Likes

@phreakv6 How to verify if the ADD is still active or not ? DGTR website still shows as expiry date of 23 July.

In the context of above news.

Just wanted to seek other forumites’ thoughts regarding the company

In the AR 2019, the following RPT were observed:

- PIL Chemicals , a subsidiary

As on 31.03.2018, shares 83.54 lakhs worth 25.04 cr

As on 31.03.2019, shares 83.54 lakhs worth 25.04 cr

Now when one observes the Financial position of this subsidiary detailed on page 140 of the AR, it is mentioned that its share capital is only 8.35 crores.

Now what is surprising is that, PAT of this company is 1.26 crores only (on an investment of 25 crores) That is like buying the company at a PE of 25 (NOCIL itself trades at a PE of 10)

The reserves and Surplus of this subsidiary is 26.64 cr. Given that the share capital is only 8.35, am assuming that NOCIL has purchased PIL’s shares at a premium, by paying share premium !

- Mafatlal Industries

As on 31.03.2018, shares 19.54 lakhs worth 51.02 cr

As on 31.03.2019, shares 19.54 lakhs worth 21.17 cr

As can be seen there is a huge write down in the value of this investment to the tune of 30 crores , which incidentally equal to almost 1/6 of the NP of the current year, going down the drains.

4 Likes

Mafatlal Industries- Company’s pioneer plant at Navsari is closed now and company is in fragile condition.

3 Likes

Came across this report on NOCIL: https://jcfinadvisory.wordpress.com/2019/12/01/nocil/

Has a couple of new things to say, such as NOCIL will be a big beneficiary of the EV disruption (their opinion, not mine). Also, they are predicting big increase in dividends.

4 Likes

Hi, pl share inputs on how to understand the amalgamation of Suremi Trading approved by board of NOCIL. Suremi Trading has stake in Mafatlal Ind, which is majorly pledged.

As per the latest concall, before doing amalgamation all pledged share will remove.

Means there will not be any pledged at the time of amalgamation.

In additional, Suremin Trading is assets light company, so there will not be much improve in assets.

I didn’t understand it means they pay money and remove pledge ? Or someother way they can remove these pledge at the time amalgamation

This has report on NOCIL though largely nothing new, mostly known things at least for the regular followers of the stock.

5 Likes

Has anyone received dividend? Or due to lockdown people haven’t received direct credit too

Hi

I received my dividend on 24th . Do you have physical shares? As they mentioned in a press release that they will be sending the physical cheques when the lockdown opens up.

My shares are in demat that’s why it seems very strange… thanks for the update though. I am trying to contact their registrar but not able to get through anyone

Received for shares in demat on 24th March.

In their balance sheet, they have declared 250 + crs of land - can anybody explain me more about how to approximately value this entity or if someone has come up with the reproduction cost of assets - how did they value their PP&E. ?

1 Like

This has happened in the past, as was pointed out by DrVijayMalik blogpost. In the past, NOCIL made investments into Mafatlal group companies which were subsequently written down:

- Vibhadeep Investments and Trading Ltd (₹23 cr)

- Mafatlal Finance Company Ltd (₹6.8 cr)

- Mafatlal Services Ltd (₹0.22 cr)

- Mafatlal Engineering Industries Ltd (₹0.17 cr)

- Mafatlal Ltd U.K (₹0.03 cr)

I would urge you to read in detail the blog link I mentioned above.

4 Likes

Yes there is a pattern

- Promoters increased significant stake (3.83%) in period (July 2011 – March 2012) (32.83% to 36.66%) when stock prices were in 15-20 range

- Increased little stake (0.95%) in period (Sept 2014 – Dec 2015) (36.66% to 37.61%) when stock prices were in 30-50 range

- Reduced significant stake (3.01%) in 2018 (36.79% to 33.78%) when stock prices were between 150-230

6 Likes

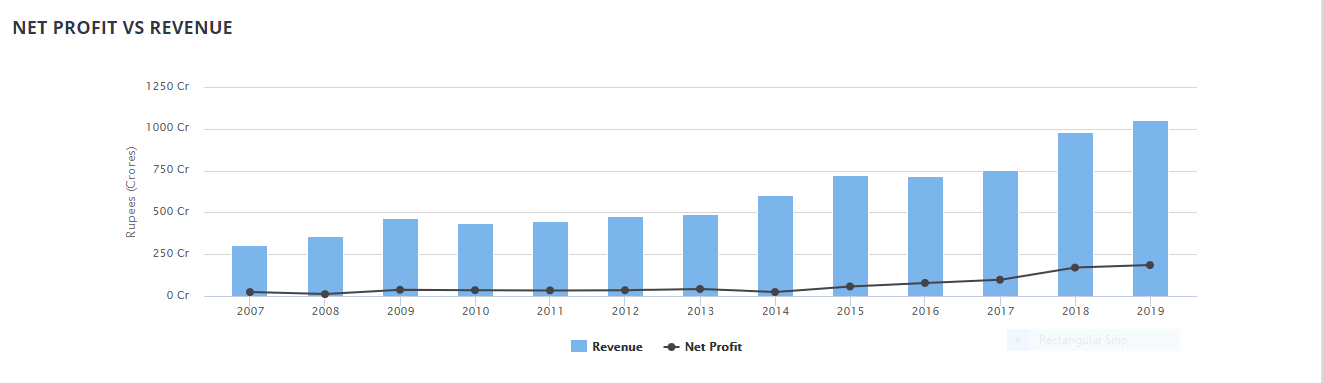

When we see NOCIL from qualitative as well as quantitative point of view with a long term perspective in mind, as a whole it looks as an attractive investment opportunity. The fundamental performance of NOCIL to suffice the argument is its track record of substantial revenue growth that too in sync with the net profit growth in the last 5-6 years :

