@sammy11 have seen this with few more companies . One company I remember correctly is vidhi dyes . No wonder their valuations r hugely underperforming (60 to 70%) compated to relaxo against financial quality of business difference (25-30% if one seems difference in financial parameters like ROCE, growth, leverage etc). Its a ballpark qualitative number but I hope you got my message. Market punishing corporate governance through valuation . Disc : only a trading stock for me .Positions purchased n sold in last 6 months

3 Likes

Mirza International has almost doubled in the last 2 months, taking the valuation comfort away. The problem that it has to cope with from hereon is that exports that constitute at least 2/3rd of Sales are facing strong head winds, while domestic sales that are growing well constitute less than a third of Sales. Perhaps a case of the tail wagging the dog! These headwinds are perhaps getting reflected in Q4 results. Things will probably change going forward over the next 3-4 years with Indian operations gathering scale, but there is a possibility that the low hanging fruit may have been picked.

The issue of “guarantee commission” seems like an entry through the back door! The promoters are better off adding the guarantee commission amount to their remuneration, but perhaps there are restrictions on director remuneration. I can think of numerous co.'s where the directors have given personal guarantees for debt taken by the Co., but I can’t think of too many instances where they have been compensated for giving their personal guarantees by an amount almost equal to their remuneration! Perhaps the problem is also one of there being just too many Mirza’s running the Co., with some still to make it to the board!

Another concern is that most Sales to UK are made to a Co. owned by the promoters in their personal capacity, which then distributes the sales. Hopefully the mgt., with an eye on the market cap should correct some of these legacy issues going forward.

What is however, going well for the Co. is that the brand Red Tape is holding firm. With Bond Street gathers traction, the mgt. does seem to have the wherewithal to scale up the Indian operations with very limited capex.

Dis: Booking profits gradually.

11 Likes

So the last year acquisitions of Genesis footwear P Ltd. a related party supplying shoes has not done any good to the company but only adding to the issued share capital. Rather than expected increase in overall profit as the Genesis profit was expected to be simply getting added to the Mirza’s profit, the profit has declined this year in comparison to last year. Strangely there has been the significant increase in the purchases of FG as compared to last year.

Sold my position.

Mirza International LTD

Mirza International is the first preferred Indian supplier of leather footwear to global brands since last 25 years with 37 years of manufacturing operations established in 1979. It is also the first premium lifestyle Indian brand of footwear to have a major market share in the fashion and design conscious UK market, and it is the first preferred supplier of leather footwear to UK from India.

“RED TAPE” the flagship Mirza brand is the leader in the mid segment men’s fashion footwear in the UK market.

Market Presence

- Brands :-

RED TAPE

Oaktrak

Bond Street (Red tape London)

Yezdi - Network :-

140 + Brand Shops

185 Shop in Shop with presence in 73 cities

Three distribution branches in India

“www.amazon.in” online website to accentuate sales - Products:-

Leather

Footwear

• Casual

• Formal Shoes

• Polyurethane (PU) shoes

• Sportswear

Garments and accessories with a range of fashion formals, casuals, T-shirts, shirts, jeans, and accessories like belts and socks

In 2016-17 , Launched two new sub-brands of REDTAPE:

- Bond Street

- REDTAPE Athleisure (Sports range)

Brand Presence

REDTAPE is now a full-fledged lifestyle brand, with garments and accessories under its umbrella. Over 1.20 million pairs of red Tape shoes are manufactured in a year and overseas revenue from REDTAPE increased by over 35% on a year-on-year basis . 32% of total REDTAPE sales in FY 2016-17 came from the matured markets of UK and USA. REDTAPE store count increasing 30 stores annually 60 REDTAPE stores to be opened in the next two years to take store count to 200. This brand extension has enabled us to increase our market share and position REDTAPE as the one-stop shop for men’s dressing. Domestic sales of REDTAPE brand increasing by 28% in FY 2016-17 on a year-on-year basis.

Oaktrak is another brand under which the Company sells leather footwear to global retailers. The brand stands for style and comfort and is targeted at the niche customer base of senior professionals

Bond Street provides affordable polyurethrane (PU) shoes to address the growing demand for value-fashion footwear in Tier 2 & 3 cities. By offering excellent quality at affordable price points, we aim to meet the expectations of the mass segment.

REDTAPE Athleisure Sports range We are providing high-quality athletic footwear which is priced at far lower price points than existing leading international brands. With the young population becoming increasingly conscious of health and fitness and embracing casual wear as part of their lifestyle, the market for sports footwear has been growing at a fast pace

Overseas Presence

500+ MBO Stores in USA selling RED TAPE. Mirza brands have an increasing presence.

1200+ MBO Stores in UK The Company has garnered a 25% share of the men’s leather footwear in the mid segment category in UK selling RED TAPE or Oaktrak. . In UK, Red Tape is priced in the mid market segment that is the largest single market segment. Oaktrak our other brand is priced as a niche brand of formal footwear

Products and brands of the Company exports across 26 countries and 5 continent including some of the most fashion and design conscious markets of the world like USA, France, Germany, West Asia and South Africa… 70% of our total revenue is derived from sales in international markets

Online presence that caters to the now emerging and popular cyber sales segment 75% of Mirza International’s total revenue is derived from overseas sales.

