Hey @PraveenKG. I don’t actually. I used Muthoot capital services as training to understand the nbfc sector with skin in the game. The more I studied it the more I realised how inherently risky nbfcs are and I sold off a while back when covid 2.0 began and I felt my money was way too exposed. I have no regrets though since studying it made me understand the sector and what the small players are doing to survive etc and this led me to understand and invest in probably the lowest leveraged lender in the market ie ugro capital. Currently ugro capital is the only nbfc I own and considering I’m not willing to pay high book multiples for lenders it probably will be the only one I own(bajaj and muthoot finance are the best bets in this sector but considering the inherent risk in lending I don’t like paying up) . Its Lower levered, higher crar and cash, better tech, huge scope for growth, low npas… . Basically its everything Muthoot is trying to be in a few years. I suspect that this second wave will put even more pressure on Muthoot and its not cheap enough yet even now to be a survival play considering its trading above book value.

Why has the group been silent?

The Muthoot capital has seen quite a value destruction and despite all the tailwinds, and good promoters they are not able to make it a solid franchisee.

I was going through the annual report and I have two questions:

- Why has the business in FY21-22 reduced to 397 crore from 504 crores when the Auto sector has started bouncing back.

- While their interest expense is down to 150 crore yet there expenses have increased from 186 crore to 476 crore

- What is this other expense which has increased by 102%. Is it a one-time thing or what’s happening over here?

Let’s discuss this stock and see if it’s a value trap or a great opportunity to be tapped.

The stock has been making new highs on a daily basis.

Moreover, CRISIL has upgraded it to A+ from the A status.

What’s the view of other shareholders on this stock?

I think, with credit cycle going up, it should do well, but most of theor revenue is dependent on two wheeler sale. That will be the key metric to monitor.

I wanted to share some recent developments that have given me renewed hope for a particular stock. Despite previous setbacks, the management’s efforts seem to be paying off, and I’m optimistic about its future prospects. Here are the highlights:

![]() CRISIL Ratings has upgraded the ratings on Series A1 PTCs and Series A2 PTCs issued by ‘Plutus 09 2022’ to ‘CRISIL AA+ (SO)’ and ‘CRISIL AA- (SO)’ respectively, from their previous ratings of ‘CRISIL AA (SO)’ and ‘CRISIL A+ (SO)’.

CRISIL Ratings has upgraded the ratings on Series A1 PTCs and Series A2 PTCs issued by ‘Plutus 09 2022’ to ‘CRISIL AA+ (SO)’ and ‘CRISIL AA- (SO)’ respectively, from their previous ratings of ‘CRISIL AA (SO)’ and ‘CRISIL A+ (SO)’.

![]() In FY23, the company’s PAT (Profit After Tax) increased to 77.92 crores, a significant improvement from the loss of 161.82 crores in FY22.

In FY23, the company’s PAT (Profit After Tax) increased to 77.92 crores, a significant improvement from the loss of 161.82 crores in FY22.

![]() The EPS (Earnings Per Share) in FY23 stands at 47.84, a remarkable turnaround from a negative EPS of 104.53 in FY22.

The EPS (Earnings Per Share) in FY23 stands at 47.84, a remarkable turnaround from a negative EPS of 104.53 in FY22.

![]() The yield has maintained an average of 19% in FY23, up from 16.5% in FY22.

The yield has maintained an average of 19% in FY23, up from 16.5% in FY22.

Considering these positive developments, I am growing increasingly hopeful about the future potential of this stock. However, I would love to hear your opinion and insights of others on this matter.

Disclaimer: Please note that I have personally invested in this stock over the past 3-4 years.

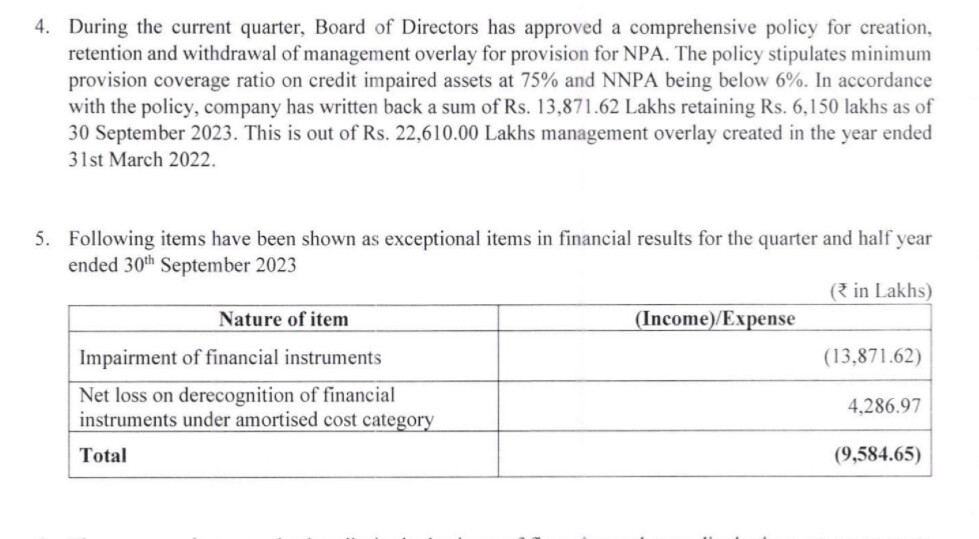

Company has been doing well, however this quarter was muted. However thr interesting thing is that the company has written back provisions worth 100 crores (market cap- 650cr) that were done in 2022 making this quarter EPS jump to 50. Shareprice currently is at 400 levels.

Waiting for their concall on 30th to ask them about it.

Disc: Invested from lower levels