It’s good to see your portfolio evolving as compared to the original at the start of the thread.

Many of your stocks were either cyclic or PSUs which have greater risks associated with them as compared to other business. Playing Cycles for a new investor is not that easy.

Generally it is said that if you want to play cycles , buy at high PE (When everyone is avoiding & company making losses or less profitable) and sell at Low PE (When everyone gets attracted towards it and earnings are positive). It requires a lot of patience as well as understanding of the cycles and patterns which in my view comes from experience and thus is not everyone’s cup of tea.

Coming to the current portfolio , i would like you to reconsider your investment in Dilip Buildcon. The balance sheet is heavily stretched to make up for Profit and loss statements. The business is extremely capital intensive. Even if you have good conviction , 14% allocation looks too high. I hope you understand the exact nature of business and why they are growing currently (Showing high sales and profits). For me , it is like a house of cards which may fall any day just as the likes of JP Assosiate , Lanco , Unitech etc. Also the corporate governance issues have been there in past. Here is a news from 2012.

Coal India is a cyclic and PSU bet. Personally i find it tough to understand but there are several contrarian views emerging in market about good prospects for the business going forward. Though , it is better to avoid if one does not understand the business.

Allocating such high% in Yes Bank may be risky as new things may come up in market after Ravneet Gill taking over as CEO. It may be better to wait on sidelines or reduce allocation till clarity emerges and paying up a little higher after clarity will be more prudent than taking such risks in dark. Personally i prefer HDFC Bank as it is managed very well but waiting for it to correct to some good extent.

SBI looks more a like of turnaround bet in Public banking space after clearing the NPAs and stricter IBC Codes. But again , there are risks like waiving off the loans just recently happened for Pulwama attack victims. Morally it is very good but as a business , it is a loss. Though one thing i have noticed that the PSBs have become more aggressive in terms of recovering the amounts and are given free hands to attach properties of defaulters to recover the money. Those who understands the space , SBI and some few PSBs looks good as contrarian bets.

I do not have any idea on HDFC life (currently understanding the industry) , Persistent , Bharat Electronics.

ITC , Hero , Maruti , Godrej Consumer looks good. Don’t know what made you exit in M&M which is one of my long term bet.

Disc: You can avoid my views as i am also a new investor with less than 1.5 year of experience. Some thoughts may sound immature and need not to be taken seriously.

Thanks for providing your feedback. Please see my comments below.

Dilip buildcon - I agree that my allocation is high(14%) even though my conviction is high. Also I agree about high CAPEX need in the business. I am planning to reduce my allocation to 7-9%. I got high allocation since I started buying from high(700) and keep on averaging. I see non-bjp govt as risk for the stock. But stock is at 7-8 PE due to that reason.

Coal India - I also dont understand the business and was thinking if I should keep 4% allocation in the stock or completely exit from it.

Yes Bank - High allocation - Agree on this too. I realized this last week and reduced my allocation to 10% as it has become around 13-14%. I will further reduce it to 5-7% and will get into HDFC Bank as I get opportunity in term of price.

M&M - There are many reasons why i dont like M&M anymore. One is high debt and another one is due to absence of good car in PV. I don’t see any car from Mahindra which can beat Maruti. Mahindra came up with XUV500 and Scorpio in past. But there are many other SUV came into market like Hyundai Creta and Maruti Vitara Breeza. So personally I dont think Mahindra can compete with Maruti. Hence I am not planning to have it in my portfolio. We can still bet on tractor division though.

About Dilip Buildcon, I didn’t started buying due to low PE. I was watching this for some time and started buying when stock price started falling due to stock added in ASM. But it was removed later on from the list. I liked the business due to its order book, ability to execute the business before time etc. There is a risk of high debt. So I will monitor it for some time and will decide if I want to reduce my stake or not. But irrespective of that, I will not have have more than 7-9% of any stock in my portfolio even if I have high conviction in that stock(some FMCG stock might be exception in future).

Regarding M&M, probably I was not looking at the numbers standalone. I think I should look at it again carefully. XUV300 will definately make a difference. I looked at the SUV online when it launched and it will will tough competition to Maruti Breeza.

Hi @kumars1672 since you are around my level of learning, let me give you another lesson which will save you a few years of pain. Do not buy PSUs. My experience shows that they do not make money. Just compare the mentality of a PSU employee to a private sector employee and you will get the answer why! PSUs in my mind is an excuse of an enterprise which are run to appease the politicians and influential (at least in India).

I totally agree with you about psu. I have small allocation of coal India and sbi in my portfolio which I am debating in my mind wheather to keep them or sell.