Apart from its proprietary brands, the Company also supplies quality footwear to international companies that sell them under their own labels. These international labels come to Mirza due to the ability to effect quick deliveries; offer great build quality and maintain economic prices thanks to the integrated nature of our manufacturing facilities

Indian Footwear Industry

The Indian footwear industry, comprising leather and non-leather segment, is pegged at 25,000 crores with a CAGR of 15%.

India is the 2nd largest footwear manufacturer in the world, producing more than 22 Billion pairs footwear per annum out of which 90 % consumed internally. It is also the second largest producer of leather, next only to China.

Abundant availability of raw material and local talent, and competitive wage levels make India an ideal base for manufacturing leather goods. In terms of exports too, the leather industry is among the top ten foreign exchange contributors to the country’s global trade. Footwear export accounts for 45% share in India’s total leather and leather products export. On the home front, 1950 million pairs are sold in the domestic market. The Footwear product mix constitutes: Gents 55%, Ladies 35% and Children 10%.

Footwear exports from India have grown at a CAGR of 20% in Indian Rupee terms during the last five years backed by growing demand from European nations and increasing focus of main importing countries to shift sourcing from China to other low-cost producing countries.

Shopping pattern of India is expected to witness a growing shift towards aspirational and branded products. Further, the implementation of the GST will boost the business of organized players, especially in the low price segment.

India’s sportswear market, including sports apparel, footwear and accessories, grew by 22% during FY 2015-16, surpassing the segment’s global growth of 7%. The Indian market is expected to continue this strong run by growing at a CAGR of 12% until FY 2020, driven by the young Indian population’s growing interest in fitness and sports. Within the sportswear market, footwear is the largest category, holding 60% of the total market.

Indian Leather Industry

With an annual production of 2 billion sq. ft. of leather, accounting for 12.93% of the world leather requirements, India is the second largest producer of leather next to China. Employing nearly 2.5 million people with 30% being women, the industry offers tremendous potential for employment opportunities driven by the growth in global demand for leather products, especially in footwear, furniture, interior design and in the automotive industry, among others. Countries in the European Union account for nearly 56% of India’s total export of leather and leather products, Germany, UK, Italy and France being the prime markets. USA is the other major market for Indian leather exports. Footwear holds a major share of about 49% in India’s total leather & leather product exports with an export value of USD 2775.75 Mn.

Operations

We have 6 Fully Integrated IN house shoe production Facilities and are equipped with an In-house Tannery. The plants are supported by number of dedicated ancillary units and have The capacity to produce 6.40 million pairs of shoes per annum with 80 % capital utilization in FY 2016-17. Mirza International has two design studios located in India. Company operate 1 modern 70,000 Sq Ft warehouse to serve E-commerce channels and 3 distribution branches.

CRISIL has Reaffirmed its rating to the Company as ‘CRISIL A/Stable/CRISIL A1

Team of 40 skilled designers has intimate knowledge of market trends and fashion

Mirza International’s tannery is the largest in India and is one of the least polluting tanneries in the world.

Business Model

Company Supply Chain Management ensures that the right design is available at the right time, every time and every where. Company design center is connected to manufacturing with CAD/CAM facilities to ensure that the time gap from design to production is minimized.

Company has marketing offices and warehouses and a distribution network in United Kingdom to ensure availability of stock at all times. Pricing targets both the upscale mass market, through the REDTAPE brand, and the niche customer base of discerning senior executives, through the Oaktrak brand. The mid-market pricing for REDTAPE has helped us capture a large share in some of the world’s top consumer markets.

Company Brands are focused on the young adults, a customer segment which is seeking trendy and quality products at reasonable prices. By leveraging the channels of EBOs, MBOs and LFS, we are expanding our reach in an aggressive manner. Through the launch of Bond Street and REDTAPE Athleisure Sports range, we have forayed into new categories, namely the PU segment and sportswear. This will enable us to make inroads into the entire range of men’s footwear and expand our total addressable market.

Marketing mix comprises in-store publicity, print advertisements and in-flight magazine. In FY 2016-17 company spent 9.37 Crore towards advertising compare to 6.7 Crore in the previous year. This translates to 4% of our domestic revenue in the review period. For the current fiscal, company is targeting to increase our marketing budget even further to reinforce our brand and deepen customer engagement

Design advantage :- With a team of more than 40 highly skilled designers, company release 1,000 new designs every year. Of this, 300 new designs are for shoes, 600 for garments and 100 for belts and other leather accessories. The number of new designs keeps us fresh in the mind of consumers. To optimize all resources and minimize the gap between design and manufacturing, our design center and manufacturing units are connected by CAD/CAM.

Supply chain agility :- A huge network of own brand sales and white label exports requires an extremely efficient supply chain, to prevent inventory build-up and very fast design-to market transition – in our case, it takes only 25 days. As fashion changes frequently, it is a race against time for any manufacturer to keep up with consumer demands. Mirza International’s agility in this respect is proved by our global success

Growth Drivers

Abundant availability of raw materials :- Endowed with 21% of the world’s cattle and buffalo and 11% of the world’s goat and sheep, abundant raw material availability is the key driver to the growth of the leather industry, enabling production of 235 million pieces of hides and skins.

