Any Updates after recent earnings, investor presentation and concall.

In concall management said they had bought new land parcel in greater Noida for future growth.

Any Updates after recent earnings, investor presentation and concall.

In concall management said they had bought new land parcel in greater Noida for future growth.

The Company’s business update for the fourth quarter and full year ended March 31, 2022, based on a limited review by the Management Team is as follows:

Annual report for FY 2022

D: Invested with a small tracking quantity at 350cr market cap. Company is foraying into a new area which is in nascent stages in India. Trusting the promoter pedigree & their past track record & hope they can make wonders here.

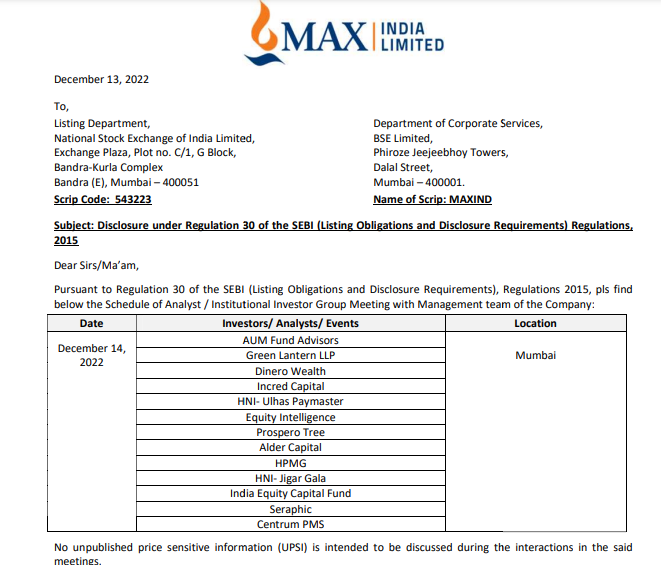

Latest Investor meet intimation, Quite interesting to see the HNI & fund managers list.

Update - It seems Porinju sir from Equity intelligence bought 2.5 lakh shares yesterday.

Max India will take its time to turn profitable, may be few quarters/ years, but good to see investors trying to join the party a bit early (hope so it won’t inflate the prices until I finish my desired buying quantity at lower prices ![]() )

)

D: Invested, Transactions in last 30 days.

Company today reported a major fire accident at their care home facility, in which 2 casualities. Disappoting start to new year.

Excerpt from Q3 FY23 Investor slide deck:

1)Residences for Seniors:

Antara Dehradun: 1st Community, 96% of units sold as of Dec’22 end, repaid all debt, continues to be cash and PBT positive.

Focus on sales closure of remaining units.

Antara Noida Phase 1: 2nd Community, 98% of units sold.

Antara Noida (Under Construction): Targeting to achieve planned IRRs inspite of cost headwinds through robust sales velocity, price increase and timely delivery. Total 550 units.

Noida Phase II: Application for revised building plans submitted with Noida. Planning to get RERA application post approval.

Gurugram (with MEL): DM Fee model aligned for the project along Dwarka Expressway, Massing of the project has been finalised. Work in Progress for revised costing based on final massing.

Bengaluru: Two potential partnerships identified at Bengaluru. We have engaged IPC for scouting more opportunities at Bangalore.

Pune: Draft term sheet shared with two landowners at Pune. Working on the financial model and will share the proposal.

2) Care Homes/ Memory Care Home

3) Care at Home

4) Med care:

Balance Sheet: Strong BS position with Net worth of Rs 540 Cr

Consolidated Revenue at Rs 153 Cr in 9MFY23, Up 6%^ y-o-y (Q3 Up 8% y-o-y)

Consolidated EBITDA at Rs 6.5 Cr in 9MFY23, Up 7x y-o-y

Business is still in the investment phase. Seems like promoters are very transparent in their actions/ filings/ investor friendly & ready to accept their mistakes. I think they are trying to establish & prove a proof of concept/model for most of the segments. They are very conservative & trying not to burn more cash & trying to slowly scaling up. As said in previous concalls, once they have a proof of concept in place, they can easily scale up by raising funds.

Break even or profitability may take few more quarters. Key thing is to focus on how management walk their talk & their execution capabilities.

Please feel free to add if I have missed anything.

Requesting fellow members to share their valuable thoughts if anyone is tracking.

D: Invested, Biased. Transaction in last 30 days.

Investor Presentation Link:

Hi InvesterUK,

I am also tracking Max India. Can you elaborate the rationale behind your purchase. How about the competition. Any builder with deep pocket, can start this business by making collaboration with some doctors/hospitals. What is the moat? What is the market potential?

