That helped, Thank you

My few cents post Q3:

Paints segment slowed down, but thanks to the new plants at Mysore/Vizag, the overall numbers look decent. Management expects a better Q4. The company plans to add to existing capacities in a staggered manner over the next 4-5 years, which would support volume growth in the long term.

Food segment has been flat YoY, but the company has added a number of new clients and entered into new industrial segments which could further add to volumes. Management expects F&F sales to grow 35-40% for FY20, and become 2.5x in the next 3-4 years.

Lubes has been a dampener, which can be attributed to the auto segment slowdown.

Overall, the management seems confident about 20% growth over the medium term aided by systematic capex and expansion into high margin F&F categories. Mr. Rao is very open with his answers and positive about the overall business. The stock has been consolidating for a while now, and any positive surprises in Q4 should help with a re-rating. The removal of entire share pledging by April 2020 is an evidence of the promoters vision to work towards the benefit of shareholders.

I avoided the quantitative details to keep this crisp, details of which can be found in the concall transcript.

Any thoughts welcome.

7 Likes

Q3FY2020 Concall

For the question on pledge, Management clarified that the pledge is from non core promoters (Not for the company operations) and they have been advised to revoke the pledge by April even by selling their stake. He further clarified that this advice was given to them to remove unnecessary speculation on the pledge in the market. This shows the sensitivity of the management to market movement of the price.

3 Likes

Release of Pledge

@vivek_mashrani Are you still tracking this company? IMO it’s an excellent proxy to the consumption theme (strongly underscored by the foray into FMCG) with immense potential as a market leader in rigid packaging. The promoter has been buying recently as well.

Thanks!

One of the main promoter bought around 70000 shares and

3 promoters (with minor holding )sold around 3 lakhs shares in last 2 months in open market

Main promoter has explained and given heads up in Q3fy20 concall about non core promoters selling shares to clear the pledge. Main promoter said he has advised all promoters to clear pledge by April.

1 Like

Hi

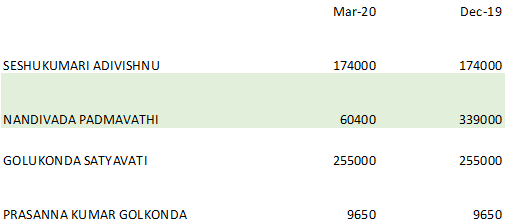

The pledged shares fell from 7.97% in Dec 2019 to 5.19% in March 2020.

One of the promoters reduced.

Pledged shares below

Rgds.

Hi,

How much of a pain in numbers for the next 1-2 quarters due to the reliance on Ice cream packing in foods ( ice cream industry has taken quite a hit ) and slow-down in new infra projects also affecting the paints business ( https://www.bloombergquint.com/markets/the-significant-risks-that-turned-goldman-sachs-bearish-on-asian-paints )

Hi All, my first post on VP.

Business overview:

- ~35 year old Company, makes injection molded plastic containers (rigid packaging) with in-mold labelling (IML) technology. IML is the process by which labels and parts are created in the same step. Also has other printing techniques such as heat transfer labelling and off-set printing that are done as an extra step after molding of part is completed

- Three main customers segments:

a. Paints: Enjoys good wallet share with Top 4 (Asian Paints, Berger, Akzo and Kansai)

b. Lubricants: Customers include Castrol, Exxon, Shell, BP etc.

c. Food and FMCG packaging: Ice-cream makers, edible oil maker, dairy products makers, some customers - ITC, HUL, Cadbury, Amul etc. - Brief financials (which justify worth looking into further):

a. 5 year revenue, EBITDA and PAT CAGR range: 12-15%

b. Consistent EBITDA margins in the high teens

c. Mcap – INR 800 cr, revenue – INR 400 cr, EBITDA – 70 cr, pat – 30 cr, debt – working capital 80cr, term debt – 25 cr

d. ICRA A- rated - Key Promoters: Well educated owners who seem to have been running tight ship on operations. Also second generation also into business

a. J Lakshman Rao (JLR) (MD) (Main promoter who looks at marketing and finance and who usually frequents investor calls)

b. Subramanyam (DMD) (Looks at mold design / production / manufacturing) - 7 plants across India. UAE plant shut-down after Company ran it sub-optimally for ~3 years (did not get enough orders from clients as envisaged earlier) (injection machines have been relocated to India and been put to use for making edible oil packs instead. Company has taken a write-off of ~12 cr, initial investment was ~50 cr)

