Going through the documents related to Anupam Verma Committee on banning pesticides, I could find a match for Butachlor and Triazophos which are being reviewed for banning and are also being produced by Meghmani. However, I couldn’t find much info on the contribution of these pesticides to Meghmani’s topline.

So it looks like there will be upward pressure on export prices of pesticide products.

Unlike air pollutants( which might have less severe environmental impacts during summer months, & hence restrictions on these pollutants might get relaxed) water pollutants like pesticides might be restricted throughout the year ? Can we make this assumption ?

Also, can someone quantify the expected upside on Meghmani’s realizations ?

Revenue up 26% yoy to 452 Cr. Strong revenue growth across all 3 segments year on year.

PAT up 133% to 63 Cr. Major contribution came from base chemicals segment. Profitability decreased in pigment and agrochemicals segments. For agrochemicals, it may be the case that Q3 is a slow quarter.

Finance cost at 9.90 Cr compared 10.1 Cr last quarter and 12.75 Cr last year same quarter.

Acording to Phillip Capital, Meghmani has posted the strongest quarter and the growth momentum should continue. They have summarized the Q3 performance as below:

Sales (+28% y-o-y) were 9% ahead of the estimates, led by +43%/+37%/+22% y-o-y jump in Agrochemicals/basic chemicals/Pigments business (better than expected across all three segments).

EBITDA margin improved to 26.0% primarily driven by sequential expansion in basic chemical segment (helped by strong pricing in caustic soda) and improved operating performance. EBITDA was +33% vs. estimates.

In line with strong sales and operating performance, PAT (Rs 435mn, +118% yoy) was 33% ahead of the estimates.

Caustic soda sales saw 37% yoy growth and EBITDA margin improved significantly to 46%. Agrochemical sales saw robust 43% yoy jump and EBITDA margin remained healthy at 19%. Pigments sales saw healthy growth at +22% yoy with 14% EBITDA margin.

Expects its chloromethane (CMS) project (with capex of Rs 1.4bn) to be commissioned by Q4FY19 (delayed by a quarter). MEGH expects 20‐22% operating margin from this project against negative impact of chlorine currently. Hydrogen peroxide project (Rs 1bn), caustic soda expansion and captive power plant (Rs 3bn) – are well on track and will add to value growth from FY20

Upgrades target to Rs. 135 from Rs. 100.

It was an all round performance by Meghmani, with Management targeting Rs. 1800 cr. topline in FY18 and a contribution of Rs 1000 cr. from each of the three segments in next 3-4 years taking the topline to Rs. 3000 cr.+ (which is 20%+ y-o-y growth). The young generation of Soparkars/Patels are already building aggressive vision documents for the Company which ensures smooth succession planning, longevity and continued growth of the business.

Why aren’t we seeing upward revision in P/E despite good Q3 results? I don’t understand this. It is still languishing in between PE multiple of 14 to 17. Can somebody please help me understand.

I think market is perceiving that caustic soda prices have topped. That was the major concern of most of the investors on con-call. That’s why share prices have not done anything for last 3-4 months.

Thanks. Can anyone help me understand how Caustic soda and crude oil or any other raw material influence their raw material price or profit margin?

I want to learn about how this business is run and what factor influences its revenue or profit?

Reported good numbers in Dec '17 quarter; traditionally co’s weakest quarter (Q3 FY) - some seasonal aspect.

Q3FY18 Concall Highlights (Source: Capital Market) -

Net sales was up 41% at Rs 443.1 crore driven by strong exports growth of 45% contributing 56% to net sales and domestic growth of 35%. EBITDA up 93% as raw material cost as percentage of Net Sales declined from 54.7% to 52.0% while other costs as a percentage of Net Sales declined from 22.9% to 18.5%. Interest outflow was down 22% to Rs 9.9 crore compared to Rs 12.8 crore in Q3FY17 with reduced debt. PAT increased 118% to Rs 43.5 crore.

Exports grew 45% driven by robust growth across Pigments (up 52%), Agrochemicals (64%) and Basic Chemicals (49%)

Domestic business grew by 35% led by strong growth in Agrochemicals and Basic Chemicals, marginally offset by lower net sales in pigments

Pigments

Pigment net sales were up 33% YoY at Rs 148.8 crore, driven by robust growth of 52% in exports. Exports share was at 85%. Net sales declined in domestic market due to increased focus on higher margin exports. Total sales volume was up 23% YoY to 4030 tonne with higher blended realization.

EBITDA increased 6% YoY to Rs 20.6 crore led by higher net sales while EBITDA Margin declined marginally to 14% from 17% in Q3FY17.

Capacity utilization increased to 75% compared to 70% in Q3FY17 while production was up 10% YoY to 6004 tonne

Sees stable demand, better utilizations, and improving operating efficiency in pigment segment and expects to improve EBITDA margin at 16\17% in FY19.

Agrochemicals

Agrochemical net sales increased by 54% YoY to Rs 151.4 crore led by robust growth in domestic and exports market, up 32% and 64%, respectively. Exports market contributed 69% to net sales compared to 64% in Q3FY17. Sales volume was up 18% to 4246 tonne coupled with strong growth in blended realizations on account of increased sale of higher margin products.

