After a small correction, it seems attractive to me considering how each vertical, MF, HF, Brokering is going to expand in the next 5 years. In case there is another correction of 10%, it may look good even for short term.

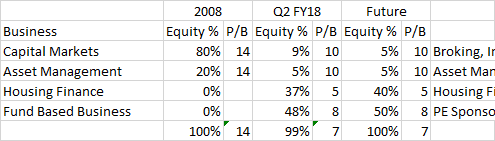

I did some follow-up work on this - based on my rough calculations, the stock was trading at highest P/B of 14+ during peak of bull market in 2008. At that time, MOSFL was primarily a broking and asset management business. Few changes to these business since then:

- Broking side has now added investment banking which, in my opinion, should have similar types of P/B

- Asset Management has expanded into Wealth Management and PE businesses, all of which should have similar P/B

However, new streams of business i.e. Housing Finance (37%) and PE sponsor commitments (48% along with LAS) form a major chunk of total book size.

I have tried to work out a consolidated P/B for the business based on individual estimations for each business as below (I have tried to estimate an ideal P/B for this business - will look to apply margin of safety over and above):

2008 Q2 FY18 Future

2008 Q2 FY18 Future

Business Equity % P/B Equity % P/B Equity % P/B

Capital Markets 80% 14 9% 10 5% 10 Broking, Investment Banking

Asset Management 20% 14 5% 10 5% 10 Asset Management, PE, Wealth Management

Housing Finance 0% 37% 5 40% 5 Housing Finance

Fund Based Business 0% 48% 8 50% 8 PE Sponsor Commitments

100% 14 99% 7 100% 7

2008 equity % is my own assumption. The P/B values for individual businesses are my best guess estimates (would really help if someone can provide better estimate based on their experience)!

Thanks. The purpose of putting up this analysis was to get inputs on the efficacy and data.

Could you direct me to data points on funds deployed in individual category. My estimate on Fund business P/B was based on assuming a higher proportion of PE sponsor commitments (could not get breakup of allocation within Fund Business).

Irrespective, it appears that MOSFL is a good high beta proxy on fund flows into the market and thus highly cyclical with such fund flows. The Management appears to realise this and therefore, is getting into unrelated businesses (with high ROE) to diversify in order to show better performance even when equity markets are “slow”.

Looks good now after having corrected by around 20% from top.

Further fall. Where is it going to stabilize?

No matter how much tax is increased on cigarettes or tobacco products, consumption never reduces much … Similarly no matter how much tax is increased on lottery people won’t stop buying them…

Similarly, people who are in stock market, especially traders dealing in derivatives, intraday traders and short term traders, can never reduce or stop trading. This class of people contribute a good portion of income for all broking companies.

Brokerage income earned from delivery based trade is comparatively less…

I feel there will be hardly any major decline in income of broking companies, infact there income should increase only as earlier difference between short term and long term was 15% and now it is just 5%. I feel people will now book profits at regular intervals. Small investors who would want to save tax will try to take advantage of 1 lakh LTCG benefit by booking some profits every year, and reenter again, increasing trading activity and hence increased brokers revenues.

I think once the dust settles, people will realize this and will slowly start buying I to these brokerage companies which have already corrected by 20% from top.

Disc : entered Motilal oswal recently around 1300 and adding on declines.

An interesting article on restructuring of MOFSL where it is consoldating it’s business vertical to make its main vertical stronger.

Article - Motilal Oswal Financial Services makes core areas stronger

Stock has been dropping consistently on a day to day basis. Is this just because of the general mood in the markets or has there been any development?

Stock price has come down because market is unhappy with the performance of Aspire Home Finance. Ramdeo Agarwal still dreams that Aspire will reach the heights of PNB Housing or Gruh Finance, something which can be achieved only with super stars like Sanjaya Gupta or Choksi at the top. In the latest concall, Ramdeo Agarwal informed the analysts to assume 0% return on equity for Aspire. Stock is still adjusting to that calculation. With Ex Dewan housing employees, Aspire can atleast hope to become a DHFL. Or they could buy an insurance company and use the float like Buffett since Ramdeo Agarwal is the master of the stock market. Considering the growth of the company, corrections like this could be a buying opportunity as the analysts will value this company at 50 pe again if Aspire turns around. Considering the ROA and RONW this is a well managed company. Disclosure: Invested from 1170 with 10% of total funds and hoping to gradually bring it down to 5%, so that this stock can be held permanently even beyond the bull market.

3 Likes

This is ultimate bull market leveraged story. I missed it @300-400 levels but now my other stock Edelweiss is outperfoming MOSL on the downside. IMO, Aspire goof-up is already discounted. Given the badgering all brokerage stocks have got recently suggests that the market is worried about decline in trade flows and MF inflows. Given the political scene the fear is legitimate that the bull market is over. If the hypothesis is correct, there will be more downside for sure. However, the way MOSL is ramping up its equity biz in AMC and wealth mgmt makes the current price appears too tempting.