Value chain:

- Key raw material: Polypropylene (main supplier is Reliance Industries), labels & other consumables (form the balance RMs)

- MTP operations are integrated for injection molding and label making. Sales is direct to customers. The robots and tooling required for IML process are made in-house

Business:

- Promoter and management quality: Feedback from concalls is that Promoter is generally on top of business numbers and also of emerging trends. JLR seems to be the key man driving business and bringing in new clients

- Business key investment themes:

a. Largest IML rigid packaging company with capabilities of in-house mold design, robot making and labelling – Helps in efficiently managing production & supply of different SKUs, cost of operations lower (compared to importing robots, outsourcing labelling)

b. Blue-chip customer relationship established over several years (Asian Paints contributes 30-35% of revenue and is core customer)

c. Attractive industry growth prospects

i. Consumer play that can mimic growth of underlying paints, food and FMCG industries

ii. Premiumisation in packaging leading to conversion to IML packs (% of food & FMCG business has increased for the Company from 5% 7-8 years back to ~20% now). This will also be margin accretive as food & FMCG packs are sold at higher realisation

Key risks: - Is this a growth trap? – Can Company keep growing at 15% topline? Lube growth may bring down overall growth of ~10-12% growth of paints + Food/fmcg

a. Growth may be supported by conversion into IML packs from paints and food & fmcg clients. Currently food & FMCG contribution is 20%, another 20% increase can take EBITDA margin up by ~2%). Need to assess ease of switching by speaking with fmcg players. How big can IML get In one of the concalls, it was mentioned that paints is a 2000-2500 cr market, lubes is another 1000 cr market, food + fmcg could be 20000 cr - Client concentration: Top 5 contribute 60-70%. Need to diversify volumes to more customers.

a. May be difficult for AP to shift out volumes to competitor, but gradual shift-out to Hitech others may be possible but would categorise as low threat - Technology: Need to assess how advantageous is IML over other packaging/labelling techniques. Also Company claims to be the only player to have figured out how to make IML packs successfully at scale to its clients. Need to dig deeper as to why it is so difficult to replicate

- Can company sustain EBITDA margins: Margins seem to be consistent historically. Company claims to having monthly reset clauses based on a certain RM price fluctuation

- Regulatory ban on plastics: Currently not affected. Crackdown on single use plastics/thermocol not related to Company. Any future ban on multi-layer plastics of higher microns will have to be seen. Need to assess what % of Company’s business is <50 microns, 50-200, >200 etc.

Financials and valuation:

Want to attach an excel however not allowing new users to do so

15 Likes

Management walking the talk. Continuous release of pledged shares.