About bharat electronic, I think with make in India initiative and India-pak issues, govt will spend more money on defense in order to modernize the arms. Hence I have that stock. I might reduce my allocation to 5-7% though.

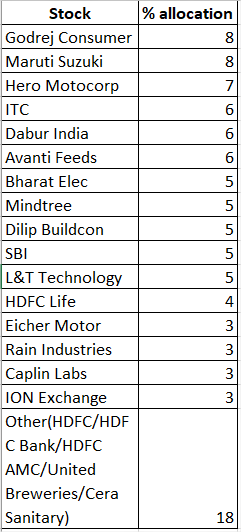

I am sharing my updated portfolio after a long time and would request experts to provide feedback/opinion. I have bought few stocks from my last post. It includes increasing allocation to existing stocks as well as adding new stocks. I have around 23 stocks in my portfolio. But 70% allocation is in 6-7 stocks. Some of the stocks like multibase, mirza international, beekay steel were bought as experiments and got stuck in them. Also Yes Bank might be NPA stock. But I want to give it some more time. Some other stocks like Exide, M&M, Coal India are there in my portfolio for some time. I didn’t increase the allocation. But didn’t get rid of them either. I have highlighted stocks in orange and yellow which I will to get rid.

Some of the stocks which are in my watchlist are ION Exchange(Govt focus on providing drinking water to all), Mannapuram Finance, HDFC Bank, HDFC, L&T Finance,Cera Sanitary, Eicher Motors.

Overall goal is to keep around 15 companies(20 at max).

Dont allocate any money(even a small %) if information is not present or you are convinced. I bought multibase even though there was no information on the company - no concall, no presentation, very limited information about the products. Buy stock only if you have done some research. You can keep doing more research after you do initial study and buy some stocks.

Allocate enough money to good quality stock e.g. HDFC Life came to 350 and I bought only 1% of it.

Never miss the opportunity to buy quality stocks. e.g. I saw price of HDFC,HDFC Bank going down to 1600 and 1900 respectively, but I was waiting for prices to go down further. I should have started buying these type of stocks. Another example is HDFC AMC which came down to around 1300-1400 level. But I didn’t buy it

Book losses - I should have book loss in Multibase instead of averaging down.

Keep 60-70 of the stocks which are large cap(I will say large cap like ITC,Godrej Consumer). 30% could be mid cap and small cap. Never experiment more than 5-10% of your portfolio.

I see in your rationale for Godrej consumer and itc that they are not great companies. Can you pls elaborate which companies you consider great in FMCG and why you chose these two and not them for your portfolio. Also what characteristics make a company great according to you and what is missing out of those in these two. Thanks

I would say company like Nestle are great companies as they have products like Maggi. Reason why I dont think companies like Godrej consumer are great companies is that they are mainly into hair color, insecticide etc. I dont think they are dominant in soaps or air freshner category. ITC is into lot of products from school notebooks to aata to soaps and many more. But I have experience interacting with their management(not higher management) for some purpose. Their culture seems like govt company. So my personal opinion is that ITC will not be aggressive like other companies.

My opinion about great company is where customer get used to a brand due to any reason. e.g. I dont see any substitute for Maggi just for an example. Top ramen and other noodle also came. But failed to get market share.

Reason why I have Godrej and ITC in my portfolio is that I wanted FMCG companies with low PE even though they are not great. Both of them are good companies where I will not lose my capital even though growth might be slow. Godrej’s promoters are good and I think company will grow if they keep on innovating new products. Nestle has high PE. So I was not able to buy it.

Very true . Apart from whatever you mentioned above , what one often tends to forget is that Nestle has 97 percent market share in Infant cereals and 67 percent in baby food . In this segment it’s a monopoly and plus more importantly its more sticky than other FMCG categories as ppl would generally never think of taking chance or risk on their baby food .

Hi ,

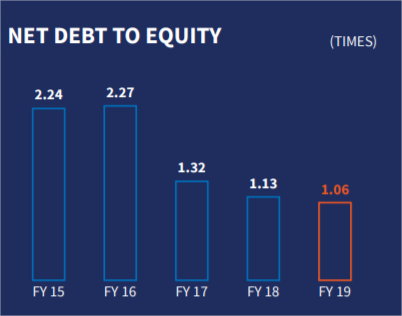

I hope you are aware of very high Debt to Equity of Dilip Buildcon , very poor Cash flows , Capital Intensive nature of the Business , Pledging etc. Earlier there were news of Tax raids too in 2010. Such high allocation must be backed by good study and not merely on expectation of Government spending.

