Do Nike and Adidas offer discounts? And aren’t the people who purchase them different from who buy Mirza?

Thanks Siyaram. Good to know. I am keen to visit a redtape store.

I personally see Redtape as a low cost alternative to Skechers (most of their sport shoes are Skechers based models).

But that’s where I see trouble. I wouldn’t be willing to buy Redtape if the price gap with Skechers reduces.

Hopefully as brand becomes stronger, this will change.

2 Likes

Yes, you are right, Red Tape customers are different from the big players.

1 Like

Hello I am also from Hyderabad.where exactly is store of Mirza Intl? I want to visit

R D Kaushik, the Chief General Manager of Mirza International Limited, claims it is the domestic waste going directly into the Ganga that is much more harmful. “We have spent a great deal on creating an infrastructure to treat all our effluents.”

1 Like

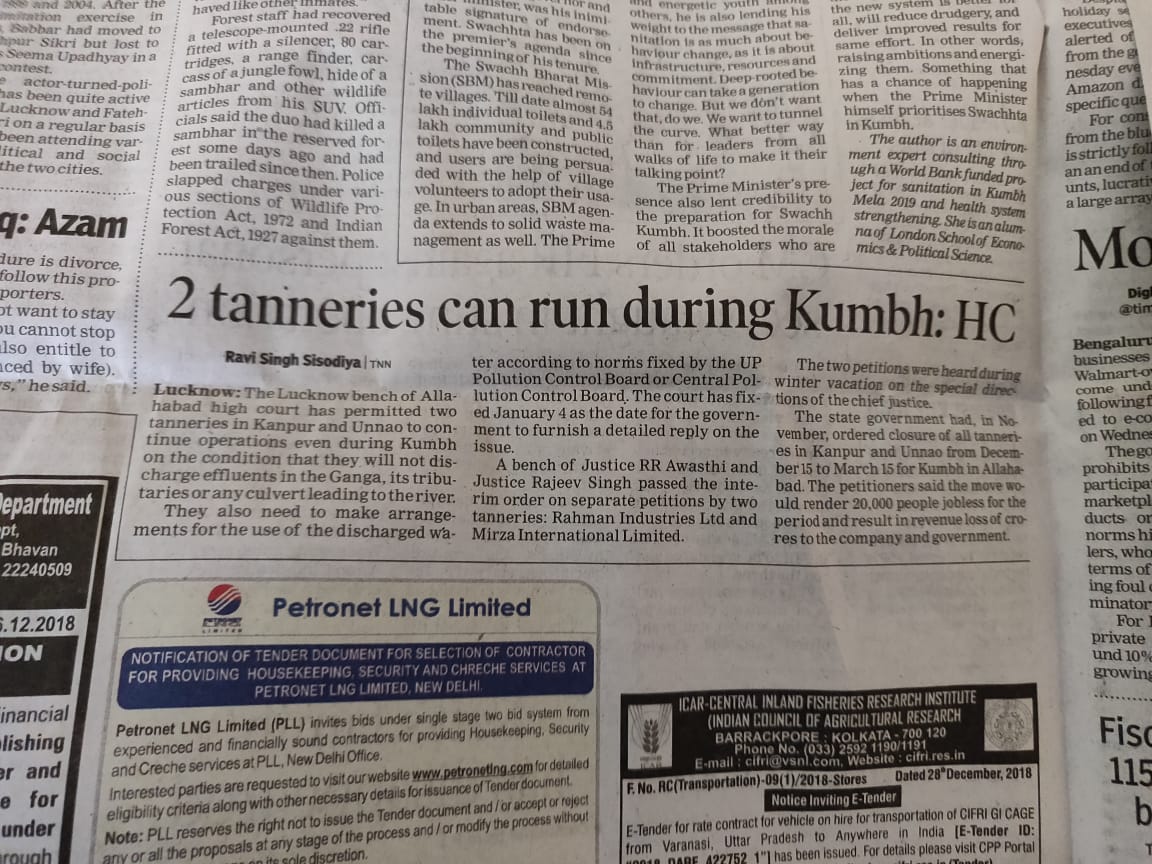

In December, following petitions by Rahman Industries Limited and Mirza International Limited, the Allahabad High Court permitted two of their tanneries to operate, on the condition that they ensured that their effluents did not go into the Ganga.

Do refer to the newspaper article posted by @ayushmit, where this is already discussed.

FY19 Q3 results:

Branded business growing more than 40% yoy.

However, very disappointed by decreased margins and profitability!

2 Likes

Well I think Mirza International result is a mixed bag of performance. Sales up significantly. Gross Margin down by 5% but from Assets deployed in Brand Business it seems they have finally reined in on inventory. The revenue break up shows Export business is down but Domestic and Branded business is up … Domestic and Brand Business asset didn’t go up much from Q2 19 (From Rs. 460 cr to Rs 480 cr) … To me it’s a major positive as Mirza must have cleared some of old inventories at a lower margin… Taking risk in P&L is always better than taking risk in Balance Sheet in my view.

Anyway, the business may evolve over time…Increase in sales is good sign but profitability improvement is key without spoiling balance sheet … Not an easy job!!

