It is really surprising to see it near 52 week lows since its peers are doing well. In fact Edelweiss is close to 52 week highs. It is ironic since they have been heavily promoting their brand on TV and the stock keeps tanking. I think it is mostly to do with the screw up in their housing subsidiary and potential turbulence in capital market biz due to political tubulence. Let’s see how do they perform and the plans to come out of it. We need to keep in mind that when they let one new subsidiary slip into difficult times, the managment discount starts creeping in.

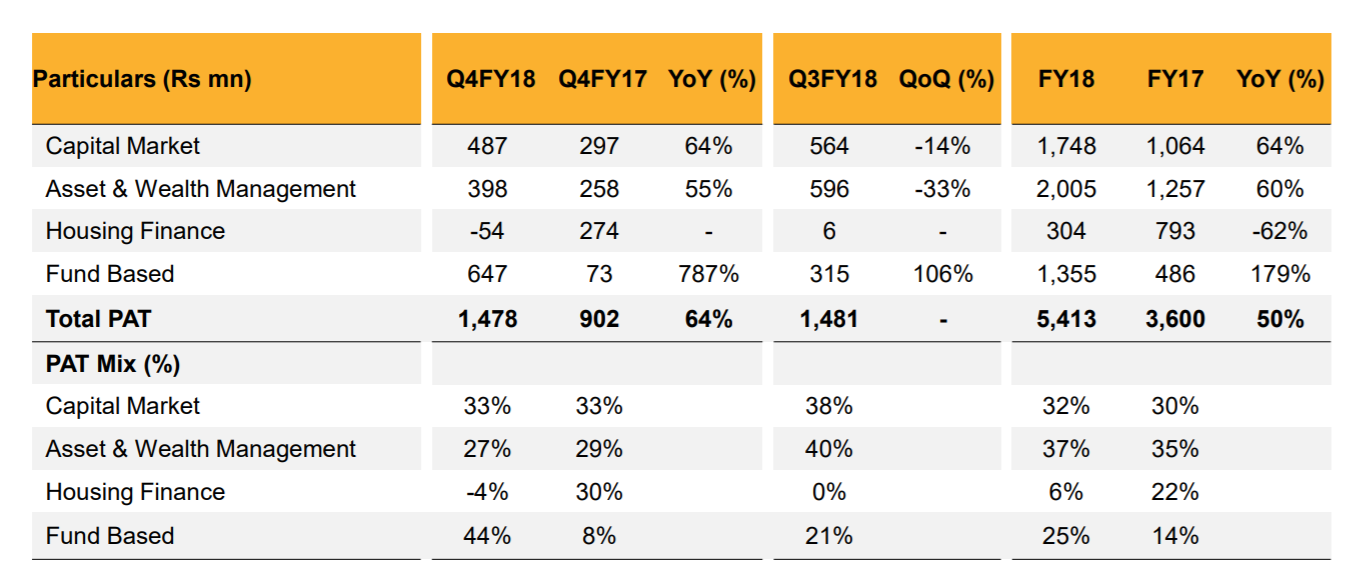

Q4FY18 PAT of Rs 1.48 billion,

+64°/o and FY18 PAT of Rs 5.41 billion, +50% YoY.

Aspire Home Finance’s loan book grew by +17% YoY. Margins stood at 4.1% in FY18 versus 3.6% in FY17. Net NPA is down on QoQ basis, from 3.6% to 3.3%.

all round good performance despite tepid sequential nos.

Aspire - despite writing off 72cr in FY18 and provision of 56cr, PCR is only 35% . Good amount of pain is still left here. They expect NPLs to rise further in H1 FY19 before stabilising in H2. Let’s see how Mr. market reacts to this. With the benefit of hindsight they should have started with wholsale debt biz first rather than retail housing loans.

Heard from sources that people are redeeming motilal oswal mutual funds due to their bad performance due to high valuation exposure and also manpasand saga. Can anyone through some light on this if they have heard about it?

The stock is crashing as if there is no end. One of the key mistakes of this year for me is to not to sell at the right time. While performance seems good despite Aspire, looks market is reading and knowing more than what is there in books.

At 24 times earnings it is not as if the market is negative on Motilal as a company. It’s still very expensive from a valuation point of view.

Only thing is the momentum trade in this stock is over. In fact one can argue it will now reverse.

But it still is a great business.

Don’t think we should read too much into the price correcting nominally.

How much PE value should one assign to such company considering this year market will not be like last year , after a good correction and seems bull market is also over and it can consolidate till elections , interest rates may rise also which can reduce current year earnings also. I dont track this stock but wants to understand from valuation point of view. what could be the fair PE , if we consider earnings will decrease in current year. Is 15-18 PE is fine ?