Focus Sector :- The Government is providing various incentives to the leather industry in Foreign Trade Policy and allowing concessional Duty for import of Machinery. Department of Industrial Policy and Promotion (DIPP) is implementing ‘Indian Leather Development Programme (ILDP)’ consisting of six sub-schemes .

Central government scheme such as “Skill India” National Skill Certification and Monetary Reward Scheme of the National Skill Development Corporation add skill labour to serve leather industry. “Make In India “ campaign run by central government promotes leather manufacturing in country with subsidies.

Growth Strategy

This year Company has adopt the strategy of market penetration by which we have launched our new Brand “BOND STREET” which seeks to have a mass appeal by providing fashionable footwear at very low price points

Your Company already set a benchmark in leather shoes market, this year your Company has launched Athleisure Sports range which is unique in market using fly knit technology. This will help in setting new benchmark in the market and adding more customer base

Company also acquires entire stake of HI-LIFE FABRICATORS PRIVATE LIMITED by making it Wholly-owned subsidiary of Mirza International Ltd

Challenges

Product designs not aligned to international requirements,

Lack of warehousing support from the government

Tanneries not conforming to environmental regulations resulting in closures

Fluctuation in international prices of leather

Unawareness of international standards

Risk

Major risk is depreciating of rupee again dollar due to major segment working toward export.

Shortage of Skilled Labour :- It is estimated that 90% of the total work force (directly or indirectly) is either semi-skilled or unskilled Hon’ble Prime Minister has placed due importance in this regard. As a result of this, the Leather Sector Skill Council has been established under the National Skill Development Corporation (NSDC) to ensure training of manpower, both in hard and soft skills.

Raw Material Base :- With the Indian leather industry aiming to achieve the export target of USD 18.5 billion by 2020 and the domestic market for leather, leather products and footwear projected to double from the present value of USD5 billion, leather requirement will considerably enhance in the coming years. Thus we need to be prepared to meet the challenge of shortage of raw materials faced globally. For this, we have to identify new leather sources in overseas countries. To augment domestic availability of leather, the proposed Mega Leather Cluster projects will play a major role in enhancing internal raw material base.

Outlook

Company seek a mix of horizontal expansion into new markets and vertical penetration in markets where they are already present. With footwear purchase trending towards online e-commerce, they are also seeking to augment our digital marketing initiatives and increase our presence across multiple platforms for easy accessibility and visibility

After entrenching its position in leather market, now the Company focused at replicating the leather market success in Sports Shoes market

Extend Brand offerings beyond footwear to allied areas of garments and accessories

Online platforms now offer a new growth engine for retail companies, cognizant of this, the Company will be looking at engaging with more customers through a well-thought digital strategy

The sustained low price of oil and other commodities helps our bottom line, definitely. Then there is the sheer amount of attention drawn to Indian manufacturing by the ‘Make in India’ drive. If inflation stays under control, or comes down, there may be banking rate cuts, helping businesses and thus generating employment and consumption. Any number of things could work in favour of manufacturing as a whole, and for consumer goods, specifically.

For sports shoes, the designing is being done in-house but the manufacturing has been out-sourced to China and vietnam. However, going forward, once our sales reach a certain scale, we have plans to manufacture them at our own facilities.

Corporate Social Resposibility

Company is doing very good in CSR by supporting to Quami-Ekta Inter College in Unnao District, Uttar Pradesh, for providing education to students living in remote areas. Company in association with Pride Aducation, an NGO in the field of education and sanitation, had constructed public toilet blocks in the rural region . Company is the major contributory to the Mirza Charitable Hospital Ltd. Company distributed 25 sewing machines to women to enable them to become self-reliant and earn their livelihood.

Financials

Segment Wise

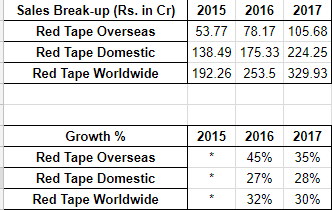

The Company’s business segments are primarily Shoe Division and Tannery Division. During the year under review, revenue from the Shoe Division increased to 843.56 Crore as against 818.86 Crore in the previous year. Revenue from the Tannery Division was 210.96 Crore for the year as against 240.88 Crore in previous year.

The Board proposes to transfer the amount of 7.50 Crore to General Reserve, as compared to 8.00 Crore transferred in the previous year

Company has disinvested its 25% stake in Azad Multispeciality Hospitals & Research Centre Ltd. resulted into bringing down its holding from 41.67% to 16.67% as at the end of financial year 2015-16.

Overseas Revenue

Revenue from overseas sales stood at 650.68 Crore as against 691.71 Crore in the previous year. While revenue from UK operations decreased from 464.26 Crore to 452.04 Crore in FY 2017, showing a decrease of 3%, USA operations have increase in the revenue going up from 89.51 Crore in the previous year to 92.23 Crore in the year under review, showing a growth of 3%… RED TAPE online sales was 44.69 Cr in 2016-17.