22 Likes

Overall nos look poor and concerning. On the positive, the growth in domestic sales is remarkable. The company has been able to grow the branded business at a very high rate over last few years. Had it been an unlisted company, it would have got lot of attention and perhaps valuation of 2-3 times the sales by PE funds just to gain presence, customer penetration and visibility. But unfortunately its a listed company and market may not like hit on margins along with growing balance sheet. It will be a question as to what are the sustainable numbers…are the margins of this qtr temporary or not? In this quarter the company would also have been affected by shut-downs due to kumbh (as per several articles, the industry has been in a bad shape).

17 Likes

Apart from the results, the drastic change in the management’s risk perception is very concerning. The company already has a medium amount of Financial Leverage (As of September 2018, ~50%). By investing aggressively in their Retail operations, they are clearly increasing their Operating Leverage too (Stark increase in Fixed Assets and Working Capital). Combine both of these with the fact that they’re risking the Margins too, and you’ve got a recipe for disaster.

The Share price is comforting, but at what cost? I am forced to remind myself of this wonderful quote from Benjamin Franklin: “The bitterness of low quality remains long after the sweetness of low price is forgotten.”

We live in uncertain times as far as the Capital Market is concerned. Mirza’s antics are really just obscuring the picture more.

Disc: Mirza International ~3% of my PF. I may not add further or may be even be willing to sell.

21 Likes

Has anyone got a chance to update Mirza Conf. call? Appreciate if one can publish the notes and it would be really helpful.

1 Like

I think this is available on stockadda. One needs to login to listen.

1 Like

Below is Conf Call notes I took.

Margin :

- Heavy discount in few items to get rid of excess inventory

- Exports soft

- Tannery was shut down

- Margin pressure in Q4 expected.

- FY20 16% EBITDA margin expected. Q1 FY20 margins shall be good.

- Change in Guarantee commission would be discussed with promoters

Inventory:

- To go down in 3-4 months

- To bring down to 400 Cr by May 2019

- Current 462 Cr 52-53% domestic inventory rest Tannery

- 25% of domestic Garment inventory

- Bondstreet inventory 10-15%

- Larger projection of number of shops were assumed hence higher inventory ordered, but few shops were couldn’t open due to issues.

Balance Sheet :

- Gross current Debt 375 Cr, 35 Cr additional debt expected.

- CFO 83 Cr Capital exp 55 Cr (35 Cr domestic).

- No FCF expected due to capital investments.

Revenue:

- 600 Cr in domestic sales by this year.

- Pressure in 4th quarter

- New stores to use existing inventory

- Exports down by 6% in 9 months. Visibility for 3-4 months.

- 5% decline in exports for full year.

- Lot more shops in pipeline

- 194 stores now.5 more under construction. Targeting pan India including North East.

- Greater NOIDA facility in the making

- Exports impacted due to Tannery closure.

- Retail 170 Cr revenue, with XX% growth. Wholesale contracted.

Business Strategy:

- Advertising Planned next year

- Bond street distribution closed as company has experience in Retail through stores.

- First shop was opened 10 years back.

- Red tape is 50-60% of Mirza revenue. Real Growth has happened in last 3 years.

- Core Strength: Online and Own Stores.

- Next CRISIL Rating review in April 2019

14 Likes

Thanks Prakat for the notes.

1 Like

What I read between the lines in the conference call -

- Shuja agrees that targeting a high level of growth has led to inefficiency on inventory management, receivables management which has hit the working capital needs pretty hard. This was a trade off that they signed up for, what they could not envisage was that their store opening plan will run into tough times which affected their ability to sell. So the double whammy of higher working capital and lower margins has hit the company in Q2-Q3 since they are now forced to clean up inventory by selling at discounted prices. This is likely to continue into Q4 as well.

From an investor point of view what we see is - higher inventory, higher debt and now the inventory is selling for a much lower spread on the cost.

- Going forward they are having two channels - online sales and company stores. Sales through these two channels will have to do the heavy lifting since distribution led sales is not something that they are able to manage well.

Translation - Selling to ecommerce players is much easier than selling it through a basket of distributors and retailers. B2B sales does not call for too much day to day management since terms can be standardized and driven from the corporate office, inventory & logistics management gets streamlined as well.

- Growth targets going forward are likely to be in the range of 25% rather than target aggressive 40%+ rates. Logically it should be much easier to run a tight shop at hygienic level of growth, this way growth can be value accretive.

Investor tone was very tense and more confrontational this conf call, some of the inputs being -

Please put up a press release along with the results where you have a detailed presentation that answers all factual questions in black and white rather than giving estimates & guesstimates on the conf calls

Growth is not as simple as opening new stores and pushing products. India is a dog eat dog hyper competitive market where growth can be done in a value dilutive way. If Mirza wants to build a good brand over the medium term and create value for shareholders, it needs to be a more well rounded and nuanced approach rather than the promoter family running everything by themselves - they need to get in professional folks who have seen the journey before and can guide the family on certain things.

