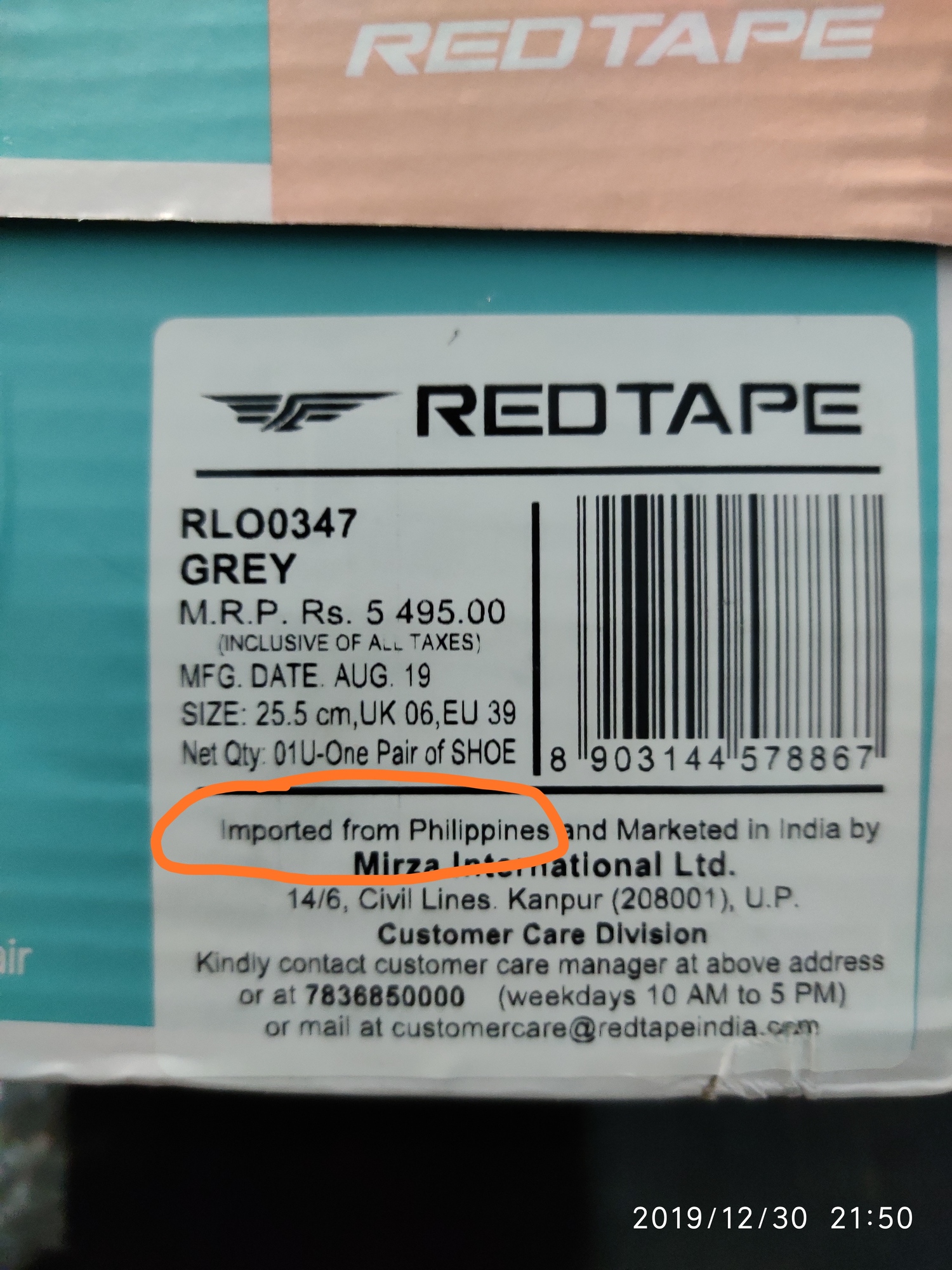

Just received a pair of ladies sports shoes online and observed as ‘imported from Phillipines and marketed in India’. What it means ?? I thought they are getting these shoes manufacted in India or Bangladesh.