2 Likes

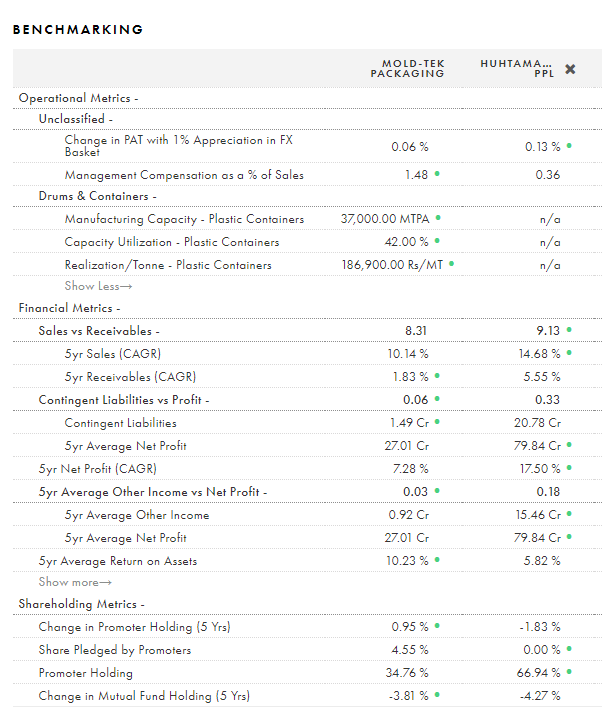

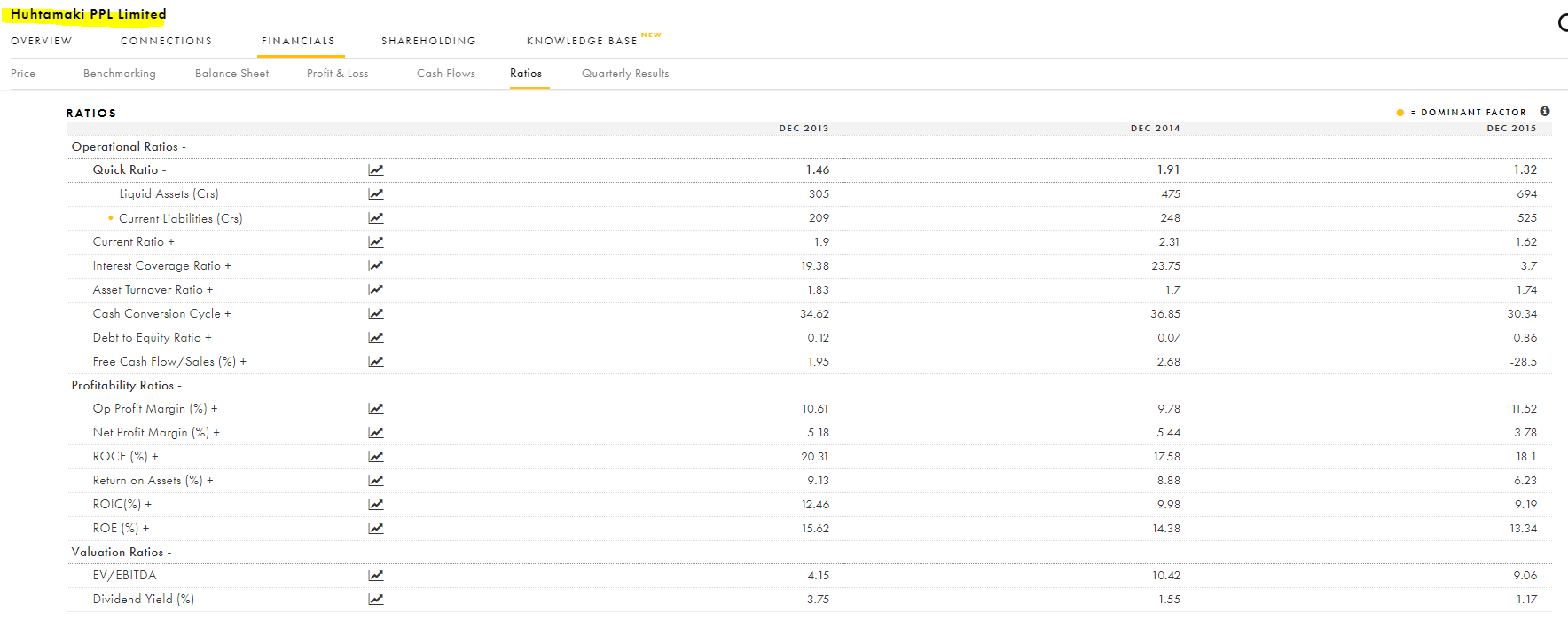

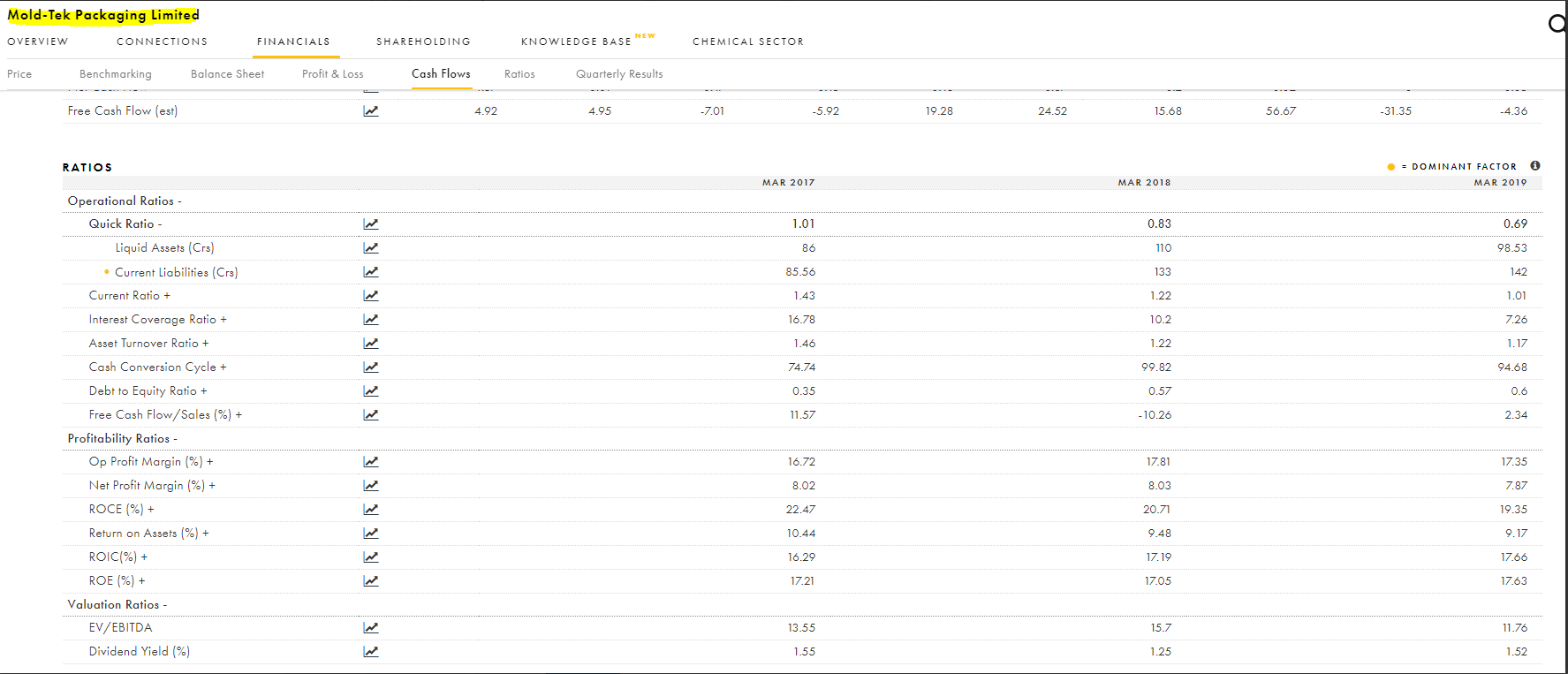

Can someone share their thoughts on like to like comparison between between Moldtek and Huhtamaki PPL ?

What software have you used?

It is Tijori Finance .

2 Likes

Hi

A rights and a warrant issue.

More details here.

Rgds

1 Like

As per the letter/announcement

For every 50 shares of mold-tek packaging you will receive 1 rights equity and 6 warrants.

Rights equity is at a price of 180 ₹ and same be subscribed at 45 ₹. These shares are already credited to account and trading at 227.4 (closing on 30th Oct). Which give the value of rights share at 272.4 ₹(227.4+45) which is slightly above the market price of equity 260.7 ₹.

Warrant will be issued at warrant price of 184₹ per warrant which means we have to pay 184₹ to convert warrants into equity within the warrant expiry date which is 18months in this case. These warrants are not yet credited to account. (Others please confirm and any info on when they will credit ).

NRI’s need permission from RBI to subscribe to both Rights and Warrant.

Also the difference between Rights and warrants is that Rights is short term instruments which is converted to equity in short span (within few days) and warrant is long term instrument which can be conveterd into equity within few months (18 months in mold-tek case) and both are traded on exchange.

Please correct me if I am wrong.

Disclosure: Holding since long

And planning to sell both Rights and Warrants as I am an NRI (need permission from RBI to subscribe)

Can anybody please confirm my above assumptions?

Further, why rights equity is trading above the share price today ?

I am searching for same answers.

The analyst who recommended the stock say he does not know.

Have you got warrants credited to your account

I have only shares credited.?

I suspect mgmt may be planning to convert warrant to equity. Thats the only way I can explain daily upper circuit from 100 to 465