Hi @tushar24 , do you know if they have declared the number of NLSL shares that an existing NIIT shareholder receive?

Thanks,

Mahesh

Hi @tushar24 , do you know if they have declared the number of NLSL shares that an existing NIIT shareholder receive?

Thanks,

Mahesh

All holding 1 share of NIIT pre demerger will get 1 share each of both companies post demerger.

Look at the press release. Results of both the companies are there

Hi,

Any one here have any clarity on when we could expect to see NLSL list?

TIA

As per last concall, management said that NLSL will be listed in 30 to 45 days from the record date which is 8 June 2023. So roughly around 8th July to 23rd July 2023.

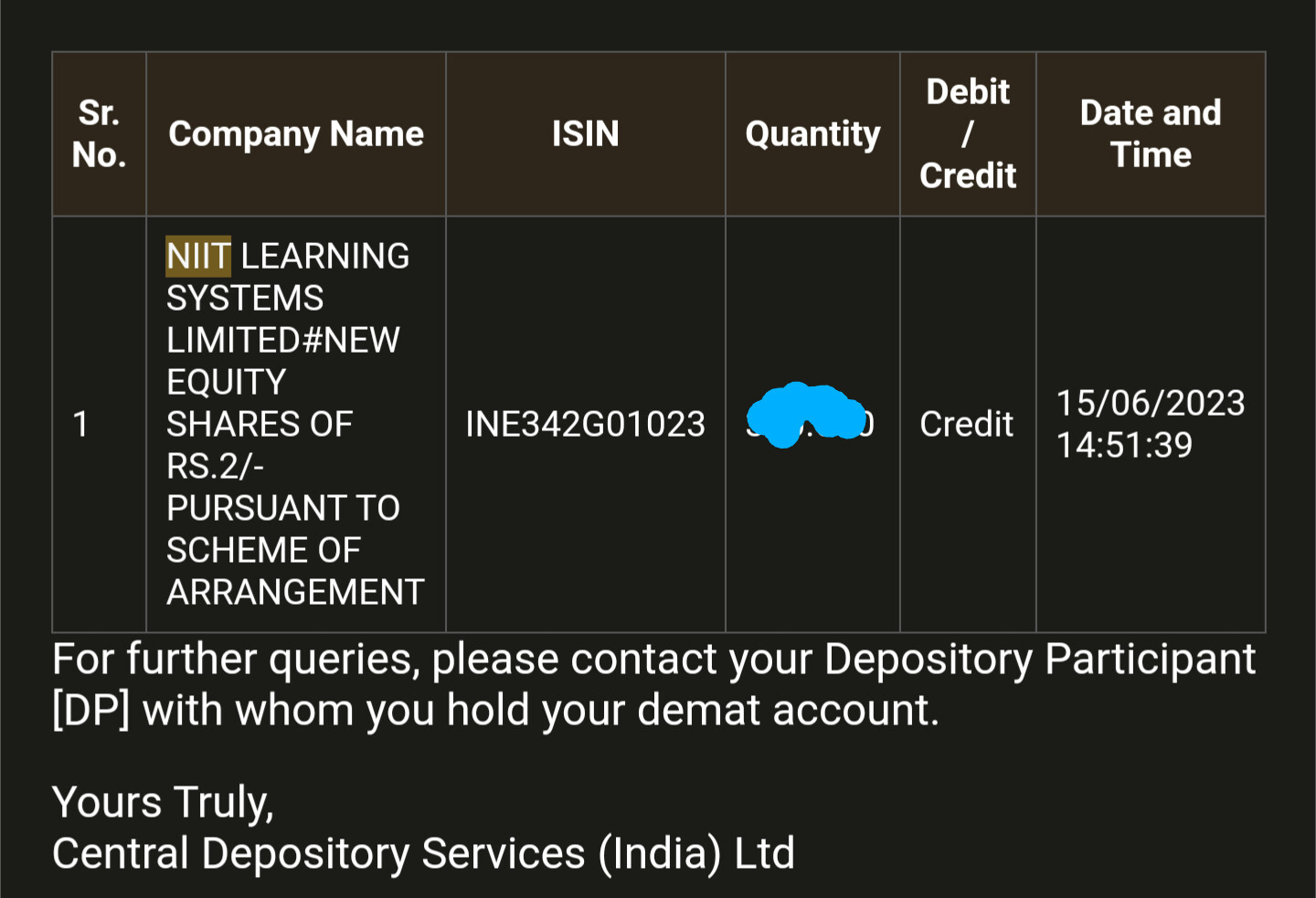

NIIT Learning Systems Limited shares is now credited in the demat but it still not listed.

You can view your shares, do check your demat account or CDSL account.

However listing will be in next month.

Now that the NIIT demerged entity trades at 1100 cr market cap roughly is it undervalued?

Hi all, a quick question,

The record date of 8th June’23 has passed. So, if I wish to sell the existing NIIT position now, I will still be awarded with NLSL shares in coming days.

Is the above understanding correct?

Thanks,

Mahesh

Yes, you can sell your NIIT shares now

Hello All, Have the NIIT MTS (NIIT Learning Systems) shares been credited to your accounts? I can’t see the same in my Zerodha account.