Better to book losses where you think it was a mistake and invest that money into convincing ideas. Merely waiting for stock to bounce and then sell does not look great choice. I believe that good companies will rise higher when market sentiments will change.

Also regarding Ion Exchange , it has been very popular these days marketed as Govt focus on drinking water. Reminds me of similar times when Sterlite Tech was marketed as 5G expansion (It was at 400 levels) and Graphites story were there as structural shift (HEG was 4000). It has run up a lot in past 1 year and now being marketed on forums. Invest only after you understand the business well.

Hi @bharat19 . Yes I am aware of high D/E of Dilip Buildcon and capital intensive nature of business. Basically I am betting on below things -

Order book - company has around 21000 crores of order book and I am expecting company to get more orders.

Execution capability - company has completed more than 90% project before time and received early completion bonus

Debt level reducing - Debt level has been reduced to around 1. I was hearing management interview and Rohan Suryavanshi mentioned their goal is to reduce it to below 1. This is considering company has 10000+ pieces of equipment on its own.

In term of risk, i know still they are at high debt level. Ideally it should be less than .5 But considering company is available at low PE, i expect risk is already covered in the price.

Also recently govt sent letter to NHAI about changing their model. This might be another risk on how company will get more orders.

Ion Exchange - This will be very small holding in my portfolio(might be less than 2%). I see company has good financials with debt less than .5 Also considering there is shortage of drinking water in India and govt is focusing on it, i think company will benefit from it.

that the above two companies are dealing or depend directly on government and its related projects - Payments/Policy making is the real issue. Probably thats the reason in construction and its related industries, we only have one successful company in our country, L&T, even after 70 years of Independence.

As janata changes opinion every five years both at state and centre level, also the ministers changes every now and then obviously policies changes very frequently.

Recently Andhra government changed and they are trying to change all including the already awarded contracts, half executed ones also- everything is a mess now.

Most important thing at the portfolio level is one cannot have these kind of companies major holdings - i learned this the hard way by paying my tution fees.

If some thing goes wrong, we have to sell immediately no matter what, just sell and think later, not the other way around.

I feel, you have too many cyclical companies & sectors that are in downturn.

Avanti Feeds, Autos (Maruti,M&M,Hero,Metals (JSPL,Rain,Beekay).

Cyclical better to buy when the ground reality of sector changes. Autos, Metals are having serious issues. If you are someone who can ride few quarters of downturn and wait for good times in few years time,then do it.

Other thing is, there are few companies in too much debt - JSPL, Rain, Mirza

ITC price has come down but it has given no value unlocking for shareholders for some time now. HDFC life is good to continue.

I have not seen even Rs 10 repaid back on debt…not one year…last 10 yrs they have no paid back even one rupee…how can we assume in next 10 yrs will they pay this at half of the debt…

I agree metal are having serious issues. I was holding JSPL for last one year in hope that steel price will increase. But it keep on going down. I will wait for 1-2 more quarters before I start reducing my allocation in JSPL.

Avanti Feeds - i believe management is good and company will do good in future.

Auto - Currently auto industry is down. But I dont think it will be down for a long time. Maruti and Hero will grow once auto industry recover