Domestic Revenue

Domestic Sales stood at 285.88 Crore as against 237.01 Crore in the previous year thus showing an increase of 20.62% REDTAPE Domestic Sales – 166.52 Cr from Footwear , 57.73 Crore from Garments & Accessories

Quarter Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17

Sales 252.2 250.26 228.03 205.19 252.08 240.4

Sales YOY % 1.033571 -2.03554 5.481543 0.224686 -0.04758 -3.9399

EBITDA 43.78 37.96 39.72 39.22 44.13 42.44

EBITDA YOY % 0.83 -7.01 16.04 -25.05 0.80 11.80

Net Profit 20.03 16.46 17.17 17.65 20.41 19.35

Net Profit YOY % 11.15427 2.746567 13.78396 -39.0749 1.897154 17.55772

Income Statement

Rs in Cr Mar-13 Mar-14 Mar-15 Mar-16 Mar-17

Sales 643.4 706.97 918.34 925.75 935.68

YOY % 15.60922 9.880323 29.89802 0.806891 1.072644

EBITDA 115.55 121.44 141.98 170.54 160.51

YOY % 32.06 5.10 16.91 20.12 -5.88

EBITDA % 583.50 -84.10 231.81 18.93 -129.24

PAT 43.44 43.37 51.16 78.09 71.2

Cash Flows

Rs in Cr FY13 FY14 FY15 FY16 FY17

Cash Flow from Operations 89.39 48.38 97.34 90.28 113.62

Cash Flow from Investing -58.1 -53.67 -58.93 -33.94 -36.34

Cash Flow from Financing -39.4 7.78 -39 -50.65 -82.22

Balance Sheet FY-13 FY-14 FY-15 FY-16 FY-17

Borrowing 167.4 211.96 217.7 205.07 156.02

Other Liabilities 89.12 119.3 129.67 116.39 110.03

TOP TEN SHAREHOLDERS

Name % of total shares of company

EPSLON ENTERPRISES PRIVATE LIMITED 0.29

KITSON ENTERPRISES PRIVATE LIMITED 0.44

PERPETUAL ENTERPRISES LLP 0.55

PARAG MEHTA 0.70

LUKE SECURITIES PRIVATE LIMITED 0.41

IL & FS SECURITIES PRIVATE LIMITED 0.28

HSBC MIDCAP EQUITY FUND 1.03

KOMAL VINCOM PRIVATE LIMITED 0.41

QUANT CAPITAL HOLDINGS PRIVATE LIMITED 0.57

QUANT CAPITAL SECURITIES PRIVATE LIMITED 0.62

Note :- Mr. D.C. Pandey has resigned from the office of Company Secretary and Compliance Officer of the Company and succeeded by Mr. Ankit Mishra on 15th March, 2016.

Mr. Irshad Mirza was resigned from the office of Chief Financial Officer of the Company on May 30, 2016. Mr. V. T. Cherian was appointed by the Board of Directors in place of Mr. Irshad Mirza as Chief Financial Officer of the Company on May 30, 2016.

Investment thesis

Mirza International is first preferred Indian supplier of leather footwear to global brands since 1979 plus its flagship brand Red Tape is lead in mid segment men’s fashion footwear in UK market. The Company has garnered a 25% share of the men’s leather footwear in the mid segment category in UK selling RED TAPE or Oaktrak.

Deep Distribution- It has 140 + Brand Shops , 185 Shop in Shop with presence in 73 cities, 3 distribution branches in India and also extensive distribution channel in export countries especially USA and UK.

Industry tailwinds - Also Indian footwear industry is growing with CAGR of 15%, and sportswear market which company is focusing on is growing for more than 20% as discretionary spend is increasing in India. So all in all there is a huge runway ahead and further GST will be favourable for our company to grow faster.

Focus Area - Now, Company Brands are focused on the young adults, a customer segment which is seeking trendy and quality products at reasonable prices, becoming more health and fitness conscious. On basis of this, Bondstreet and Athleisure Sports range has been introduced. It is in line with thought process of huge scope of growth for discretionary spend in India expected.

Bond Street provides affordable polyurethrane (PU) shoes to address the growing demand for value-fashion footwear in Tier 2 & 3 cities. Athleisure Sports range provides high-quality athletic footwear which is priced at far lower price points than existing leading international brands

Cross selling opportunities - REDTAPE is now a full-fledged lifestyle brand, with garments and accessories under its umbrella. This will help company to increase bill per customer and also addition of new garment customer and cross selling of products.

Operating leverage - It have capacity to produce 6.40 million pairs of shoes p.a with 80 % utilization in FY 2016-17. This gives a play on operating leverage plus at this 80% is a time when company can also raises its prices for increasing demand.

Innovation and Advertisement - It also has two design studios located in India. Company operates 1 modern 70,000 Sq Ft warehouse to serve E-commerce channels and 3 distribution branches.

For the current fiscal, company is targeting to increase marketing budget even further to reinforce our brand and deepen customer engagement. After entrenching its position in leather market, now the Company focused at replicating the leather market success in Sports Shoes market.

Expansion - REDTAPE store count increasing 30 stores p.a which will help to further gain market share.

Net debt free - Borrowings of company has reduced by around 30%, and if company progresses on similar lines ,it can be debt free in coming 1-2 years.