Disc: No holding

I find it difficult to agree that it is a leveraged story. The debt equity ratio is only around 3, which is not very much, also considering its housing finance portfolio and the fact that all finance companies have a ratio of 5. But the company Edelweiss you are talking about is overleveraged at around 8 times with an interest coverage ratio of less than 1.5, which is extremely dangerous. Edelweiss has issued a lot of Esops this year and taken Qip funds and give a poor return on asset of around 1.3 and they have poor ROE too. The return on assets of Motilal is exceptional even from 10 years back. Motilal is growing at around 50% and if your theory of bull market being over is correct, it will be seen in q4. I still think that this is only a bull market correction. The stock had not corrected this year and I see it as a normal correction. One thing I don’t like about this company is that they have a policy of giving 25 to 30% dividends and I would have preferred a share buyback, considering the class of Ramdeo Agarwal.

4 Likes

Instead of growth,ROE, D/E why are we ignoring 6% GNPA which could eventually increase to 10% GNPA in coming quarters? For any financials,bad asset quality, credit cost could kill an institution.I thinks with 6% GNPA ,it is still overvalued in Book value term…

3 Likes

There are times when one considers all aspects and takes a position. Now or after a month? But when all expectations of good performance are met, markets won’t wait to give a good entry.

Looking at the 66% profit growth from previous quarter is one way of looking. Looking at the 4.6% NPL in the housing business is another way of looking. In one case the glass appears to be half full and in the other case, the glass appears to be half empty. Balancing the two is the art of investment.

In the conference call, Ramdeo Agarwal informed that they have shown more NPL over and above the statutory requirement, to be on the safe side. Also he informed that he could have shown profit in this business but refrained from doing so. A company may goof up, but how they approach it shows the quality of the management. The 66% growth is in spite of the housing finance loss. What a business!

4 Likes

You got me wrong here! When I say leveraged to the bull market , it is not about balance sheet but the trend in the market. Brokerage and capital market contribution is disproportionately high for MOSL. Well, I am still ok with holding Edel as some of their Biz like ARC is counter cyclical and a true diversification. Just one deal like Binani cement will make 500cr of profits for them. Ex- insuance RoE has already moved beyond 20% +. They are NBFC with a difference and not much impacted even if bull market gets over. Coming to MOSL, even if they have to writeoff 10% of assets in Aspire, they would be comfortable since they have 700cr worth of unrealized profits. I think they will definitely exit this biz at an appropriate time and focus on equity biz in consistent with their branding.

2 Likes

Will the famous buyer of stressed assets, itself become a stressed asset? ROE s and debt equity ratios are calculated on the entire business and not by keeping insurance business separate. Book value increases by 15% and not 20%.

In that sense Edelweiss is risky. A perusal of Edelweiss annual report talks about a lot of Off balance sheet assets which is a jigsaw puzzle. If you can put 20% of your funds into Edelweiss without fear in your heart, then go for it. I was 20% invested, but sold off, due to fear. Motilal is better leveraged and growing faster. In fact if you exclude investments and cash, the leverage is nil as per the latest investor presentation. With aum of just 8000 crores last year, it has to multiply several times to become a 1 lakh crore ki kahani. It is available at an EV/EBIT of just 18 times based on Fy17 numbers and by estimate of Ambit capital supposed to grow by 50% in FY 18

and 19. With Motilal, the bet is on Ramdeo Agarwal, the master of compounding.

2 Likes

Regarding '“Above the statutory requirement”" every financial institution shows, it is very normal.Moreover Provisioning of NPAs does not happen in single quarter, it will keep happening still all the NPAs 100% provisioned so impact on the profitability is just started and tip of the iceberg .When the loan book growth will be stopped then actual NPA amount will pop up,

1 Like

There is 700 crores unrealised income from gains in equity portfolio which will be taken into profit in FY19. Ramdeo agarwal has mentioned that the company is undergoing such exponential growth that he will not the able to predict the upside in next quarters earnings. This is similar to the 2003-07 period where the business made exponential gains. So there is unrealised income and exponential gains in FY19 to take care of any NPAs. Running a HFC is not rocket science and should be brought under control. Q4 result declaration today.

1 Like

If inflow to MF reduces, govt / SEBI pressurize to reduce expense ration on MF, what will be impact on profitability of wealth management companies like MOFS?

In the long run, I am quite optimistic about this stock. The particular reasons for this optimism are leadership of Raamdeo Agrawal,past good returns,skin in the game. Even the portfolio of Motilal Oswal mutual funds have selected few quality stocks.showing a blend of consistent performers & emerging companies.