MangoSip is also provided on Rajdhani trains. I myself had it on Delhi-Mumbai route. Also recently I was travelling on a Duronto train on Mumbai-Indore route. I reached station a bit early and I witnessed all the stuff being loaded in the Pantry Car. There were only two Drinks, mostly MangoSip (around 70-75%) and some JumpIn cartons. I was surprised to see JumpIn as I havnt seen it anywhere in last few years, they might be providing very attractive pricing for railways.

I have also seen Manpasand products in hyper markets, Big Bazaar and more often in last one year. Though I think they do not sell that well at least in the cities. But in the Train I do feel MangoSip is a bigger brand. These are all my personal opinions, just thought of pointing out what I observed.

I second that on jumpin… Always get it in Rajdhani trains…

And I thought it was old brand…but looks like they still make it for Railways…

Some of the previous posts are on whether manpasand products are selling or not.I think the share has crashed not because it’s product r not visible but because of certain corporate governance issues leading to resignation of auditors.The exact reasons are still not public.Its similar to kwality it’s products are still selling , but the share price has crashed by almost 75%.I think it would help members if someone could get info on the reasons for resignation and its impact on the company.

I informally spoke to a company contact, he seemed to suggest that they had an issue about releasing the results on a particular date last year and this year also it came up. This time round they refused to budge with the auditors about the release date and turn Deloitte shocked them with the resignation. The new auditors are on the job… but the damage is done… Kwality is completely different… have you seen their debtors! My guess is that if nothing comes out from the new auditors reports as they would have a lot of reputation at stake then slowly and steadily things would get back to normal… Some FIIs have surely sold out but thats precisely the time that you get to buy these stocks at reasonable valuations… Its a debt free company with hard assets on the ground and in market that is immense potential… In ten years time, with new plants coming on line and high free cash generation, it could be into a totally different orbit… What is strange is that all of a sudden people are totally forgetting the big picture…

Management has to come out with clarification officially and then only they can be trusted.

Dear Atul,

Quite interesting market psycology know? We want to ask the convict that he is a murder or not?

Do you think, if we will ask for proof they will give us? Hope they will come out with some clarification!

Results declaration date announced

Results Declared

My take on results …

Results are definitely looking superb on books… But market is doubting which will be cleared only with time…

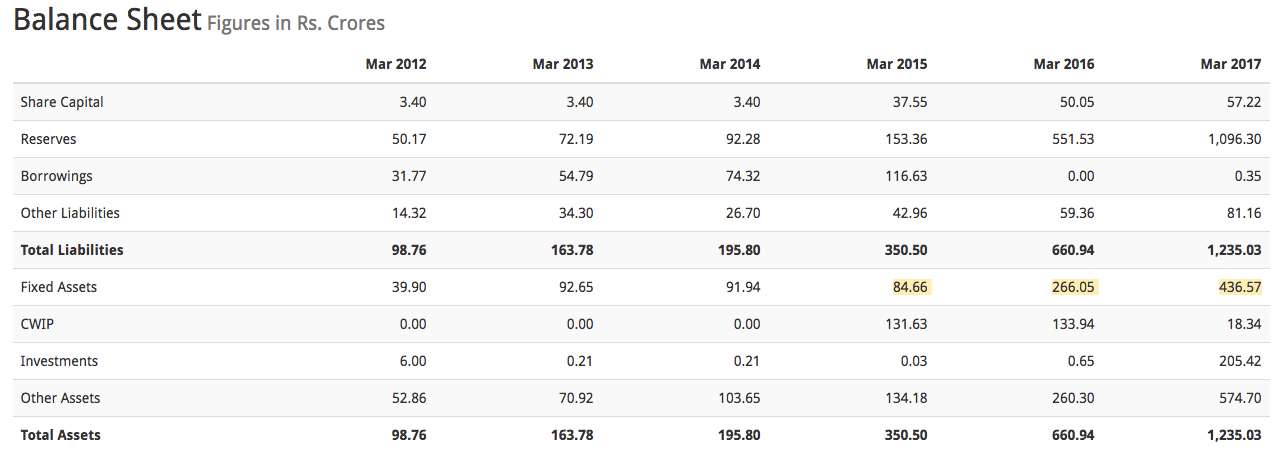

Some observations

High CWIP due to Capex Cycle

High Current Borrowings compared to last year

Investments amount reduced (which are knocking off CWIP)

Important things

Dividend declaration

Recently launched health drink (which can be future of company)

Tie up with Parle for distribution

And expansion going on in Varanasi and one more city

Manpasand anyone? Will this be a time for greed during fear?

