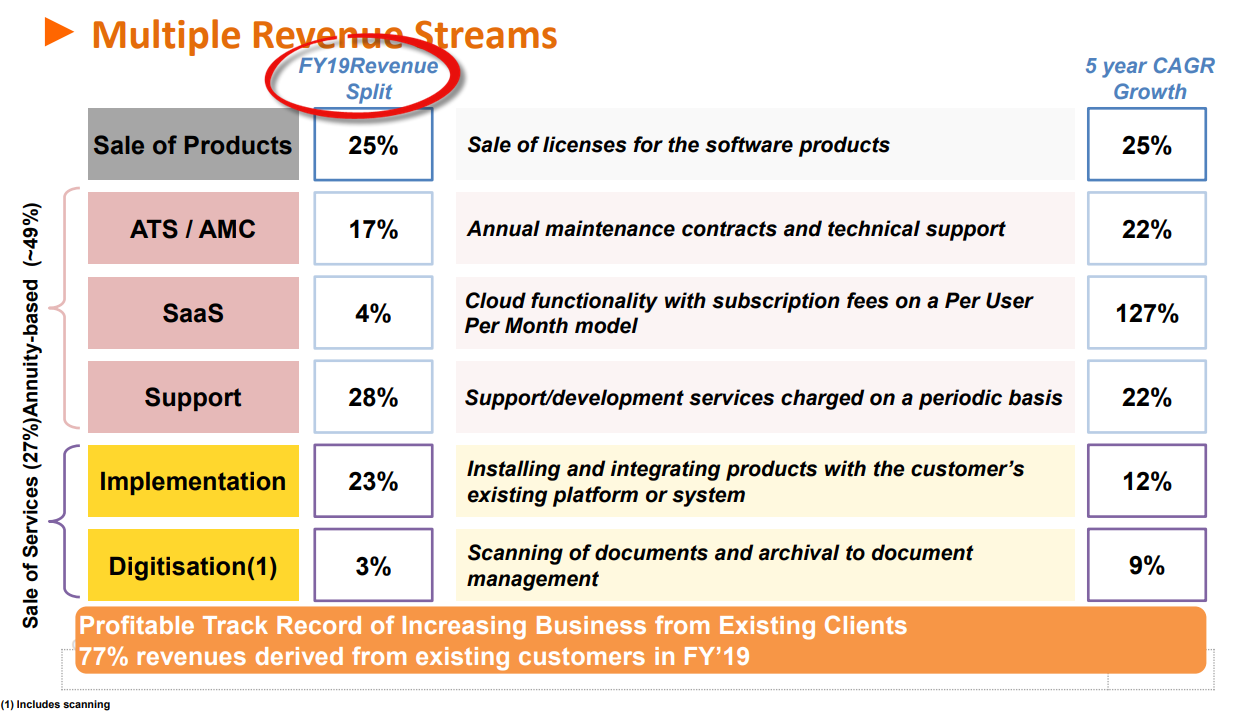

To be honest, I have still not been able to figure out to my satisfaction why the cos revenues are so seasonal. The mgt has tried to explain but I just don’t get the terms they use because I am not from an IT background. They do have a well diversified revenue stream and all the patents. I spoke to a couple of people about patents and it seems that cos can apply and get generalised patents purely based on concepts without actually having to demonstrate it in practice which struck me as a bit weird. Due to my inability to understand fully how they generate business and the ease with which cos can get patents I have decided to walk with caution esp after the cos stock price hit my most flexible stop loss and triggered an exit for me.

There patents are nothing to write home about. There Software is a platform therefore has wider use cases…but thrre are better softwares now with much better interface…they have not been able to conceptualize any new software beyond DMS and BPM…DMS is quite a legacy product…to scale further will take a lot of effort…which i think is doubtful given promoter age and all…

I can talk a little bit about the revenues IT product companies earn in emerging markets as I have a work background in this space. Generally local System integrator partners in the emerging markets generate leads. The partners invest in trainings their personal depending on how popular these products are in the local market. Earlier bigger companies used to charge the smaller partners for training but now most companies big or small provide free training to be competitive. Generally the partners have a % cut in license (10 - 55%) fees depending on market and how much of sales effort is done by the partner. If the software is not established in the market then the partners negotiate a larger fee because the cost of sales for a new software is significantly larger than selling an established software. Software buyers usually expect local support and generally prefer dealing with the principals (software makers) than local system integrators. Ofcourse the software sellers cannot establish offices in all the countries, hence they train the local system integrators. implementation and support revenues are also plum incremental revenue that local partners eye for and the percentage share varies largely between local installation or SaaS / Cloud model. For cloud software the local support is not that critical as the servers are central and not local hence partners have less clout. Hope this information helps understand then business better.

