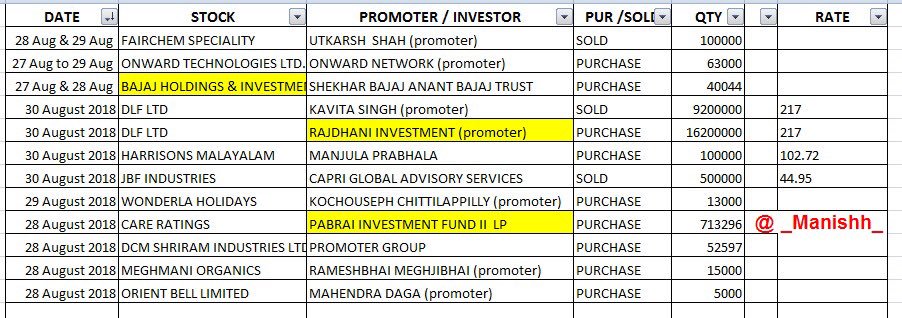

Again today, promoter acquired 15,000 shares from market value Rs.1351549

Yes they are seeing the stock very attractive at such prices. The P/E is just 9-10 when other chemical companies are commanding a P/E of atleast 15-20

@virajkhatavkar - Can you please help me to find out from where did you got this data.

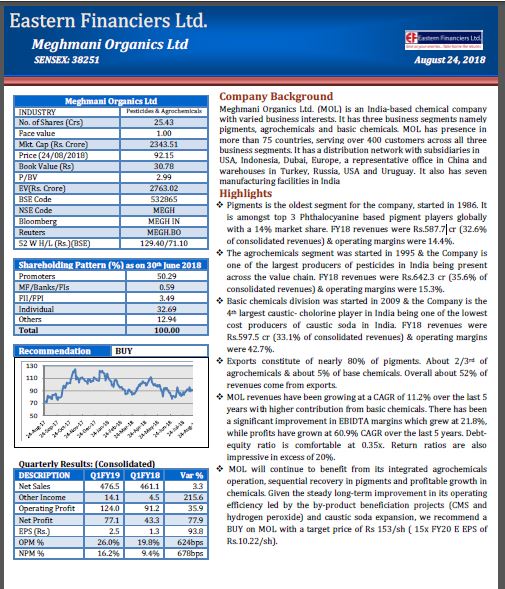

Basic chemicals and agrochemicals are commodities and it is difficult for a company to have pricing power. Even if the company pushes these products through strong distribution network, which is what Meghmani Organics is doing at present, lower realisation could lead to lower profit margins and, eventually, low growth or negative growth in profits. While the current OPM is around 23%, right up to FY14-15, OPM was below 15%.

Growth rate of revenue in June 2018 quarter has already slowed down and capacity utilisation levels are at near peak. It should be interesting to see how commodity prices play out, going forward, which will have direct impact on company’s performance.

On the financial front, performance ratios have improved dramatically in FY17-18; almost every important ratio has improved. Cash conversion cycle has improved gradually in the past few years mainly on account reduced days of outstanding receivables. Timely debt repayment has reduced interest expense and improved interest coverage ratio. Return ratios are at their highest in FY17-18; return on equity is 30% (in FY16-17 it was 17.2%), return on assets is 14% (in FY16-17 it was 7.3%) and return on capital employed is 30% (17.3% in the previous year)

And, yet, the stock is currently trading at price-to-earnings (P/E) multiple of 8.3x. The stock does appear to be cheap in terms of valuation but, given the capacity utilisation almost at its peak, the OPM is at a historic high and with the large expansion plan being implemented, the risks are considerable.

-MONEYLIFE

9 Likes

Actual P/E is 11.2. One needs to see the consolidated “E” after minority interest. A good chunk of “E” goes to promoters directly by way of their 18% holding in Meghmani Finechem which is 82% subsidiary company of Meghmani Organics.

1 Like

Agreed.

But, even for commodity businesses, high utilization coupled with strong demand translates into bumper profits.

I still am of the view that Meghmani is poised to grow more due to the problems in China. There is still chance to make good profits if one stays invested through ups and down for 12-15 months. The stock is hovering around at the same price for almost 8 months now. I am waiting for the rally which is bound to come sooner or later but not more than Mar 2018. The rally is probably going to re-rate Meghmani and mostly take it around 150 where it will stabilise and have some resistance.

Jun 2019 is my lakshman rekha. If the stock doesn’t move I would probably move my capital somewhere else. But I am going to hold what I have until Jun 19 and maybe add a bit if the stock goes below 85.

Management is positive on it’s view that they will achieve the 3000 crore target in revenue by 2021. For Meghmani to achieve that target it has to grow it’s sales by 20% on a CAGR basis. It’s market cap will atleast double in that period. And do remember that when I say double I am being conservative in my estimate. Medium case it might even go 2.5-3x and if everything works out well maybe 5x.

3 Likes

Entry Point in a commodity business is the key. Investors who bought last year below 50 are still sitting on decent profits. Here, the issue is the management has given a huge revenue growth forecast, while operating on peak margins. I would prefer to track this stock over the next 2 quarters, rather than getting my capital stuck in an opportunity cost. There are better immediate options within the specialty chemicals sector, such as Kiri Industries.

2 Likes

Most of your answer is lifted from the Moneylife article on Kiri Industries. Hence, I do not wish to further respond with my views. Except, I’d like to state that the management of kiri is far from “dicey”. In fact they are visionaries with the dystar investment. Once fully unlocked the shareholders will realise the value of their shares.

2 Likes

That is not how you cite source @virajkhatavkar . The 2 letters ML looks like an afterthought and is evasive. Please append this way “Source: moneylife.com”. Also a clear demarkation btw the copied information and your personal views will also make things clearer.

Regards.

It’s better that I delete it. I don’t intend to make users of this group seem that I am trying to take the credit for moneylife. I thought people are aware of MoneyLife. I shared it with no harmful intentions.

Thanks - Viraj!

@jitenp Do you have idea about how the current rise in crude prices would affect Meghmani’s business? I am thinking that the simultaneous rise of rupee would offset it or give more forex gains. In the last quarter Meghmani had gained about 13% in other income due to forex gain.

Dear friends and all respected senior members, there is a news of amalgation in MOL in market and many people are saying until or unless NCLT agrees on amalgation…Promoters are trying to keep the price low…Does this is possible by the promoter to keep the share price low intentionally? If this is true then what are Promoters motive behind this? Please guide us …

Or show the path to understand the amalgation issue…

1 Like

The CRISIL report reaffirmed Meghamni’s rating and if you read the whole report, it sure gives good analysis/report on overall business and risks associated with Meghmani. I would suggest anyone invested and looking to invest should read this report.

1 Like

It seems that caustic soda prices are going to be high this year as well which is a good news for Meghmani.

Couple of observations

- Capex of Rs.1000 crs to Rs.1200cr planned for FY19 and FY20 as per CRISL rating report. Majority of them in Caustic soda capacity building where demand is high and EBITDA margins are 42% for FY18.

- Basic chemicals division contributes 33% of total revenue

- Fourth largest caustic-chlorine manufacturer in India

meghmani q2 results:

1 Like

Whats your view on the results ? Not actively tracking, b ut looking as it came on my screener.

Results looked good at a broader level. Why then market seems so despondent about this company?

1 Like

Revenue declined for basic chemicals, which is supposed to be the key growth area… that seems to be the concern!