Here are my notes about this company and textiles mills in general.

After introcuction BT cotton quadrupled our cotton output last decade, govt had to provide incentive for converting all this cotton into yarn else cotton prices would have crashed. This industry provide large scale employment to low skilled workers (unlike IT, Pharma) and has export potential. All are import for the govt to keep the incentives on in one form or the other.

All this has resulted in many entrepreneurs borrowing and setting textiles mills thinking that yarn being a commodity, all they have to do it to make it and take it to the market and it will be easy to sell unlike a consumer product where they have to build distribution networks and brands. Indeed receivables of many of these companies is low indicating they are able to sell their finished goods quickly and get paid.

Trouble is, many entrepreneurs from time to time hae built capacities without any due diligence of demand supply outlook. This has resulted in occasional margin squeeze when factories are commissioned just when RM prices rose.

Cheap debt (due to interest subsidy) has resulted in bringing down the ROCE into single digit level. ROA is also low so under leveraged players cannot earn decent ROE. Leverage is a necessary evil in this industry.

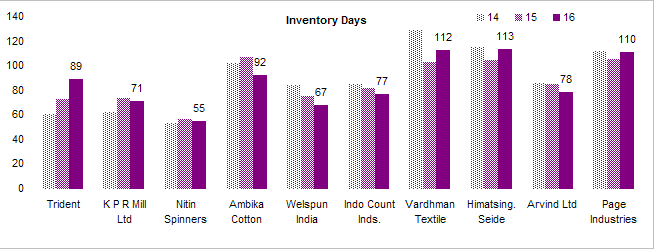

Management of working capital is crucial as once the factory is set up with cheap money, cost of working capital can eat into your profits. Receivables is fine so that leaves inventory management a key indicator. Often, volatility in cotton-yarn spread can cause significant damage to the bottom line if you hold large inventory.

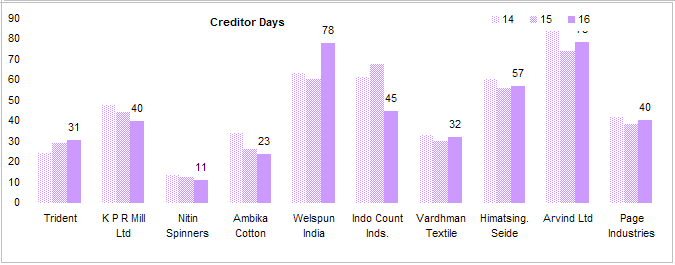

A quick comparison shows Nitin Spinner has lowest inventory days.

However it also has lowest creditor days

Looks like they have to pay suppliers to secure timely delivery of RM.

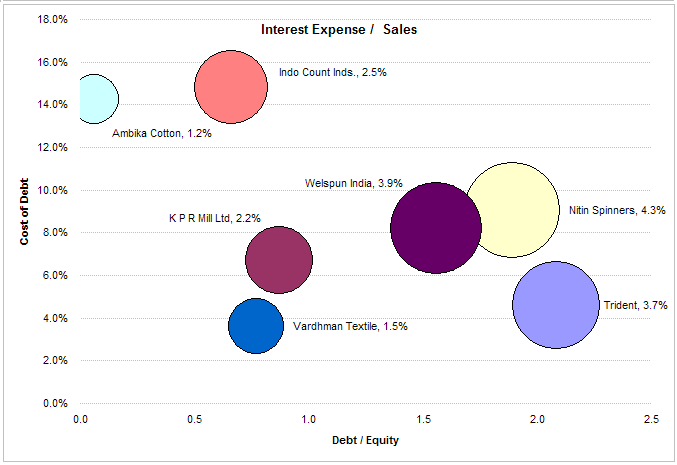

Another key indicator for this industry is debt servicing and optimum level of leverage. A quick comparison shows Nitin has highest debt costs in terms of interest expense as a % of sales.

Bubble size represent Interest Expense to Sales ratio. Nitin has to get its interest costs as low as Trident or KPR.

Disc - No position but researching the whole industry.

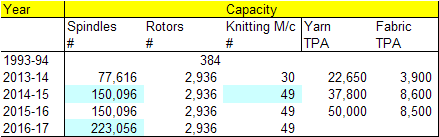

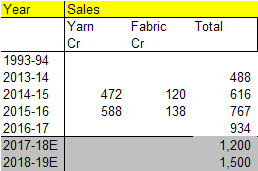

Highlighted cells shows expansions. Most recent expansion in 2016-17 has started commercial production in Feb 2017 and impact will be seen in next 2 FY. The rate at which they have built these capacities and utilized them is impressive. Receivables is low suggesting that they are able to sell everything they made.