My two cents with regards to seasonality in revenues: -

New logo wins seem to be consistent across the quarters with probably an equal win across H1 and H2 based on available investor presentations for fy18 and fy19. However, understanding the kind of wins within these numbers across the quarters and the deal origination market (emerging vs developed) is essential to bifurcate annuity revenues (cloud/ats/support) from one time revenue (product implementation/digitisation) and timely payments (characteristic of developed world) from bunched up payments (trait of emerging world) respectively. While these details are not available, a quick crude level check on top line sales shows: -

H1 fy19 vs H1 fy18 = 23% upside

H2 fy19 vs H2 fy18 = 19.7% upside and

H1 fy20 vs H1 fy19 = 11.33% upside (low figure could be attributed to macro issues as faced by other IT cos)

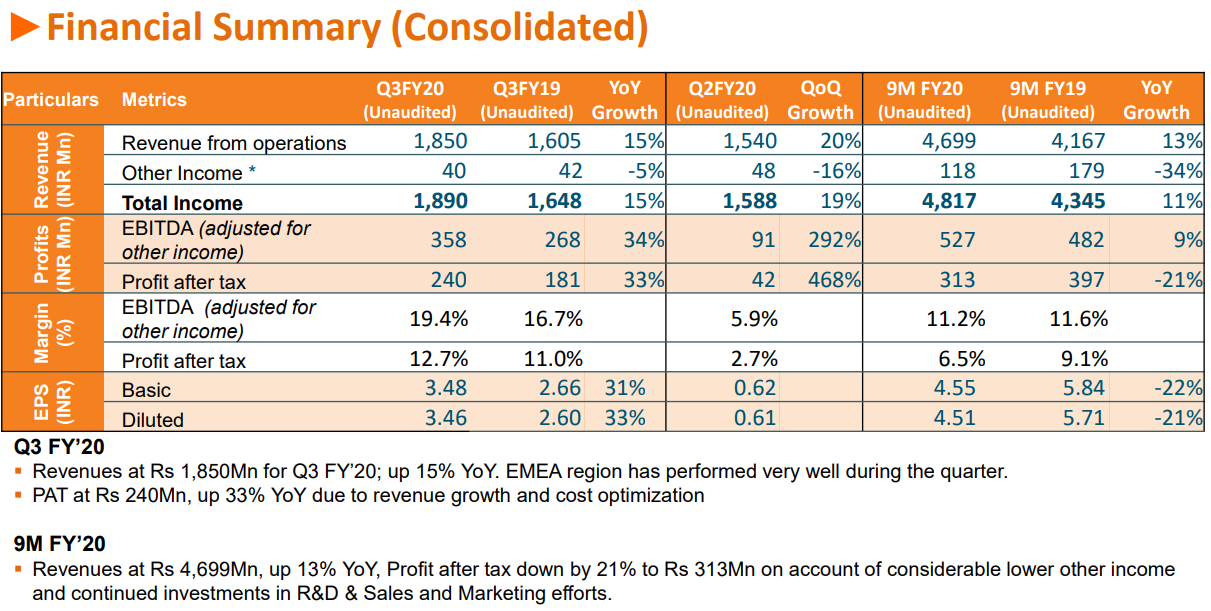

While q3 fy20 is up 15% yoy

The above indicates a growing top line sales which I believe is very important for this business considering the generic nature of their offerings.

As regards the patents, acquiring patents on concepts is not so uncommon in the IT domain but are these filed in India or US? I would certainly give more weightage to patents filed and awarded in US vs India.

Inquisitive to know the other software available with better interfaces. Can you share the names or the competitors offering them? Also why is dms legacy? What’s the technology stack used?

Any reasons as to why costs are attributed to India with regards to global sales? PBT figures across geographic segments seem skewed due to this.

