You must also consider the recent Q1 results. Sales = 196 cr. Op profit - 37.82 cr…so 19.29% operating margins at almost 50% revenue growth compared to same quarter last year.

Neelesh

Margins ebb and flow with capacity utilization - it’s naive to assume that this 19 % will remain if they add another dollop of capacity. Look at 15 year margins of textile companies and you will see that they are never consistent. You are looking at crest margins here and that’s why companies are adding capacity. 2 years down the line, all these will go back to sub 20 ROCE’s

2 Likes

Yes Neelesh, You’re right that for Jun-15 quarter OPM is better YOY but if you check 3 earlier quarters like Mar-15, Dec-14, Sep-14 the OPM is lower YOY with higher sales, and that’s what is reflected in yearly comparison. Long term trend is more reliable than short term trends as far as future is concerned.

Now the question is why OPM is lower with higher sales? It should be higher with higher sales if Operating Efficiency are to be kicked in, Isn’t It? But It isn’t because 1. There isn’t much pull demand so company has to push higher production with lower margins or 2. For every incremental revenue company has to make higher incremental capex. Looking at the current scenario, we may rule out option 1 as there seems to be enough demand. So as Varad has been nicely putting it, unless company’s plants are operating at optimal efficiency generating satisfactory returns on invested capital, we may continue to see lower margins with higher sales.

Also being a commodity nature and with lots of Govt. incentives, competition will catch up in due time creating over supply where things will get scary. If company would have sweated its current assets to achieve optimal efficiency, it would have been better for shareholders because if incremental capex doesn’t bring in incremental returns why incur that in first place?

3 Likes

Another thing we need to be aware of is the mounting depreciation along with the rising interest expense. Though the company can perhaps service their debt in the coming years if demand scenario remains good and other conditions favoring the indian textile industry, however net profits wouldn’t soar by and large since depreciation would also take out a good chunk from quarterly and yearly profits owing to the expansion in the future.

Agreed that the recent Quarters are showing a decline in margins, but the facility has started production only in Feb 2015, (3 months before schedule), sud n’t read too much from 1-2 quarters res.

Overall I feel that Textile story is here to stay because India is in very sweet Spot after may be centuries ( India was a leader in textiles historically before outside rulers came),

now China is self consumed, other countries like Bangladesh/ Pakistan have their own share of problem, India with its stable government+policy support and stable cotton supply could again regain the lost glory. there would be many winners after 4-5 years with right capacity and good management ( intelligent fanatics as Prof Professor Bakshi says).

Disc- Invested

3 Likes

Is the China textile market really shifting to India.

Do we have any export numbers from FIEO or other trade bodies to support this. Lets build up a hypothesis on facts, not assumptions.Lets dig for data to establish the assumptions that Textile Story is here to stay.

There was a valuation gap in the whole textile sector, but that has lessened considerably. Now let us establish more data points to support facts.