Based on the past trend, I have estimated revenues for next 2 years

Assuming a net margin of 6-6.5%% on sales of 1500 Cr, PAT for 2018-19 works out to be 90-100 Cr. At PE of 10, company should sell for 1000 Cr in 2 years compared to 635Cr now giving an upside potential of 60% in two years.

Things can go wrong but these estimates are conservative and company has now built a good track of building capacities under budget and on time and ramping up these capacities as well. Even after nearly tripling their capacities, they still have less than 1% market share so there is plenty of room for growth.

Disc: invested. My views are biased. Not a buy/sell recommendation.

Hi Yogesh, capacity expansion went as per plan and increased revenues shows good execution capabilities… my estimate for sales for fy18 is similar to yours … However, I am not sure if they need to take on more debt to reach sales of 1500 cr… Also, for fy17 the operating margins are lower due to increased rm prices … plus tax has been paid at lower rate (any idea why ?)… in my opinion pat estimation can be tricky for Dy 18 … Disc: invested

Bottom line taking big hit… Last quarter revenue was 248 crore… Pat was 15.1 cr… This quarter 285 crore but bottom line is still 15.7 crore… So revenue grew by 37 crore… But zero impact on bottom line… As mentioned in above discussion law of diminishing returns taking full control?? Views invited…

Discl: invested from 60 levels…

Capex is done at least for now so to reach 1500 Cr they do not need capex and long term debt. They may borrow to fund working capital as the capacity is utilized.

These companies earn cotton-yarn spread so hike in cotton prices can be passed on with a lag. Existing inventory will see mark up or mark down based on movement in yarn prices. Nitin is good at inventory management so I don’t anticipate big losses (or gains).

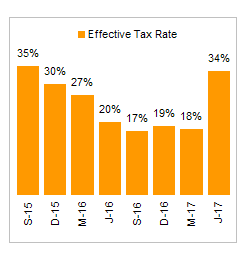

Industry get big incentive from central as well as state governments in the form of low tax rates and interest subvention. I think company has mentioned in last AR that they are getting this benefit for their new unit so that might be the reason interest and tax costs have not moved up. Some of the interest cost may have been capitalized this Q as plant started production in Feb. We will see more impact in Q1.

they have increased their capacity by 50% recently which is on top of nearly doubling the capacity just 3 years ago which could still be ramping up while the new capacity is coming on line. In order to increase the utilization, it is not unusual for companies to lower margins to push sales as they get the operating leverage. that may be the reason EBITDA margins are trending down. I am expecting growth in sales will offset drop in EBITDA margins so PAT cangrow 20-25% over the next 2 years. Based on some reports I have read, cotton output is likely to be normal keeping the prices in check and that should reduce volatility.

The bigger picture here is that industry as a whole is the most competitive in the world and Nitin is one of the competitive players in the industry. They have strong execution skills and past trip to CDR should have taught them a thing or two about debt.

Many established players are moving up the value chain into garments and home textiles so that is also a possibility for Nitin but the spinning itself has a long runway given the small scale of current operations. In this business its all about execution.

Did someone understand what was his explanation for higher taxes? I think they just jumped through that question on taxes in the video which you have posted.

Tax rate was low in FY 2016 and 2017. Now it is back to regular rate.

Source: Capitaline

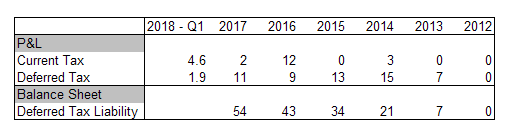

Most of the taxes charged to P&L were deferred until FY 2017. Deferred tax liability has been growing over the years. Now they are paying most of it. Some of the tax benefits must have expired.

Source: Capitaline

This is common for cotton textile companies as they get many tax sops from central and state governments.

Nitin Spinners results for Q2FY18 are ok keeping in mind the GST disruption.

Company press release says that the Net Profit was lower due to higher depreciation because. of expansion project imptemented during

the last year & disruptions in Textile Trade during the curent quarter due to GST. http://www.bseindia.com/xml-data/corpfiling/AttachLive/0ca6a7f8-f0c1-49ac-9bfe-13f33df8622b.pdf

Thank you @Aditya942000

I like this company’s execution plans and track record. P/B or P/E does not look like too high for me.

Dear @Yogesh_s, I know you are tracking this story closely.