As we can see from the above chart revenues for NOCIL has a significant uptick in the last five years with net profit also growing proportionately as an indication of improved profitability of the company in the same period. Net Profit Margin for NOCIL during the same period also improved from meager 3.96% to 17.56 percent which indicates healthy improvement as far as its ability to translate a good chunk of revenues into net profit is concerned.

Apart from net profits & revenues, what imparts financial flexibility to NOCIL Limited’s capital structure is the fact that they were able to reduce the burden of debt to minimal levels in the same period, with debt to equity ratio for NOCIL subsiding to zero as visible from the following chart :

The reduced debt burden implies that the company is running its operations purely on-off equity funding. Its recently completed mega CAPEX project for antioxidants and accelerators speaks as a good example for the same.

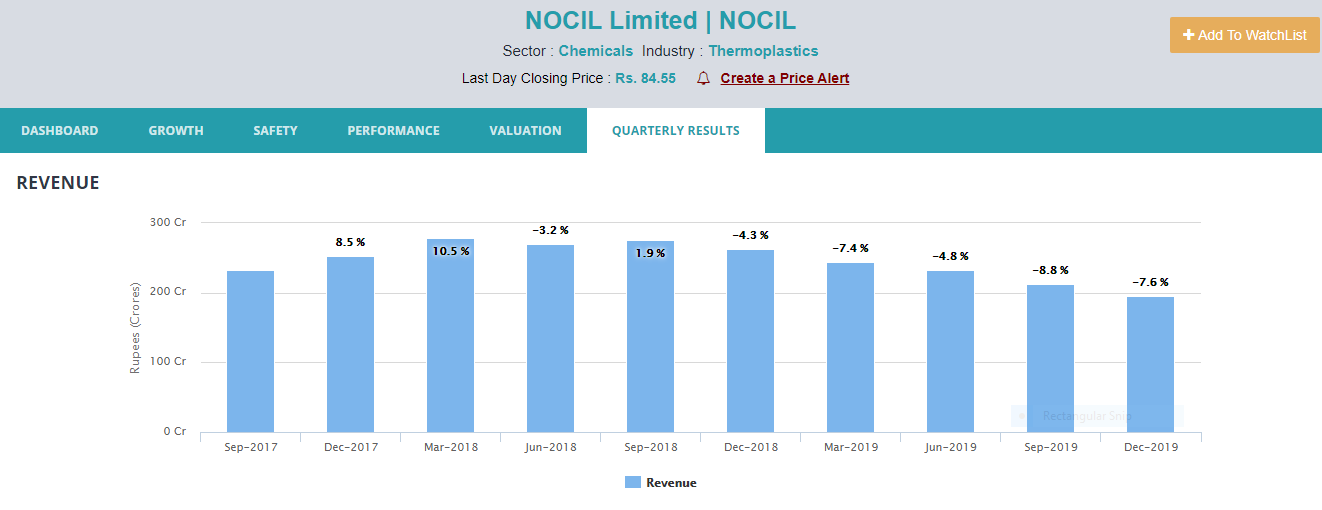

But despite this robust track record, things were not good for NOCIL limited in recent times owing to the significant slowdown in the auto sector. Because NOCIL being a Rubber Chemical player is dependent on the single largest rubber-based industry i.e. the tyre industry, which in turn is directly dependent on the Transportation & Automotive Sector. This slowdown has thus reflected in subdued revenues for the company in the last few quarters :

On the qualitative front, another reason for the downfall was the discontinuation of antidumping duty on rubber chemicals in July last year. To add to that in the last two months, things have become more gloomy owing to the prolonged lockdown arising out of the Covid-19 crisis. The temporary closure of manufacturing operations to go along with the severe demand disruption in the auto sector in the near future present a bleak picture in the near future for NOCIL Limited now. Policy paralysis in import scenarios can also present a cause of concern going forward.

In such scenario key qualitative aspects which should hold the fort for NOCIL (to come out of such desperate times stronger and faster) are: its leading market position, established clientele, sound cost optimization abilities & a better product mix. On a quantitative front, the long term road map for financial flexibility comes from, stronger balance sheet with minimal debt (providing headroom to raise debt should it need to in the future) to sustain and to come out of the timeline of big and prolonged economic crises such as Covid-19.

7 Likes

Co. shows no debt on the balance sheet and yet the credit rating report shows ‘facilities’ of 200cr.

Can someone help me understand this?

The facility breakup indicates that most of it is indirect limits which will not appear on the balance sheet. The Direct Limit is Cash Credit which is short term working capital which is a standby incase of need.

The credit rating agencies will rate the overall facilities sanctioned to the company which may not necessarily be utilized or outstanding.