Infact revenue shown across Indian standalone and subsidiary is same. Also, this question was asked in conference call to which mgmt did could not provide a clear answer claiming that the Indian subsidiary is solely for business from India with the global nos. Getting consolidated under Indian parent.

at the end of the day its an IT company that makes products, using employees who are based out of India. From their last AR if you look, they have close to 2700 employees- "With an employee base of 2,700+ across the developmental centres in Noida, Gurugram, New Delhi, Mumbai and Chennai, Newgen continues to attract the best talent in the industry ". Also do keep in mind that they might hire a few senior people for the top positions who might be based out of India, but the bulk of the employees are based out of India.

I did not have a chance to attend the conf call, will wait for the recording on RB…

Pursued this point with the company and they did verbally agree that there are costs booked in India standalone towards projects originated from overseas market with the usual reasons and calling the current negative PBT figures to be one-off. There appears to be some cost balancing/apportioning done across entities in a manner proportionate to revenues/work force.

Regardless of where the costs are booked, one would expect the consolidated figures at all points of time to be giving a true picture to which the management’s response was agreeing though not very re-assuring. However, they have agreed to provide more visibility into sales in terms of logo wins in the different areas tentatively from qtr2 FY21, that might help to track figures at a more granular level.

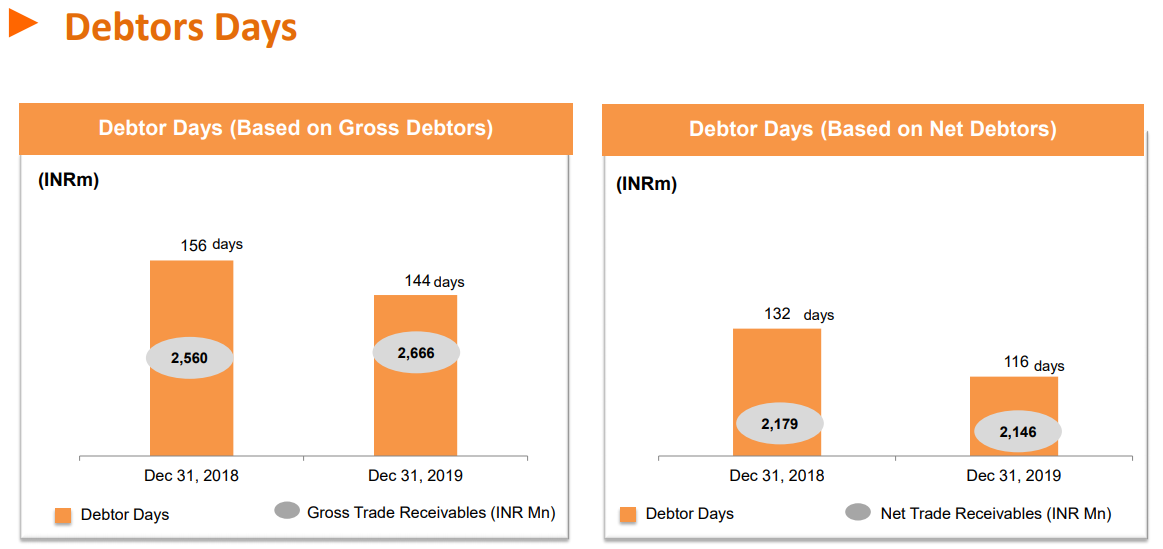

Is their receivable aging due to any specific account (or a particular invoice)? I recall that another product company Tejas Networks had BSNL as their main account and even after 1yr of product delivery the amount never got collected. Management should come out in open with respect to their customer wise Aging as generally software business should not have more than 75 days aging.

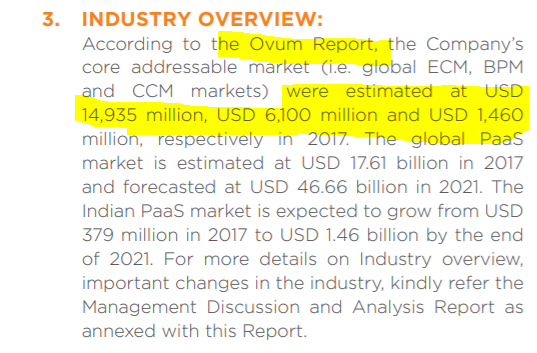

As per the annual report, they claim that company’s addressable market size is $22k m which is huge. I tried google for Ovum reports but couldn’t find any such reports. Does anyone has any insights on what is Ovum reports ?

Yes, thats the interview. The News anchor referred to a Jefferies report quoting that margins are not sustainable. I was wondering if anyone has access to that report