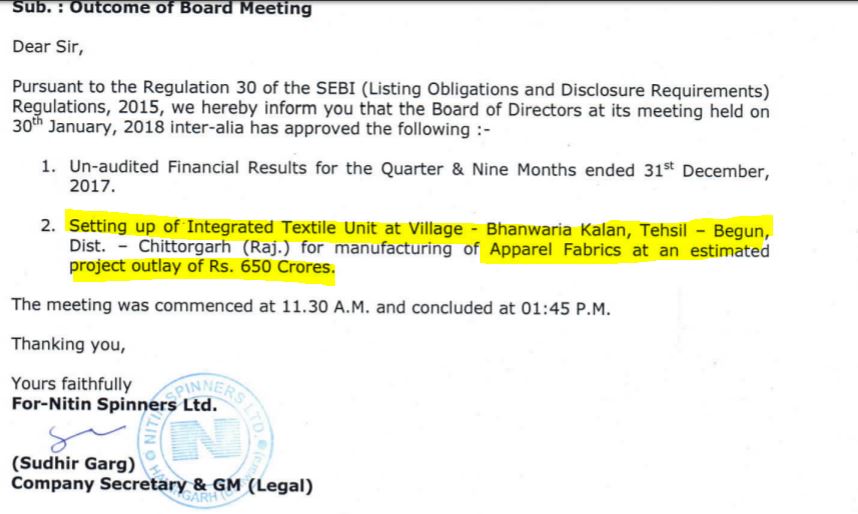

Do you know, if this a new expansion plan or part of the one you already mentioned in your May 2017 post ? In the beginning of this year the price has appreciated kind of 50-60% and remains range bound. Do you consider growth expectations already baked in to share price already ? I am bad at financial analysis, so mostly misses out on margin of safety. That is the background of this question.

The comapny did ~575 crore in 2 quarters and I think another 620-650 crores of revenue possible considering GST impact in the first 2 quarters. Please comment with your views on that as well.

The company did QIP of 108 crores and further 12 crores proposed by preferencial equity to fund the growth. What would the impact of this equity dilusion ?

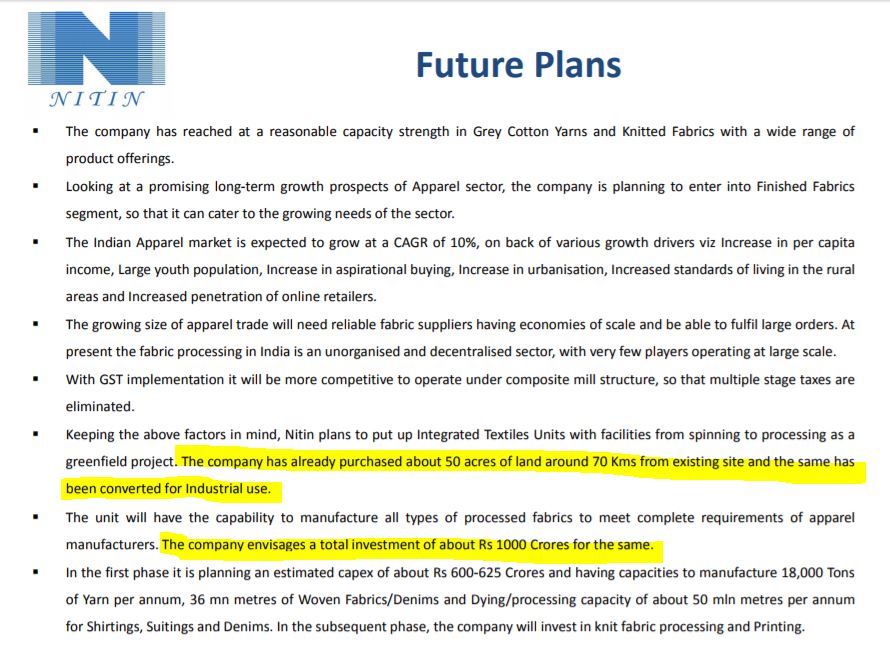

I like this company. Their performance over last 10 years has been impressive. I am little skeptical about the massive capex plans they have. Rs 1000 crore for a company with market valuation of Rs 600 crore.

I am also not sure how much of this capex will be in form of loans. I know they have done QIP but that amount of much lower than capex plan of 650 crore (during first phase). They might need Rs 350 crore for next phase of expansion.

I have read some parts of 2017 AR and Investor Presentation but I couldn’t find the source of funds for capex (maybe I have missed).

And, textile companies are seen with bit of doubt these days, after the amazing move over last few years.

Invested small amount but planning to invest more at the right time.