EBITDA increased 456% to Rs 28.2 crore on account of higher realization on products. EBITDA Margin up at 19% as compared to 5% in Q3 FY17.

Capacity utilization was at 58% while Production increased marginally to 3891 tonne

The company expects agrochemical margin at 17\19% in FY19 supported by visible sustained export demand.

Basic chemicals

Basic chemical net sales was up 55% YoY at Rs 151.4 crore driven by strong growth in blended realizations coupled with higher sales volume. EBITDA was up 94% YoY to reach Rs 68.4 crore. EBITDA Margin was 45%. Capacity utilisation was at 83%.

Caustic soda sales saw 37% YoY growth and EBITDA margin improved significantly to 46%, mainly led by increased caustic soda prices.

Caustic potash plant ramped up to a higher level of 70% and contributed Rs 23 crore (vs. Rs 47 crore in H1FY18) to sales. The company expects optimal utilisation in FY19

Chloromethane plant of 40,000 MTPA is progressing as per plan and is expected to be commissioned by December 2018

The company sees healthier margins for its chemical business at around 40\41% in Q4FY18 and expect 37\39% margin in FY19.

Expansion

Meghmani Organics has greenfield expansion project under environmental clearance (details to announce soon) and indicates this project will be backward integrated.

The company expects its chloromethane (CMS) project (with capex of Rs 140 crore) to be commissioned by Q4FY19 (delayed by a quarter). It expects 20\22% operating margin from this project against negative impact of chlorine currently

Other projects Hydrogen Peroxide project (Rs 100 crore), caustic soda expansion and captive power plant (Rs 300 crore) are well on track and will add to value growth from FY20.

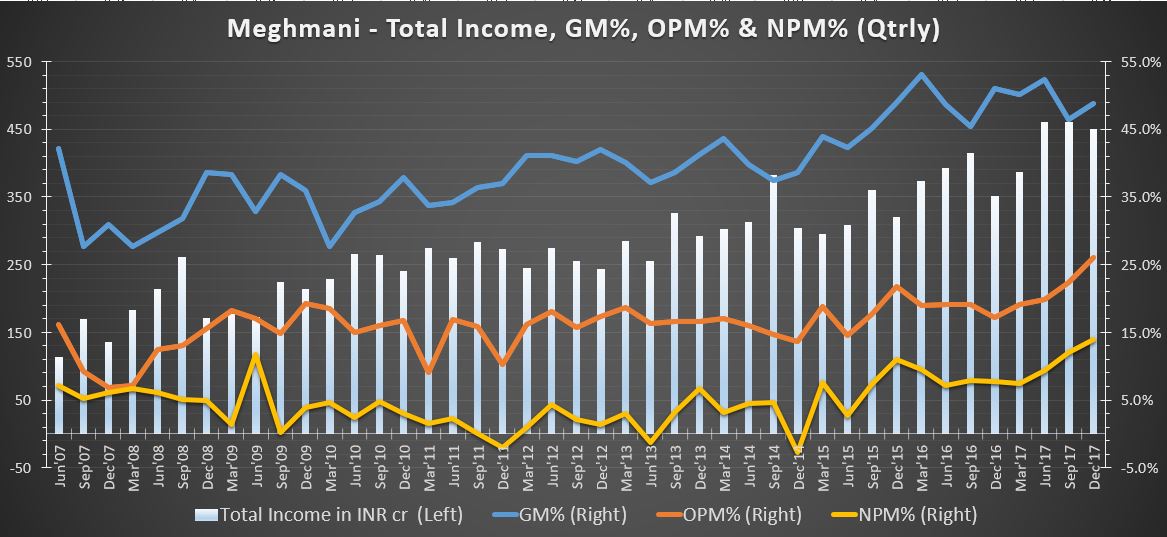

Janme, would have happily shared source info if available online. It is from my tracking spreadsheet. Intend to post (occasionally - so as not to bore) similar graph of other cos in portfolio and/or on tracking radar. Cheers.

It always puzzled me how company like Fineotex chemicals with lower EPS and profitability trades with higher PE multiple (>25) comparative to Meghmani which trades at PE multiple between 14 and 17.

Can somebody help me understand the rationale behind it.

@spatel Could you please provide your valuable feedback as well. Thank you

Yes, rationale is that big guns could not spot meghmani when it was at 39-40 range, it is quiet common that some unknown stock is picked up despite existing bigger & cheaper stock available, due to no retail participating in this small stock, it is being taken for a ride on low volumes & than recommended by some x analyst in TV & game of distribution start.. I have always lost in stocks if you buy listening to TV analyst or someone recommended to buy. Stock market is game of human physiology than maths. I am invested in meghmani & long term outlook is excellent, management pedigree is of high quality. This will go long way. Expecting 600 cr EBIDTA in 2020.

The trailing 12 months net profits on consolidated basis is Rs.189.67 crore. On equity base of Rs. 25.43 crore, this gives us an EPS of Rs.7.46 which translate into PE ratio of 13.68 considering the price of 102.