MPS Ltd AR 2021

-

MPS finds itself at an inflection point, poised to usher in a new era of organic growth. This growth will be fueled by our core strategy to Transform, Innovate, Maximize, and Elevate.

-

This five-year BUILD phase now needs to actively transition into a platform-led THRIVE phase, introducing a new era of organic growth for the business.

-

The acquisition of HighWire in the past year and the revival of the Content Solutions business give us the confidence that we are on the right track.

-

Content Solution

-

Content solutions reported revenues (FX-adjusted) of INR 229.22 crores compared to INR 205.29 Crores (FX-adjusted) in the previous year, a growth of 11.6 percent.

-

The positive change can be attributed to the successful implementation of a robust Business Continuity Program, stabilization of customers’ businesses after the initial setbacks of the lockdown, step-up in the volume of work from several of our core customers, and onboarding of new customers.

-

The primary driver of the growth in the Content Solutions business is the expansion of our Educational Publishing Practice, which includes MPS North America and the associated Content Production and Digital businesses driven from Indian operations

-

In the past year, we have seen much more educational products being developed and that too from a broad set of customers. Additionally, we saw certain key accounts in our Journals Content Management grow organically, resulting from exceptional delivery and quality even during the pandemic.

-

Ultimately, Content Solutions is the highestmargin business for us and continues to be the largest. Any positive movement in this business segment does proportionally impact the consolidated business.

-

Sustainable growth in the Content Solutions business is a great sign of the core strengthening ahead of Vision 2023.

-

-

Platform

-

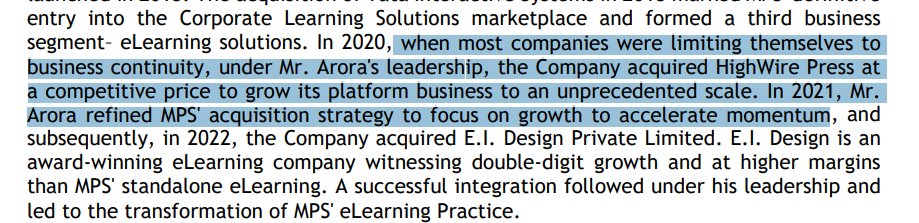

Our agenda to grow the Platforms business segment in proportion to the consolidated business significantly advanced in FY21. From 16 percent in FY20, the platform business accounted for 33 percent of the revenue in FY21. The acquisition of HighWire Press on July 1, 2020, was the predominant driver of this initiative, while the organic growth in PaaS offerings such as THINK further solidified our growth strategy

-

HighWire In terms of financials, we have generated a PBT of INR 18 crores in the first nine months. We must put into context that the original purchase price for this business was INR 53 crores net of the working capital adjustments.

-

Customers for this business are growing, and our plans to increase the revenue per customer and number of customers are underway.

-

The acquisition of US Business of HighWire was carried out through the Company’s US branch and newly incorporated wholly owned subsidiary namely HighWire North America LLC, Delaware USA, by way of forward merger at a purchase price consideration of USD 6,100,000 (US Dollars six million and one hundred thousand only) .

-

The HighWire business at Northern Ireland and United Kingdom was carried out by way of purchase of 100% shares of HighWire Press Limited based at Northern Ireland (“NI Entity”) through its wholly owned subsidiary company MPS North America LLC, USA (“MPS NA LLC”), at a purchase consideration of USD 1,000,000 (US Dollars One Million only). NI Entity owns 100% shareholding of Semantico Limited (“UK Entity”). Pursuant to this acquisition, NI Entity has become subsidiary of MPS NA LLC and UK Entity has become the step down subsidiary of MPS NA LLC.

-

Highwire total purchase consideration was Rs. 59.51 cr against net assets of Rs. 34.02 cr and Goodwill of Rs. 25.48 cr.

-

-

E-Learning

-

Our eLearning solutions segment reported (FXadjusted) a decline of 24.5% percent in revenue from INR 75.52 crores in the previous year to INR 56.96 crores (FX-adjusted) in FY21.

-

eLearning Solutions was our sole business segment that was economically impacted by the COVID-19 pandemic

-

The year started with turbulent headwinds owing to the slowdown in the Order Book with customers. As the Order Book picked up during the financial year, the execution of projects still went slow. We are gradually building momentum as the Order Book has now reached previous levels, and the rate of execution is now also nearing normalcy as customers are opening up .