It was just the proper agreement was released yesterday but they had been planning this joint distribution since long

I was more interested in knowing whether there are any bravehearts ready to enter Manpasand at this level. What if Deloitte just over reacted considering the new auditors raised nothing of significance so far. This price appears to be a steal for a stock which was quoting at Rs420 a couple of months back.

I also found nothing negative of significance in the results. Good top line and bottom line growth. Increase in receivables in line with increase in sales. Borrowing of Rs100cr considering high investments. D/E is very low even at these levels. ROE/ROCE appears low as there have been an equity raising and not all investments are yet bearing fruit.

Initiated a position @ Rs 140 and may add more if it stabilizes, investment thesis being, as proven by Satyam, ICICI Bank and others, in India every promoter will siphon off money if given the right opportunity. Its in our culture. We try to bribe even Gods through coconuts and bananas.

Corporate governance issues are to stay here for long and we need to find mispricing opportunities (where there is a chance of capital preservation) among them.

Not a Buy/Sell recommendation.

I was also thinking on same lines. But would like to know if thier are more example of companies (other than Satyam) which successfully made a comeback when such corporate governance issues were raised. I burnt my fingers in Tree house , Sudar ind etc where I lost almost all the capital. So wants to be a bit cautious this time.

Please share if you know any other good companies which went to similar fate in past and than rebounded in long term. This instills the confidence.

I too initiated a position a couple of days ago. At current valuations of around Rs. 1700 crores it doesn’t seem to be obscenely priced. I’ve tried their products while travelling in the railways. It definitely could provide tough competition to other products. In my opinion, the Indian consumption story is here to stay. However, what perturbs me is the lack of availability of their products in small stores in Mumbai. If indeed the company is genuine, it has substantial room for growth in business. There may be some corporate governance failures. But, at current levels it’s probably incorporated in the price. Rest, only time will tell.

Not a buy/sell recommendation.

Disclosure: Invested

I have entered the script too. The company is growing profitably and at a great pace. Brand moat is only going to increase with time. There is a gap where major Cola giants are unwilling to serve in cheap juices and therefore, Manpasand has an untapped market that it can exploit. Even in supermarkets, being a low cost supplier, it can easily gain market share with cost conscious consumers. This is a company that buys commodities and sells brands which is always profitable. Let us see how things unfold.

Assuming that manpasand business is valid and genuine - the lack of good return ratios should bother investors. In cos with limited or no operating leverage - low return ratios stay low and so do the valuations. The 5 yr cagr in sales is rouughly equal to the 5 yr cagr in earnings indicating that the co does not currently have a cost structure that is optimized to enable it to do that. I wouldnt be too enthused with manpasand valuations as distribution pacts are typically low margin affairs for the distributor and there is every possibility that margins may drop further - further depressing the already uninspiring ratios. Do exercise caution.

Best

Bheeshma

But if we consider that results are genuine , than current EPS is around 8.74 for this year which comes around 17-18 PE. Isnt it a v cheap bargain for a FMCG kind of stock. If we ignore return ratios and just look it from PE valuation point of view, If not v long term , atleast in next 1-2 year it can fill little valuation gap (assuming their are no flaws in financials).

I saw on bse website, insider trading info., Promoter has bought shares worth 1 crore rs in recentdownfall around 225 rs.

More importantly, the RM price of their main ingredients, sugar and mango pulp, have crashed considerably in recent days which may lead to a margin expansion.

Disclosure : Invested recently, views are definitely biased.

Lot of dilution between FY14 and FY17 and that’s how the balance sheet has grown. The money has gone towards repaying debt and capex. What’s interesting is this Capex. Who is deploying so much capital into a company with such low asset turnover and is still calling itself a FMCG play? I don’t think this is a branded play because I haven’t even heard of their brands and if their moat is railway contracts where a single-brand is supplied due to contracts, is that really a moat? What if the contractor changes their mind or chooses different brands? I am quite suspicious of the QIPs. Do we know who pumped in 500 Cr into the company in FY16 at Rs.700/share?

Last I checked Paper Boat had a valuation of 600 Cr or so. Does Manpasand products have a better brand recall than Paper Boat for a 1600 Cr valuation?

Disc: No interest