Hi sureshwaran1,

Senior care is an emerging sector in India, many believe it will be a upcoming mega-trend and I think Max India is the only listed player in this space. Almost debt free, Strong BS position with net worth of Rs 540 Cr, current Mcap ~ 400cr. Recent capital reduction scheme was at 85rs per share.

Senior care market is still at a nascent stage India. As per a 2019 report by McKinsey ,17% of the seniors in India are living alone. This number will increase drastically in future going forward due to increase in the number of nuclear families, improving life expectancy, Migration of younger generation to foreign countries. I currently live in the UK & there are many well established care homes here having good profitability, trading at 5x sales.

The demand for senior living space is pegged at about 240,000 units, is almost 12 times the available capacity. As per available statistics, percentage of senior citizens in India to total population is about 8% which is expected to increase to 20% by 2050. Considering the huge population of India, changing life style and change in society view about Care homes, better disposable income in the hands of citizens, possible government aid for senior care can create big opportunities in this sector.

Max group has a history of spotting early trends like how they started Max life insurance, Max healthcare in 2003 (A time when no one was much aware of insurance & private speciality hospitals). In 2020 they demerged Max Healthcare & it listed at 10k crore Mcap & now at around 40k Mcap. They have a history of creating shareholder wealth by scaling via foreign private investors & JV. Honest promoter group with good corporate governance standards & transparency.

IMHO, I don’t think every bizz needs to be heavily moated to create wealth. Max India has an early bird advantage here as they started off in 2012 & they have learned their lessons from asset heavy Dehradoon project & they have turned asset light now. So I feel they are not a real estate play anymore.

Compared to any “builder with deep pocket” Max has some unique competitive advantages in patient care, Existing tie ups with many hospitals/doctors, Brand building, having scale up partners from their previous experience in setting up Max healthcare, Please check AR about the profile of their MD & other team members.

In case of senior care / Hospitality sector, it is all about creating a new segment, earning trust from customers than a pure play real estate.

Though above are few positive triggers, I am closely watching their execution & bizz scale up in the next few quarters/years.

I am in a wait & watch mode for now, Let us see how this pans out. Giving a larger time frame on this investment as it may take time for the bizz to scale up & turn profitable. Cheers

A quick look tells me that their net worth / book value is falling at about 10% yoy since the start. While the balance sheet can still be strong to support their leg of growth for next few years, it is still a risk until they start to change this trend.

Disc: Not invested. Watching the development.

After analysing the historically available data about Max group of companies & by referring to some of the previous posts in this thread, I think below is the typical playbook followed by them in setting up any new business ventures;

#1. Venture in to a new sector with huge growth potential (Life Insurance, Healthcare, Health Insurance etc in the past).

#2. Capture a small portion of the overall market share (larger pie) and also have an early bird advantage.

#3. Establish a proof of concept by experimenting on pilot basis and by using an asset light model.

#4. Correct their mistakes & further optimize the proof of concept to achieve scale up & profitability.

#5. Try to achieve breakeven, Then slowly scale up & turn profitable by burning cash very conservatively (less leverage & debt).

#6. After a profitable model is established, Scale up the Bizz further using private partners/ equity dilution.

#7. Once the bizz reaches a reasonable size or Market cap, Sell to any PE or demerge to create value for shareholders.

I assume currently Max India is now at stages #3 - #5 of the above playbook. My assumption can be wrong also, Feel free to share your valuable thoughts.

I am not sure how many years they will take to move to next stages. Please note that there will be always a investment risk until they reach a reasonable size / profitability in this new Senior care sector.

D: Invested, I am not SEBI registered. Please don’t base your buy or sell decision based on my thought process.

I have a few queries in regards to Senior Living/Aged care facilities (Dehradun and Gurugam) business model.

My understanding is the units are getting sold at outright price to the aged care people (age >55) and Max india would get the income from daily operations(different services) after the owner starts living there. What if the owner chooses not to avail any services from Max India meaning if they decide to live by themselves? or if they don’t need any medical related services?

What if the owner chooses to sell the property to someone else?

How do they ensure Max India gets income from every single unit which we have sold? Is there a possibility that some people may not choose these services so there will be a risk to the MAX India income?

some very interesting points and good that you are from a place where this industry is already mature.

I was checking senior living projects sometime back and with initial glance saw some issues in India as of now -

Thanks

As you rightly pointed out, UK care markets are very matured ones with well established Govt. policies, framework and standards in place. In case of seniors, Care home expenses are funded by either Pensions, Govt. support(NHS), Private insurance, partly funded by self/ their children in some cases. And if you have no money to afford care, Govt will take care of you in their own facilities.