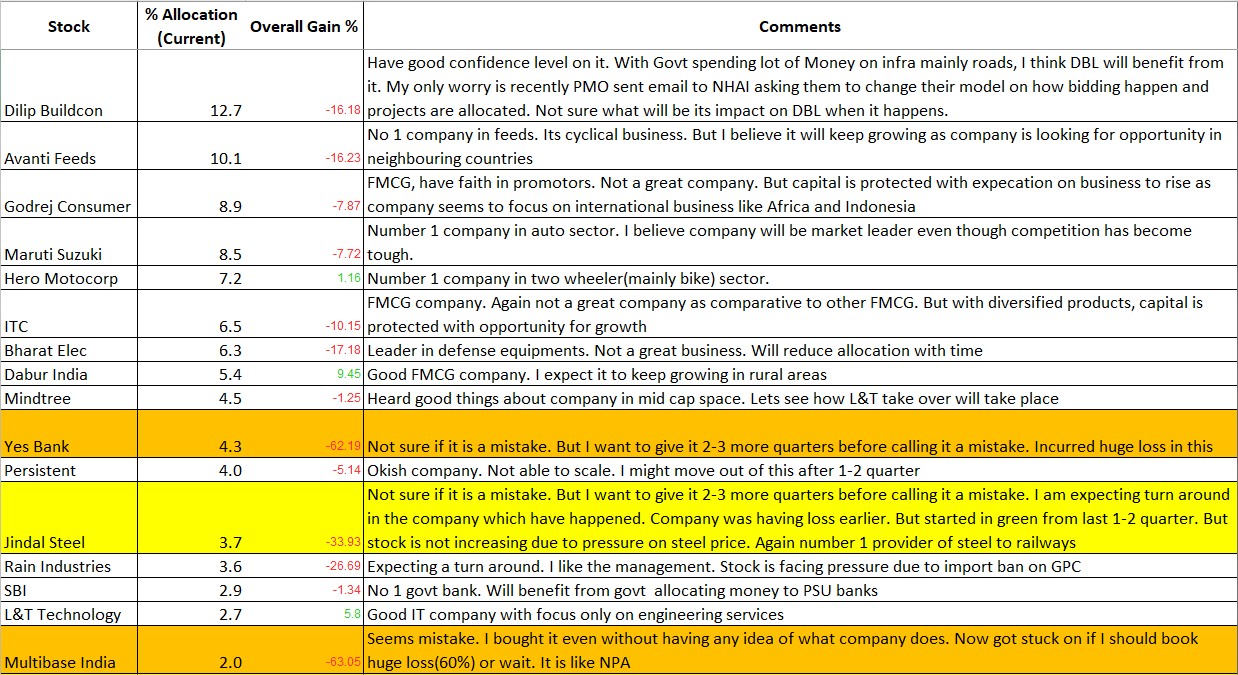

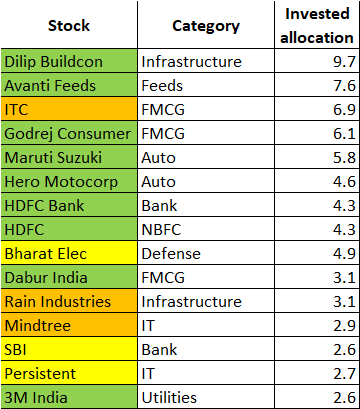

Thanks to all for providing feedback on the portfolio. My goal is to make portfolio like below in next few quarters. It includes reducing allocation in few stocks, increasing in others and buying some new(mentioned under others).

I entered into stocks like HDFC, HDFC Bank, 3M India, Eicher Motor, Ion Exchange in last few days. Now my 70% portfolio is allocated in below stocks. I sold exide industry. I am looking for opportunity to exit from stocks like Mirza international, yes bank, JSPL, SBI, Persistent system, Coal India, Multibase India. Yes Bank and Multibase India are two holdings where I am having huge loss(60%). Overall portofolio is 6% down mainly due to these two stocks.

Lesson learnt is that never catch falling knife(Yes Bank). Also never invest until you have enough details on a business, I invested in Multibase India even though there are no details about their client, business, no concall. I just looked at their financials and invested.

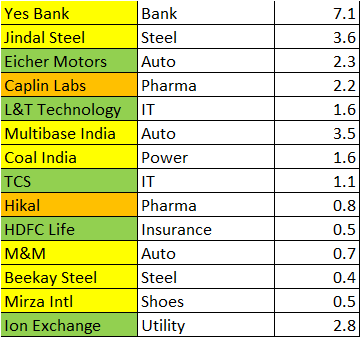

Stock Category Invested allocation

Rest is

Color scheme -

Green - Will keep it

Orange - Opportunistic - may or may not keep them

Yellow - will exit from them

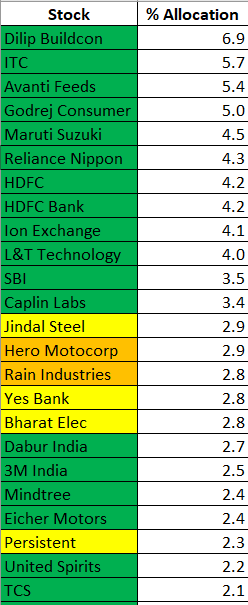

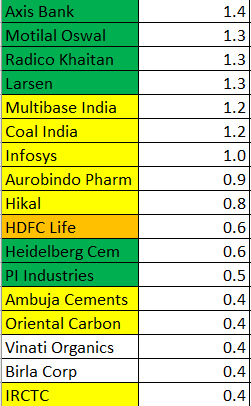

Hi All, I am updating my current portfolio. I has become MF now with 42 stocks and I need to reduce it to 25 in next 6 months. Please feel free to comment on it. First 12 stocks have 55% of portfolio allocation.

Stock Category Invested allocation

Stock Category Invested allocation