Company has disinvested its 25% stake in Azad Multispeciality Hospitals & Research Centre Ltd. resulted into bringing down its holding from 41.67% to 16.67% as at the end of financial year 2015-16. Company also acquires entire stake of HI-LIFE FABRICATORS PRIVATE LIMITED by making it Wholly-owned subsidiary of Mirza International Ltd this year.

Risk

Major risk is depreciating of rupee again dollar due to major segment working toward export.

Shortage of Skilled Labour: It is estimated that 90% of the total work force (directly or indirectly) is either semi-skilled or unskilled.

Fluctuations in prices of leather can also affect margins of company in material way.

Raw Material Base: Leather requirement will considerably enhance in the coming years, thus we need to be prepared to meet the challenge of shortage of raw materials faced globally.

Technical:

3 Likes

This company was brought to my notice by a friend recently who pointed me that few things seem to be changing rapidly for the company:

-

The branded contribution used to be small earlier but has been growing rapidly.

-

The company has been launching lots of new products and expanding the product portfolio. Its no longer just a leather company. Now they are into sports shoes (on the likes of Sketchers), apparels etc etc. One can get a feel of collection from here - Amazon.in : red tape sport shoes for men

I have personally tried these shoes and they look fantastic in look, feel, finish etc etc. I’m surprised at the price point they are available…seem to be a bargain.

- The company has been aggressively opening new large format stores (refer to concall for details)

Above things do get validated from the segment results of the company:

In 9 months FY18, the branded segment has grown at about 30% with good margins. The overall results have been flat as the company seems to be facing headwinds in export markets.

I feel the Red Tape brand has a good recall and presence especially in North India. Till few years back it used to be a small portion of the overall sales of the company but it seems to be growing rapidly. They also have lot of online presence and seem to be aggressive.

As its a B2C story, it will be great if members can do scuttlebutt on the product and new initiatives by the company and share their feedback.

Disc: Invested

19 Likes

@ayushmit 2 years back when they suffered from stagnation in Europe, they started focusing more on India (there is an article on woodland vs Mirza on how they started at same time n took reverse approaches on national vs international ). You are right , now they are getting aggressive on India by channel (online, stores) , by product line (leather shoe, sports shoe, accessories ). I had position in this last year and hence had studied . There is one major governance drawback I saw. Check their debt levels of last 5 years n related party transactions and % of money they have been charging for giving personal guarantees for the debt . First I do not think they should charge and even if they are charging, it should not increase disproportionately with respect to debt. If you add salary plus this income I think last year it stood somewhere around 15-16% of profit .

However, all said n done having personally used n feedback from others, leather shoes have excellent feedback. Last year they were launching sports shoes ,so, need to check . India business doing well n sooner or later Europe should pick up. They were supposed to set up a warehouse to cater online channel. Also, last year at 90 RS promoter was picking from open market. So at 117 rs with approx 10-12 times CFO at 0 growth , this is again getting attractive provided we can ignore the governance issues n factor it in valuation. How important do you think such factors are ? Disc: traded in last 1 year and in watchlist

5 Likes

The issue of commission on guarantees has gone to court before. Here’s one example - Commission paid against Guarantee by Directors in violation of RBI guidelines is not allowable

It quotes RBI Master circular - Reserve Bank of India - Notifications

Where personal guarantees of directors are warranted they should bear reasonable proportion to the estimated worth of the person. The system of obtaining guarantees should not be used by the directors and other managerial personnel as a source of income from the company. The banks should obtain an undertaking from the borrowing company as well as the guarantors that no consideration whether by way of commission, brokerage fees or any other form would be paid by the former or received by the latter directly or indirectly. This requirement should be incorporated in the bank’s terms and conditions for sanctioning of credit limits. During the periodic inspections, the bank’s inspectors should verify that this stipulation has been complied with. There may, however, be exceptional cases where payment of remuneration may be permitted

7 Likes

Nice report about Footwear industry. 2017 report.

Yes, like I said earlier, there are corporate governance issues. But I feel these things can get corrected or may get ignored IF the underlying business is innovative, strong and delivers growth.

In this case, its good to see that the company is doing lot of product introductions and category expansion (the co is not limited to leather shoes now…they have been venturing into casual wear, sports shoes, flip flops, apparels etc) + women segment will be tapped in coming year.

Along with this they are increasing their selling points - increasing stores (infact new stores are large format stores on the likes of big brands) + aggressive online marketing. Their Advertising spend has more than doubled.

Will they be successful or will it be sort of dis-worsification by trying to do too many things?? To get early insight, we all may try to do scuttlebutt and share our views on their new stores and products.

If they become successful (which seems to be getting reflected in recent nos) then stock may get re-rated too…as there are very few good consumer oriented stories with brand power.

11 Likes

There are two other serious concerns . Back to back two privately held companies merger , one already done and one in progress , with no significant improvement in the financials of the company so at the cost of minority shareholders. Secondly huge salaries drawan by the family members . Also there is no clarity who owns the Red Tape brand.

1 Like

Hi All,

I did some work on the two amalgamations, below are my inputs.

Amalgamation of High Life: This company owned a land in Noida, at which Mirza has a corporate office. Before the amalgamation, High life was a 100% owned subsidiary. It was amalgamated to simplify the corporate structure (Source: Q2FY18 concall) and as it was a 100% subsidiary there was no equity dilution from this transaction.