On the contrary, things are very different in India & not comparable with above scenario. I think to make a clear differentiation, Max need to create an “Affordable” ecosystem with holistic care and establish customer trust. Bring in best practises similar to that of any matured markets like Doctor/GP on call, Physiotherapy, Dietary requirement support, Medicines, necessary medical equipment’s, Qualified 24x7 Nurse, Carers etc to take care of day to day well being of seniors with varying challenges like mobility issues, Memory loss etc (I think they have already implemented few of these things into their existing projects).

From Q3 concall;

“For seniors who can’t be maintained at home because of aging-related issues in terms of mobility, medication, administration or monitoring or bathing, or have gone through an intense medical episode need to recuperate for some time, or people who come from outside the city or country who after surgery have to stay for a while, we offer the Care Home facility. This is more popularly called Assisted Living Outside India. And people who have cognitive neuro disorders, dementia, Alzheimer’s, Parkinson’s in early stages, we also offer Memory Care Home option. For those who require the same services in the convenience of their home, we offer through Care at Home, we offer things like critical care, physiotherapy, diagnostics, nurse at home, caregiver at home, pathology about 16 service lines. And if seniors require some products for their comfort and recovery like wheelchairs, hospital beds, air mattresses, respiratory equipment, we also offer it through our MedCare equipment vertical.”

About cost of senior care services & its affordability in India:

Better insurance penetration, higher retirement savings & disposable income, Govt policy support etc can help seniors in easily accessing these type of care facilities. Recently I had an interesting conversation with few friends settled abroad & not planning to return to India at the moment. Parents live in India & have own house, retirement corpus, rental income etc & not willing to move to foreign countries. Most of them said that they were exploring a system similar to assisted care for parents and willing to fund the cost from their pockets (moral obligations?). I assume Max may be focussing on these kind of income groups. In these days, there are many young population from India migrating & settling in foreign countries. These kind of changes in lifestyle & dynamics might bring more visibility to senior care space.

From Max India concalls, They are targeting families above 15L income group which itself explains why their care services are priced at a premium. I agree with your point that most of the other projects now run in India by other groups are “merely normal residential real estate projects with some added features for seniors”.

Reg. the senior living projects like in Doon - From management commentary, I think now they have learned their lessons from these Asset Heavy, low margin, Less revenue growth senior living projects. Management focus is more towards Care Home, Care at Home & Medcare sectors (3 verticals) where quick scale up might be possible in future. Even for the CHs, they are looking for building on lease/ Rent models & trying to remain asset light rather than being a capex heavy one. They also provide support in their CHs for the senior patients getting discharged from hospitals but still needs medical attention for few more days. This also helps the tied up hospitals in having a better bed turnover ratio.

As highlighted before, this sector is in a very nascent stage in India, but looks quite interesting to track & see how this unfolds in next 5 to 10 years. I am bit (over?)confident about the promoter group. I felt they are very honest in their disclosures, concalls & have a good track record of scaling up new businesses in past ++ margin of safety build up at the CMP. [Max Healthcare scale up is a good case study to explore. Present MD of Max India, Mr. Rajit Mehta spearheaded Max Healthcare growth from Inception in 2003].

Somewhere I read that Promoter is like a multiplication factor. No matter how good the sector /Business/ Financial ratios are, if the promoter is a chor then the overall value is zero.

I am from a Systems engineering/OT background & not from Healthcare sector. Just trying to explore & understand the senior care space. Thanks for all the support and collaboration. Cheers!

Sharing few links for reference:

Care home types in the UK:

https://www.carehome.co.uk/advice/types-of-care-home

Few funding news from Senior care space in India:

“I have been closely observing the trends in the emerging elder care space both globally and specifically in India. I believe the elder care space is at the same cusp, what private hospitals were in early 1980," said Pai. (Ranjan Pai, Chairman of Manipal)

Quality of care speaks a lot, snip from Max India con-call.

As per my assessment, Care Homes and Memory Homes is the most exciting Segment for this company. Their only Care Home center which has matured is Gurgaon. Just notice the Contribution margin changed QoQ from 8% to 12% even though utilization remained the same at 58%.

To me, this is a sign of company raising their prices or reducing discounts. They seem to have captured the market and feel confident in raising prices.

Hi Murali. The following interview of Tara Vachani has all the answers that you need regarding property being sold to seniors.