-

Our strategic direction, step-up in activities to revamp operations, and the market sentiment help us maintain a positive outlook toward this segment.

-

-

Financial

-

forex-gain-adjusted revenues of INR 424.22 crores in FY21. Revenue growth of 26.89 percent and that too in the year of a pandemic has been a tremendous feat indeed.

-

EBITDA significantly improved from INR 82.80 crores in FY20 to INR 109.56 crores in FY21, growth of 32.31 percent. While our EBITDA margins improved slightly, much work is still to be done to drive better profitability.

-

EPS was suppressed by as much as INR 6.5 due to the one-time tax events in Q3 and Q4. The former was related to a long-overdue matter from the Macmillan days, which was settled via the Vivad se Vishwas Scheme to avoid protracted litigation and the attendant uncertainty on the issues covered in those years. The latter relates to the impact of the Finance Act, 2021, which does not allow deduction of depreciation while computing taxable business profits, and affects past transactions.

-

Content Solutions, Platforms, and eLearning contributed 54 percent, 33 percent, and 13 percent of the revenue, respectively

-

while North America continues to be our largest market, our customer concentration continues to improve, with the top 5, top 10, and top 15 segments accounting for 38 percent, 50 percent, and 59 percent of the revenue , respectively. This trend of progress can drive more stability toward the longer-term growth aspirations of the business.

-

MPS continued to remain debt-free through the year, with surplus funds of INR 180 crores on its balance sheet at the close of the year under review.

-

During the financial year 2020-21, your Company has bought back 5,66,666 (Five Lakhs Sixty Six Thousand Six Hundred and Sixty Six) fully paid equity shares of face value of INR 10 each at a price of INR 600 (Rupees Six Hundred only) for an amount not exceeding INR 34,00,00,000 (Rupees Thirty Four Crores only) under tender offer route, representing 3.04% of the paid up share capital of the Company. The Buyback was completed on 7th October, 2020. Pursuant to the completion of buyback, paid up share capital of the company stands reduced from INR 18.62 crores to INR 18.05 crores.

-

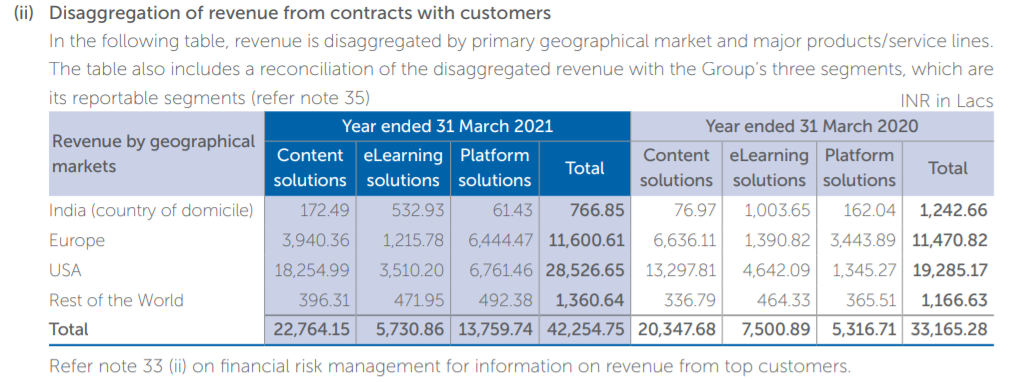

Sales Bifurcation region wise (Rs. in Lac)India (country of domicile) 766.85 (1,242.66) Europe 11,600.61 (11,470.82)USA 28,526.65 (19,285.17)Rest of the World 1,360.64 (1,166.63)Total 42,254.75 (33,165.28)

-

-

MPS employs over 2,571 people across 15 centers in seven countries. We have a significant presence in the USA, Europe, and India. Content Solutions is our largest segment by strength, with a total headcount of 1970. Dehradun is our largest center in India, employing over 1,000 associates .

-

The Company had 2269 permanent employees on its rolls as on March 31, 2021.

-

We have made seven acquisitions in seven years. These acquisitions brought synergies in business operations and solutions development, capabilities to amplify our skillset, and expanded our customer base and revenue streams to diversify and strengthen our business as a whole.