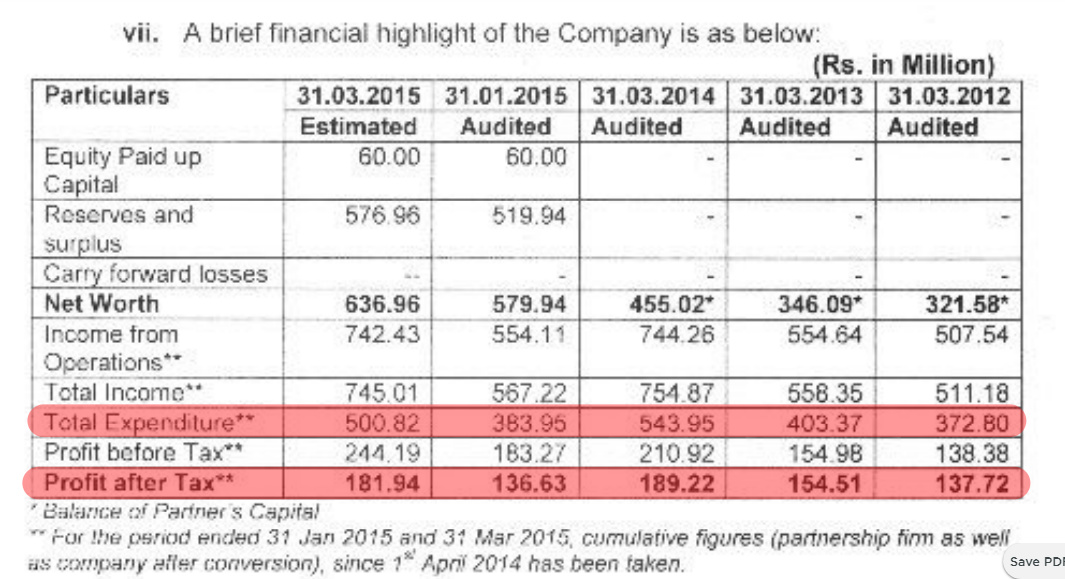

Amalgamation of GEPL: Genesis Footwear owned by the same promoter group was a partnership firm till 2014. It was later converted to a company in 2015. GEPL had majority of its sales to Mirza International. As per the scheme of amalgamation 92 shares of Mirza were given to the owners of Genesis for every 100 shares held by them. GEPL had good profitability of around 20 Cr (see below image for more financial details) and was valued at 315 Cr i.e. at a PE of 15- one can argue that a high price was paid for an unlisted entity but, on a brighter side a potential conflict was also removed for the future.

Now, investors have concerns that after this dilution no benefit was accrued in the financial performance of Mirza.

However, if one looks closely, topline could not have been better because in pre-amalgamation time Mirza was buying goods from GEPL. So, the expectation of higher sales is void.

Next, is the expectation of improvement in bottomline. Since, Mirza was buying goods from GEPL. Post amalgamation its RM cost should have come down. Here, I do see an improvement in numbers post-amalgamation i.e. in FY16 & FY17 (Please see below table). Therefore, I feel it is safe to assume that the improvement in numbers has come but the benefit is arguable…

Regards,

Yogansh Jeswani

Disclosure: Invested

15 Likes

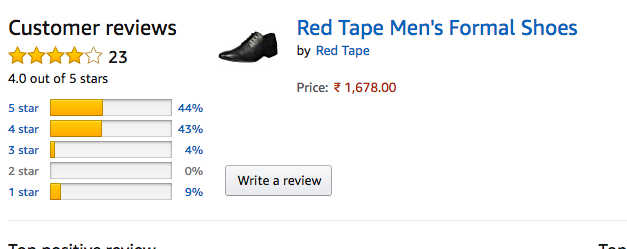

i spent last 30 mins going through the customer feedbacks on Red Tape brands at Amazon. Here is what I found -

- Most products have ratings > 4 but the total # of feedbacks are typically in low teens ; Only a handful that had more than 30 feedback

- For the leather shoes, there is a disproportionate share of feedback with rating 1 ; Many complaint about "poor product despite a good , well known brand ! "

- For the sports products, the feedback was generally good - neither too great nor too bad

1 Like

Thanks!

I have gone through amazon UK’s website to check Red Tape and Oaktrak’s reviews.

I am quite satisfied from the same.

You may want to check it out.

Sincerely,

django

1 Like

disc: invested with position less than 2 %

5 Likes

Regarding the Guarantee Commission, I spoke with the auditor mentioned in FY17 annual report.

Following are the comments from him:

-

Company has taken loan from only one bank i.e. Punjab National Bank. This shows how much trust the bank has on the company as generally for such a big exposure, banks form a consortium

-

Bank has demanded personal guarantee from promoters - and promoters obliged

-

For the risk the promoters are taking (due to offering personal guarantee), promoters are taking guarantee commission

-

Overall company’s corporate governance is ‘highly’ satisfactory

Above is a gist of my conversation with the auditor.

However this leads to more questions (which I did not ask):

a. Why is company taking loans from only one bank? Are other banks refusing to offer loan?

b. Why is the interest cost as % of total debt so high? Is this due to bills discounting?

(above are approx. numbers)

Humbly request all to share relevant facts and thoughts.