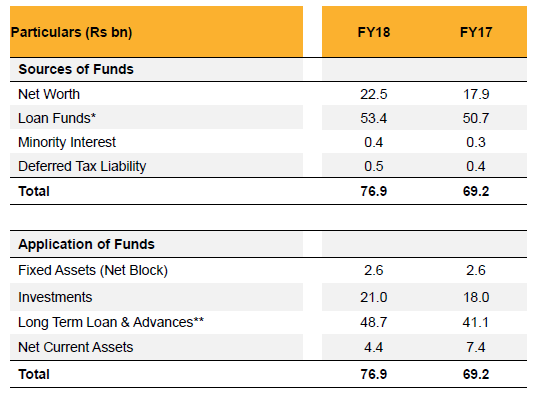

Anyone has any idea what is this Ex-Aspire borrowing of 1400 Cr used for? As far as I know, most of the company’s businesses are fee based so will not require heavy borrowing. fund based businesses are all funded by equity and not borrowing and even Loan Against Shares portfolio is only 180 Cr. curious know why is the company borrowing so much. Will appreciate any information.

Good catch! need to confirm with the mgmt. Apart from funding LAS, it could be used for balance sheet management i.e. cash management required for running diverse businesses. This means they are deploying own fund in Pvt equity etc while taking leverage to manage liquidity.

The fall is really sharp and I think it is also due to lack of volumes. FIIs are in exit mode probably taking view that domestic flows will slow down going ahead. This stock is a perfect leveraged play on Indian financialisation with broking/asset management/wealth mgmt. I don’t think bull market is getting over so soon.

Disc: It has hit my target of 800 and have taken small position.

Drastic reduction in PE for Motilal Oswal Financial. From 79+ in 2014 and 57+ 6 months back, it has come to a PE of 21.3. This is the lowest PE for the stock in the last 4 years since the foray and emphasis on new lines of business such as PE / HFC/ MF etc.,.

At the present price fluctuating around Rs.800 (even below 800),its PE ratio is lower than many other famous peers like Edelweiss,Birla Capital,Bajaj Finserv,IIFL etc.The management team including Mr. Raamdeo Agrarwal is quite capable.Hence,it can be considered for accumulation at dips in my humble opinion.

If this is what is actually happening then all those things that fired up earnings growth over last 2 years could backfire over next 2. I guess market is already pricing that scenario. the drastic fall appears as if market has gone from pricing this stock as a great growth story to a cyclical that is about to enter a down cycle.

Many of MOFSL’s earnings streams are market linked and if (or when) markets correct, those streams will dry up as well while costs remain more or less the same. Operating leverage will kick in this time in the wrong direction. I will wait to see the impact of a market correction on MOFSL’s financial condition before trying to put a fair value on it. This is the first bear market since MOFSL took leverage so we don’t exactly have something to compare with.

the only issue is we have cyclically high eanings and Mr. Market thinks that probably it might fall going ahead.

@Yogesh_s I think they have enough unrealized profits to take care of any weakness for the next two years of potential trading weakness. They might have decline in cash trading but asset management/wealth will still be growing handsomely as they are snatching market share. Fund based profit booking will be handsome due to change in accounting treatment.

The fall is entirely due to FII selling and mostly due to Morgan Stanley which is a relentless seller while many long only FIIs and DIIs are increasing stake here. No doubt Manpasand is a big screw up from Motilal oswal but I would still be ok. As an investor we need to back fund houses that take calculated risks rather than keep 100 stocks in the portfolio. I think they have private equity midset while managing MF. One can doubt their capabilities but not intentions. I also expect them to make amends quickly.

You are right on most counts. As far as my analysis and information goes, the management is not worried on any aspect except Aspire which they are trying to fix. It may still take a couple of quarters to do so, as per them. So it is a good long term at these prices, imho.

Slightly different topic: Accounting of unrealised gains in MOSL under new accounting standard i.e. Indian Accounting Standard (Ind AS) 19.

MOSL has significant unrealised gains from their investments in their own MF products. They have been selling parts of their MF products over the last few years and the capital gain has been a part of PAT (approx 100-150 crs). However under the new accounting standard the unrealised gains/losses are to be shown as profit or loss which may affect the reported profits. Below is an example:

Lets assume MOSL invests 100 cr in their own MF products on Jan 1 2017 say at a NAV of Rs 20.

Lets assume the NAV was Rs 30 on March 31, 2018 and NAV was Rs 25 on June 30, 2018.

Using the above NAVs the Market value of investment on March 31, 2018 was 150 cr and Market value of the investment was 125 cr on June 30, 2018.

Under previous accounting standard MOSL had an unrealised gain of 50 cr on March 31, 2018 and 25 cr on June 30, 2018 and they have been booking a part of it which shows in PAT.

However under the new accounting standard the unrealised gains/losses will form a part of PAT and for the Quarter ending June 30, 2018 they had an unrealised loss of 25 crs (150 cr to 125 cr). Since they have to report it as a part of PAT they now have to show it as a loss whereas they were showing a part of it as profit earlier.

Above is just my thought process but I am not a Charted Accountant and can be completely wrong. May be our accountant value pickers can chime in.

On the business side nothing much has changed. Though the inflows in their flagship focus 35 scheme has approximately halved over past few months. Maybe a market wide trend.

For most of the companies Q4 (March Year end) results are always later than other quarters so that date cannot be used estimate the probable result date for other quarters. Last year Q1 (June) results were released on July 27th, so this year there is a definite delay. Not sure if we should be worried but this is certainly an anomaly.