2 Likes

Anyone has a link for Q2 earnings call / transcript ?

They are importing from white label / contract manufacturers in PH. I know this from a friend who is in logistics. So essentially they are trading apparels and sport shoes. Mirza production is still only focussed on leather products.

4 Likes

Anyone attended the AGM. Please update with any AGM notes. Thank you.

Good results!

2 Likes

Good results! Topline and bottom line has grown significantly. Eventhough margins are stable QoQ it has not reached high teens as 2-3 years back. Hope this will improve as company rationalises its SKU management.

There has been good reduction in inventories as well.

Redtape sales have grown in footwear as well as garments and accessories. Growth in garments and accessories is stunning!

Disclosure : Tracking

3 Likes

Just an observation : I noticed that their shoes were selling at very heavy discounts during the December 2019 month as compared to other products, like really heavy discounts. I asked for my size (UK 42) but they were all sold. Few pairs were left having size of US 11 and above (observed this is at Shoppers Stop and Red Tape show room).

But as a sneaker enthusiast, I can tell that RedTape collection and portfolio is soo damm good.

2 Likes

Anyone have idea to sudden jumping 27 to 47, just extension of foreign policy for footwear or anything else

1 Like

Hi Hakim, could you share more on the extension of foreign policy for footwear? The last news I heard is from the Budget presentation of Feb’20 on the hike in excise duty on imported footwear from 25% to 35%. Is there a more recent news?

1 Like

No just they extended foreign policy which helps footwear sector for one more year, but i recently seen netin gadkari interview with Quint he talked about footwear sector he mate with them & offer them land near new golden corridor , i don’t exactly remember but you can see one time that interview, i think mirza is new hero in footwear sector because they have very good range of products, i personally check there store, but they not taking good step for Brand building,

Little invested . May be biased

March 22, 2021. ICRA. Rating reaffirmed.

-

Reduction in leverage to ~Rs. 258.0 crore as on January 31, 2021 from Rs. 388.8 crore as on March 31, 2020 due to the improved cash flow arising from the release of working capital particularly in Q3 FY2021, which coupled with unutilised working capital lines, led to healthy liquidity buffer available with the company.

-

With rapid expansion in the domestic market, the share of domestic sales has risen to 65% in 9M FY2021 compared with 58% in FY020

-

MIL is gradually reducing the share of the wholesale/ multi-brand outlet (MBO) segment owing to the high working capital-intensive nature of the segment. The same, coupled with rise in focus on online and exclusive business outlets (EBOs) led to rise in the cumulative sales contribution of these two segments over the last three years. The company has also strengthened its domestic retail network via own stores as well the franchisee stores, with 273 EBOs, increased from 222 as of March 2020.

-

The ratings are further strengthened by the large and diversified customer base in the export market, with repeat orders from reputed clients such as Steve Madden and Marks & Spencer, etc, reflecting positively on its track record. MIL has a customer base of more than 150 clients, including reputed clients such as Etablissements Cleon, Steve Madden, Marks & Spencer.

-

MIL has a policy of 100% hedging of export receivables since FY2011, which insulates it from adverse movements in foreign exchange. Since FY2021, the company has started 100% hedging of imports as well, vis-àvis 50% earlier, which reduces the forex exposure for the client.

-

The ratings remain constrained by the continued tepid demand in the export market exacerbated by the lockdowns imposed in MIL’s main market, United Kingdom (UK), to contain the spread of the pandemic including the new UK variant of Covid-19 virus.

-

The ratings also factor in the low capacity utilisation of the tanneries due to muted demand for finished leather, leading to continued losses in leather segment since FY2019.

-

MIL plans to construct a corporate office, and has a fresh sanctioned loan for the same.