@ayushmit any comments on the above?

Thanks in advance.

Sincerely,

django

3 Likes

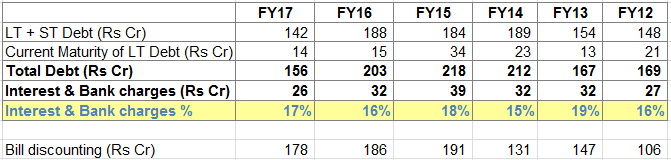

Below is snapshot from 2014-15 and 2016-17 AR. You already have the debt numbers. From 2014 to 2017 , we can see Debt has come down and personal guarantee against debt has increased . Defeats all logic to me and this is not some insignificant paltry amount

Even if they want commission against personal guarantee ,should not it decrease with decreasing debt rather than increasing. Are not fixed assets and cashflow enough as collateral ?

6 Likes

Hi @django - like mentioned by @suru27 the commission thing hasn’t been logical. Its definitely a corporate governance issue. However, like I mentioned in my earlier post, my focus is more on the underlying changes happening in the company. Can this company transform from a export oriented company to more of a domestic brand? There are definitely signs towards the same. lets see how much can they scale this up in a profitable way.

Regards,

Ayush

3 Likes

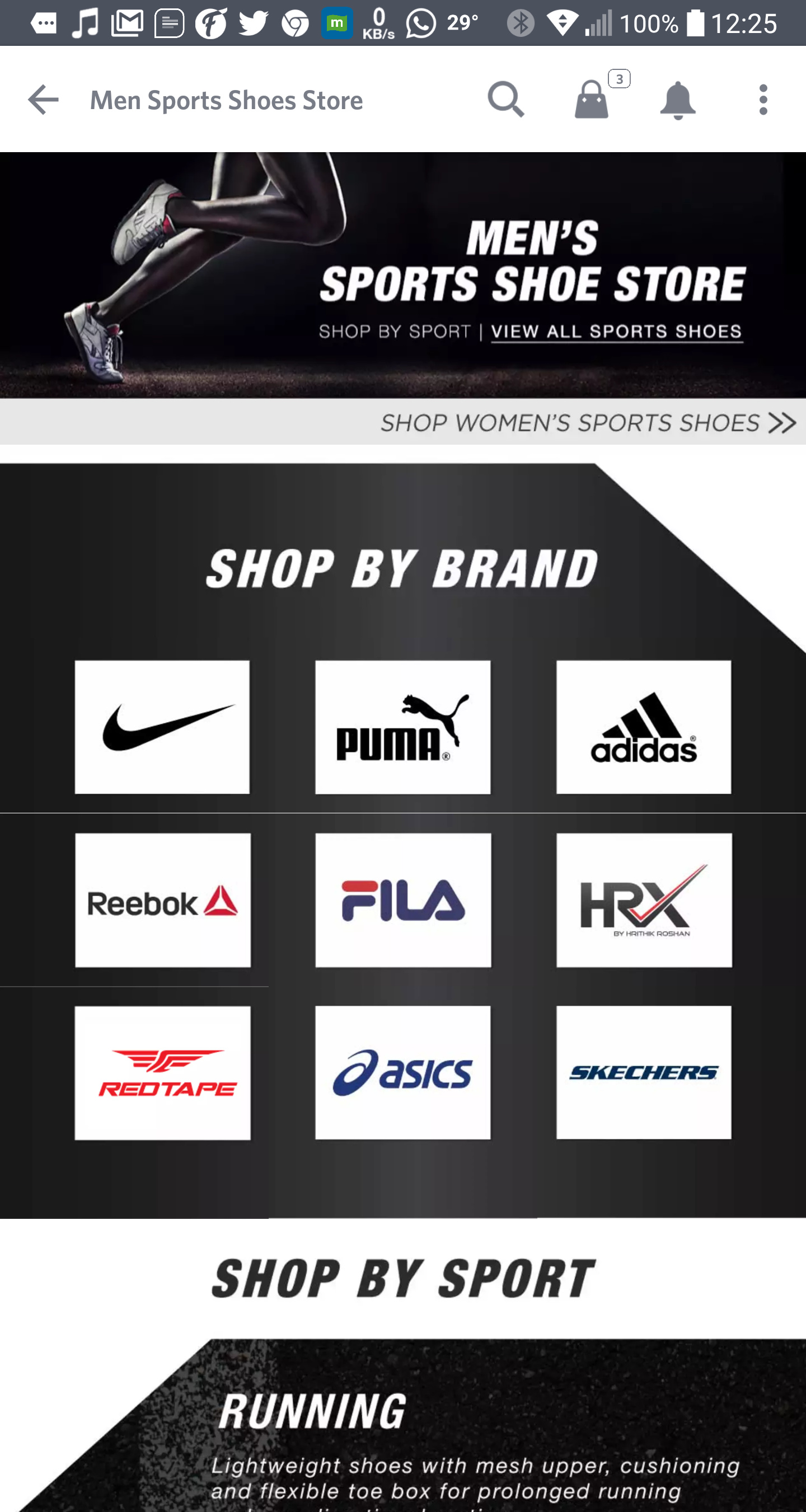

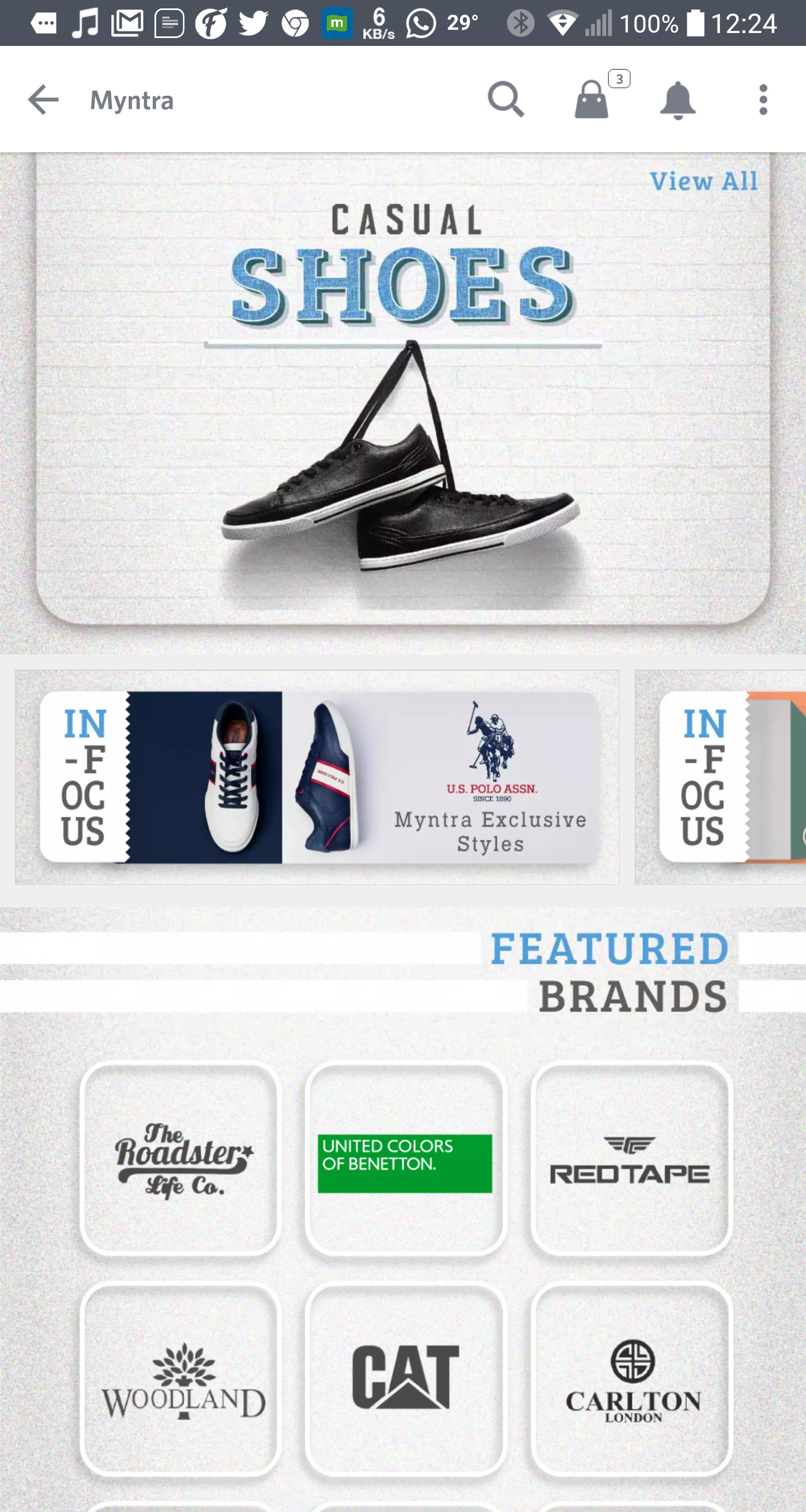

I do see this transformation happening. I don’t remember seeing RedTape brand prominently placed in Myntra’s “Featured Brands” before but now it resides alongside some marquee names. See this.

For Sports shoes, its alongside nike, puma, reebok and adidas and the only other Indian brand featured is HRX.

For Casual shoes, the only other Indian brand is a very new one - ‘The Roadster Life Co.’.

It is present in Formal shoes as well.

Also, I am noticing another fundamental shift happening in the clothing apparel and accessories sectors. I think Myntra has brought a lot of Indian brands to the fore and also a lot of new Indian brands like HRX, Wrogn, The Roadster Life Co. etc have launched and now compete fiercely with established names like Jockey, Adidas, Nike and Levis. People who may not have walked into one of these showrooms willingly now get to see them alongside popular names and that breaks a big barrier. I have personally tried names like these to somewhat replace Jockey and Puma stuff that I used to buy. I think there is a fundamental shift here in this space and we should keep a close watch.

Disc: Invested.

8 Likes

@phreakv6 @ayushmit Yes, there is no second thought that domestic focus is getting visibility . Also, in south( Bangalore) , I see redtape stores with both shoes n accessories. Coming to online, roadster n hrx have been huge success. Infact, roadster now has a physical store in Indiranagar , Bangalore next to Levi’s n all. That’s something.

4 Likes