Corporate Governance and the answers on that front hardly inspire confidence. If the management does not address concerns there is a risk that investors will just walk away from this story.

Red Tape is a well known brand and growing 15-20% without diluting return ratios should very much be possible if the management gets its act together. Drop some product if needed, rationalize SKU’s and figure out how to grow in a value accretive manner.

19 Likes

I have been monitoring this company since last year or so. This is a company that really needs proper management at the helm. In Q2 conf call, I remember them being asked about the performance of the new stores. Their answer was ‘We will see how it goes for 6 to 12 months. If they dont perform then we will shut the branch and look to move elsewhere’…To me that was alarming , showed be a naive management who desperately needs professional folks at the top. But its no surprise to me that the things are on a downward slide. Considering the footwear/leather industry on a clear upswing in past 12-18 months, Mirza is going the opposite way. They are weakening their brand they created by ridiculous discounts in Ecommerce platforms.

2 Likes

After going through the numbers & revisiting some of my initial hypothesis, here is my take -

There are some businesses and segments where even the best management struggles to deliver 10% growth. Footwear industry is obviously not one of them, in an economy like India growing a reasonably well known brand at 15% should not be that big a deal. Obviously the company is in a growing industry where both volume growth and realization growth are doable over the medium term - it does not need a great management team to be able to execute and do a decent job.

Discounting is not unique to Mirza, even top brands like Nike, Adidas give 40%+ discounts on ecommerce platforms. Instead of routing business through a distribution + retailer model where anyway margins of 35% have to be paid, one can sell at a similar discount on ecommerce sites (from MRP) and keep the broad realization range to the manufacturer intact. I have spoken to multiple category managers working for these ecommerce companies and this is indeed the name of the game. I am not worried about discounts online, the only thing that does is to take share away from the old time distributors but that does not worry me as an investor in Mirza. In fact higher the online sales I know the sales are genuine! It is much easier to do channel stocking by end of the Q under the distribution model and beef up revenue. In online sales model through the ecommerce players we at least know that the product is selling to genuine buyers.

Where Mirza is running a risky pivot is that they are transitioning from a B2B heavy model to a B2C heavy model while taking the risk of opening own stores simultaneously, probably too much too soon. In B2B business you are an order taker, the customer (who in turn sells to end consumers) tells you what models to make and takes the balance sheet risk off your hands the moment you deliver the goods. In a B2C model, design & inventory planning are on you - the risk of keeping too many/too few SKU’s will impact both your P&L and balance sheet either way.

My base case scenario was that debt will be way higher by end of 2019 and that profits for 2019 will be lower than that of 2018 since finance cost and depreciation will spike. So the results are not very surprising to me though the sharp fall in gross margins in Q3 is - however this can end up being a one off thing if the management learns their lessons and targets a healthy 20-25% growth rather than an aggressive 40% growth in the domestic business. Whether they do that or not needs to be seen.

What we are seeing right now is three factors hitting the financials at once -

- Lower volumes and sales in their export business

- Closure of tannery operations due to Kumbh (leather segment has shown -10% EBIT which during normal scenario shows 10% EBIT. This by itself is responsible for PAT being lower by approx 4 Cr each for Q2 and Q3)

- Double whammy of higher inventory and lower gross margins on the unsold stock for Q2 and Q3

(1) above will get better over time, exports for 2019 are 8% lower than 2018 as of now, the thing about exports business getting back on track is that their receivables and inventory numbers will look better at the overall level - whenever that happens though export margins are a good 3-4% lower than domestic margins during normal times

(2) is clearly a seasonal thing which will normalize soon

(3) having seen the impact of going too fast on expansion and stocking up inventory, if management calibrates and decides that they want to grow business at a lower pace but in a way where balance sheet is in check the current situation should not be too much of a problem.

Mirza is not into getting repeat business from the very same set of customers, so one time discounting does not affect the brand too much. Instead if they were into an annuity business and then do aggressive discounts then the pricing is toast going forward as well since institutional customers will squeeze you once they see there is possible slack in pricing. A one time deep discount does not erode the brand value of something that has been in existence for more than 15 years. Persistent deep discounting (which is way lower than industry standards like what a Koutons did with their buy 1 get 4 free campaign) can and will affect the brand but it is too soon to come to that conclusion now.

While the management is not exactly top quality, I have some respect for the way they have demonstrated the ability to do industry leading growth. On the latest conf call they have admitted that their judgement on the inventory and some other moves has been unsatisfactory, Shuja mentioned “learning curve” at least 5 times on the call. Let us see if they show the ability to learn from their mistakes and calibrate accordingly. If the domestic business can grow at 25% without impacting balance sheet too negatively this business can be in a different orbit in 3 years time

For the time being this is a hold for me since inventory risk is something I expected. Two bad Q’s don’t really break a story for me though persistent lapses in judgement eventually will.

If not for the current market conditions stock might have been 25-30% lower, I do not want to make the mistake of the stock price influencing my thinking too much.

Wait and watch for me as of now.

Disclosure: I am a SEBI registered Investment adviser and this is a minor position for me. I may add more in the future based on market conditions and business performance

27 Likes