-

discontinuation of the Merchandise Exports from India Scheme (MEIS), under which MIL claimed Rs. 21.39 crore in FY2020. MEIS is to be replaced with Remission of Duties or Taxes on Export Products (RoDTEP). The rates and certain key points for RoDTEP are yet to be finalised, and the same would remain a monitorable. The profitability may be impacted in case of adverse changes in rates under the scheme.

Regards

Harshit Goel

8 Likes

Looking at the last few Q and new showroom Opened, mostly in north part of India and considering from Jan to March all were open, No lock down. Plus lower Intrest cost and they reduced the debt. Results coule be better then excepted.

Fingure crossed.

Dis: Invested

1 Like

But they closed store from Gujrat…and mirzas tenarey business not doing good, i think now they focus only Brand, this year they lonch kid products

Yes! If you notice earlier there products use to sell in Brand Factories and other outlets which was concerning the cash flow due to payment delay.।।।

Now they are opening own store mostly on North India as it is so cold there. Leather products can clicked there. In addition PLI schems for Leather sector is alredy in Pipe line as announced by Piyush Goel. It will get soon. Keep an eye on this Gem!

Risk : Only Management but they are improving.

Best : Products and plans or Management.

2 Likes

If you see the charts patters today with a good delivery size, I feel some thing big is cooking in this Q.

Last June 2020 they have reported around 7 CRS of profit and in last Q nearly 20 CRS, If any thing around 12/18 CRS profit they report then stock can perform good. Key triggers will be lower interest as they are trying to reduce the debt.

- Spoken to Company secretary Priyanka Pahuja, Requested her to have a Con call as they use to have earlier after results. Been advised it will be taken care. Hope there is some actions on this too.

3 Likes

Ju

Shopping at Redtape, was trying to check How the thinks are. Kids were, Formal wear, Jeans T shirt, Shorts. All new style shoes Air.

Impressed with the service here in Hyderabad, Tolochiki and heard new branch opened at Madinaguda Hyd.

If management try or put effort or changes policies which we can See opened 270+ stores till now. Many more to go.

70+ were opened after unlock. A clear sales figure can go UP! Hoping profit around 15/20 CRS this Q on Tuesday for March 21.

Can See more good numbers for June.

Risk : Management

I can be Incorrect but Invested.

RESULTS FOR MARCH 31 2021

-

Revenue increased from 248 to 312 CRS

-

Finance cost reduced to 7 crs from 12 crs

-

Profit after tax is 8.89 crs from 7 crs Over all good numbers , Why I am considering the results are very strong and good , looks like management is focusing on debts and changes in business module.

Borrowings reduce from 252 crs to 116 crs, this is a very big number and very impressive, as said above earlier interest cost is saved and added to the current profits, It will still improve in June Quarter.

-

Domestic & Export under brand • Redtape,: & Bonstreet increased sales from 88 crs t 112 crs.

-

Leather business has improved and cut the losses -68 crs to 38 crs.

Over all this is satisfyingly results , we can see more improvement and sales from newly opened franchises will add up to the balance sheet and reduce interest cost will still make it big.

MIRZA INTERNATIONS Q42021.pdf (5.1 MB)

10 Likes

@ayushmit bhai… Could you please share your thoughts on the results given considerable reduction in debt by 60 % and trade receivables down by half. Though profits not showing much improvements when compared to revenue growth. Thanks in advance.

2 Likes

Hi, I do like some of the things they have been doing but I used to be really concerned about their balance sheet given the high working capital capital and debt. Good that there is some improvement on this front.

Given that Covid has hit this segment very hard one should probably spend time on their annual report to see finer details.

Ayush

Disc: Had sold out earlier by booking losses.

9 Likes

Stock corrected due to results and it will Rise when Annual report is release. Because every one will find in depth details progress about the Company in details like Debt reduce, Intrest cost saved, Trade receivable are down. Improvment in leather Business, Foreign trade improved.

Company Management focusing on Balance sheet.

Called the Company many time, Given proper updates as well. Requested Company Secratery for Con call after results Let See if they take.

Can be a swing in the Business.

Invested:

2 Likes