Ashwini,

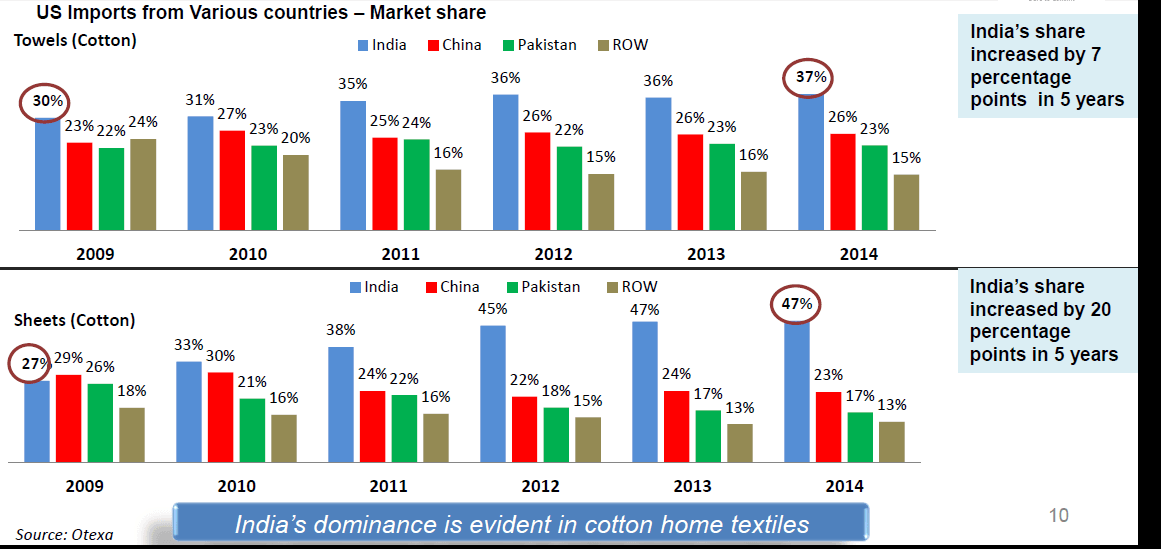

In terms of data - would suggest you to dig up import data of US (from Otexa). Also, please go through presentations/AR/con call of Indo Count, Welspun India, Alok Industries (Alok has some very good presentation stuff though the company is burdened with extremely high debt)

See chart below from one of the presentations:

Each one of these co’s point to one single thing - Indian textile story is here to stay for next 2-3 years atleast. And if macro tailwinds (stable cotton price and India’s low labor cost, etc) continue - the story can last longer and this might just be the beginning. Players who offer some niche and value added products can be in even better spot in years to come.

Invested in Welspun and Indo Count.

9 Likes

Hi @anil…Nice data points. We need this kind of stuff to establish hypothesis. This is the way VP has been built by Donald and Ayush

Hi Varadharajan,

I am not banking on the company to sustain 19% margin for ever. Will they be able to sustain for the next few years or may be a medium term? - I don’t know. With the problem in the competing countries, the shift is definitely happening to India. My sense says that this trend is not temporary or short-lived because their problems are not. I completely agree with you that this is a cyclical business and the margins fluctuate. I don’t consider Nitin Spinners as a top quality business with a solid moat either. And it has a decent debt as well. All said, I still find the prospects promising considering the structural shift from other countries and the stock trading at a little more than 4 times cash flow from operations (not EV/CFO). I will only know a few quarters down the line if my rationale was uncalled for

Btw, just saw the Q1 results of Ambika cotton announced today, Flat sales, YOY decrease in operating margins, net profit and NP margins. In that context, the Q1 results of Nitin Spinners look very promising.

Deleted - as per mod request

3 Likes

Welspun India does own brands in US and UK IIRC, but not sure how successful they are.

Deleted - as per mod request

Saying it from memory… I can google and provide you the link once I reach home, in office network currently!

The hand towels used by the tennis players in Wimbledon are from the brand Christie or Christy which is owned by Welspun India.

Disclaimer: Not invested in Nitin spinner/Welspun India/Ambika Cotton.

1 Like

@Tolaha: You absolutely correct, the they supply towels to Wimbledon. My uncle is GM-operations in Welspun India and he did gifted me similar towel few months back

Do let me know if you guys want any further details from him.

Disclosure: Not invested

@PP1 - Welspun India have their OWN brands (may not be at top end) - but they do have for sure. And they are doing brand building exercise in US as well (Hygrocotton). Go through Dipali Goenka’s interview/con call etc to know more. Also, would request to continue discussion on Welspun India’s thread - here

In the meanwhile, coming back to Nitin, 2nd consecutive LC. stock is slowly drifting below 100. With all the logjam in Parliament, the general drift of cold seemed to have caught on this even by the morning today

Serious headwinds for yarn makers/spinners exposing the commodity nature of the business.

About 500 mills affiliated to South India Spinners Association (SISPA) have decided not to sell or deliver yarns for one week from third week of this month to avoid the traders from creating a situation to source yarn at lower prices.

http://www.business-standard.com/article/pti-stories/mills-to-stop-sales-and-delivery-of-yarns-for-one-week-115081101061_1.html

The real benefeciaries of lower cotton prices seem to be garment manufactures/brand owners.

Deleted - as per mod request

Many yarn spinners are facing the decreased global as well as domestic demand and as mentioned in the article by ET, associations have resorted to spinning holidays to control overproduction of yarn. Nitin spinners has both spinning and weaving facilities ; how is the tumbling demand affect financials and profitability of Nitin? Can anybody dig little more and throw some light?

It has been a horror week for Nitin. What a fall from 107? Every other textile stock recovered except this. Hmmm…plus the usual mmb spice posts of TUFS money not being yet released by the banks !! hmm