Not yet in icicidirect

not in Zerodha also.It is shown only in Demat account.

Not sure, when it’ll start appearing in Zerodha.

Is it appearing for anyone?

Not yet listed on the exchanges, only shown in the demat holding. Also, AFAIK if they get listed, we get an email either from the company itself or from the broker.

Have a few shares.

CLG business confirmed to be listed on 8th Aug 2023. Exactly 2 months after the demerger record date of 8 June 2023

Disc: Holding

I can see NLSL in Zerodha demat.

NLSL got listed today as NIITMTS at Rs.366/share.

Valuing it at 23x Q4FY23 Annualized EPS of 4.

Results on 10th August.

NIIT CLG Business (NIIT MTS) first ever concall as a separate entity.

Summary

Story in numbers

| Q1FY24 | ||

|---|---|---|

| Revenue Growth (YoY) | 22% | |

| in CC (YoY) | 15% | |

| EBITDA | million INR | 924 |

| EBITDA Growth (YoY) | 21% | |

| EBITDA Margin | 24% | |

| PAT Growth | flat | |

| EPS | INR | 4.1 |

| Client addition | 4 | |

| # of active customers | 83 | |

| Revenue visibility | MUSD | 360 |

| Net cash added during the quarter | million INR | 762 |

| Net cash at the end of quarter | million INR | 5235 |

| Market Cap | Cr | 4750 |

| EV | 4226.5 | |

| Current valuation | EV/EBITDA | 11.4 |

| Price | INR | 350 |

| DSO | Previous range 47-52 | 42 |

| Headcount | 2390 | |

| Renewal rate | 100% |

On the quarter gone by

• Financials for Q1 include the impact of the acquisition of St. Charles Consulting Group, which the company had acquired in November of 2022. Excluding the contribution of St. Charles, the organic revenue was up 1% YoY and was flat QoQ.

• The revenue growth has been impacted in the near-term due to compression in spending by our existing customers due to the prevailing uncertainty in the environment;

• Despite the growth in EBITDA, the PAT has remained the same as last year. The increase is offset by certain non-operational and transitionary expenses included in depreciation, amortization and net other income.

• When announcing the annual results for last year, management expected the first half of the year to be flat and our results are in line with that stated expectation

• Management expected an acceleration in deal velocity and that is also visible in the customer addition in Q1 as well as having a robust pipeline of new customer additions and renewals for Q2.

On Deal wins

• The new deal momentum and pipeline for the first quarter remain strong. The company added four new MTS customers during Q1. This is the second successive quarter in which we’ve added four new customers.

• Out of the four new customers added, one is top-10 pharmaceutical companies and one is top-five retail bank in the US. The other 2 are in BFSI and aviation space

• Revenue contribution from new customers - It takes about four to five months for a new customer to ramp up to a reasonable revenue level, and then it takes about 18 months to get to cruising speed.

• Ramping up of a new customer does require investments. We bring people on and training the people and getting them ready for the work ahead of the revenue starting. There will be some pressure on margin, every time we have a transition, especially for large customers.

On Acquisitions

• Investment in inorganic growth has helped the company break into key industry segments that we wanted to get in.

• With Eagle Professional Services, we’ve been able to get into the life sciences segment and now we have five out of the top 10 pharmaceutical companies as our customers.

• With the acquisition of St. Charles, we have deeper penetration into professional services market segments where we know that the spend on training for employees is almost double the average across industries. St. Charles Consulting was highly distinctive advisory and consulting services across the wider customer set that NLSL has.

• The company announced a strategic investment in InnoEnergy of Euro 3 million and opening new customer segments in the areas of renewable energy and higher education.

• Acquisition strategy - We look for market segments that we are not serving today and how can we add those. And the third is geographies,where we do not have the strength that we need to grow market share.

On FY24 outlook

• It is taking a little longer to rebound the spend on training services as compared to what was expected.

• Outlook is challenged in the near term as the positives of adding new customers at an accelerated pace is being offset by the compression in spending across existing customers. This is reflected in the flat quarter-on-quarter growth that we saw in the previous quarter.

• We expect to start seeing sequential growth returns in H2, driven by continuing new customer additions ramp up and stabilization as spending rebounds in our existing customers.

• Given the delayed recovery in consumptions, we now expect mid to high-teens on year-on-year growth for FY24 in constant currency. This is a revision from our earlier forecast of 20% growth for the year

• From Q2 perspective, we expect flat Q2 with respect to revenue and Q2 margin is likely to be in the 22% range. Customer sentiment is not showing signs of recovery yet but no deterioriation either.

• On 20% margin guidance (current is 24%) - We didn’t say there is going to be 400 basis points compression in the margin. We had indicated that the expectation should be greater than 20% margin and we are staying with that expectation, we don’t expect it to go down to 20%.

• One more thing to keep in mind, typically when we have a renewal during any quarter, there is a step jump. There are a number of renewals due in Q2, but there were none which happen during Q1.

Sharing notes from NLSL Q2 FY24 concall. I wonder if we should have a separate thread for NLSL