http://content.icicidirect.com/mailimages/IDirect_NCLInds_MgmtNote.pdf

thanks for these information. As ICIci report mention they are planning to get this loan of Rs.325 crs And these 18% P.A is not way too high??? another question is as per last qtr results their Interest cost was about Rs. 7 crs and annually it is about 30crs so for 325crs at 18% their intrest cost will go to more than 55crs annually. Is my understanding right? correct me if i am wrong.

Thanks

These loans are generally structured and includes PIK portion (linked to EBITDA perfromance and stock price performance). Most of the companies account only for cash portion of interest.

This are copies from ARFy16. so they will incur atleast 55crs interest cost once whole NCD will be withdrawn.

Prashant

do anyone has done market review of demand and price realization of cement after demonetization in these regions?

Thanks

Prashant

The NCDs with Piramals and also the last quarter result are a bummer. I just feel this is a trader’s paradise with swings from 80s-140s. Investors be a little cautious as the promoter’s are not genuine in their intent. They once say post a result that we can hit this much EBITDA and PAT. They said post 15Cr Q1 last year, we will be 70Cr FY and they managed 42Cr or so. K Ravi does a lot of magic when he comes on TV and just promises a lot of things but the balance sheet and P&L statement do not reflect those.

The rising interest costs and also the proposed capacity addition under current environment where capacity utilization in the South is 60% also raises a lot of eyebrows. I have burnt my hands in this counter by investing heavily and not buying other players like KCP, Kakatiya, Kesoram, Ramco etc,

5 Likes

Q3 bang bang results from NCL, Topline up 50%, Bottom Lime up 3 fold. Stock up 16% today. 1 Rupee interim dividend declared

Oct 16 buy coverage from way2wealth

Disc: Invested

1 Like

Prices may increase further in the near-term: NCL Ind

Healthy improvement in demand in South India: NGVGS Prasad

Expects sales and EBIDTA CAGR to grow at 15% and 19% respectively.

http://economictimes.indiatimes.com/et-now/corporate/healthy-improvement-in-demand-in-south-india-ngvgs-prasad/videoshow/57771209.cms

1 Like

Any updates or any useful information on rally off ncl industries. Cements prices looking going up. Any analysis on trends of prices and consumption of south based cement companies

CREDAI alleged that cement manufacturers have artificially raised prices by more than 60% in Telangana and Andhra Pradesh thus pushing the prices anywhere from `240-380 per bag in the last one week.

Can someone advise on the impact of this to companies like NCL

2 Likes

Promoter bought from market on 26th July and Sagar Cement another small cement player in AP posted excellent result.

Q1 FY18 Results : Gross Sales at 297.5 Cr vs 256.3 Cr, Net Profit at 16.3 cr vs 9.1 Cr , YOY.

http://www.bseindia.com/xml-data/corpfiling/AttachLive/D9DE8A0C_8325_4E90_991C_EF89C6D08118_172942.pdf

2 Likes

1 Like

NCL AR 2017 Colour Executive Version final.pdf (1.7 MB)

Management says:- Growth seems good for short to medium term. Rising price of fuel is major concern.

Anybody have any idea of what is the price of Pet coke currently. Sharp rally in Goa Carbon Ltd give some hint that the prices are increasing

1 Like

Can someone help me with cemebt outlook and forecast to help me understand whether ncl is a good buy at this price. Kindly share ur insights ok ncl industries

[Uploading...]()

Ncl industries to set up a unit to manfacture readymade doors

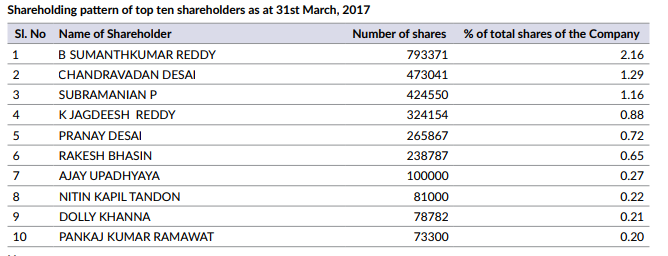

Interesting Top 10 Shareholders !!

3 Likes

Any comments on the results.

- New particle board plant opened with effect fro 2nd dec

- Margin pressure is seen in cement division (Any particular reason ?)

Couldnt find any details on the commencement of additional cement capacity. Looks like WC pressure is back.

1 Like