This is a double edged sword. Jubilant trebled after the management resigned. Maybe internal problems, maybe good times ahead?

Manappuram Finance Ltd

Highlights of Q4 FY18 and FY18 Results

Q4FY18

- Consolidated revenue from operation 889.8 Cr

- Consolidated PAT 182.18 Cr increase of 5 % QOQ

FY18 - Consolidated Net profit 670 Cr lower by 11 % compare to last year

- Standalone Profit stood at Rs 169.5 Cr for Q4 and for the full year was700.7 Cr

- Company Gold holding was 64 ton up by 2.6 % QOQ and 4.8 % YOY

- Total number of gold customers for the year were 22.5 Lakhs

- Gold Loan book stood at 11735 Cr up 3.6 % QOQ and down 5.5 % YOY

- Auction during the quarter were Rs 89 Cr

- Weighted average auction stood at 1835 Cr which was at 65 % of current gold price

- Interest Accrued was only 2.5 % of the total gold loan AUM

- Loan disbursement during the quarter was 20,488 Cr . Online book accounted for 32 % of the total gold loan book compare to 25 % in previous quarter

- Total AUM grew by 7.6 % to 15765 Cr compare to previous quarter and 15.4 % YOY

- Asirvad Micro finance

o Closing AUM stood at 2437 Cr which is 15.4 % up on QOQ and 35.7 % YOY

o Net profit for the quarter was 13.05 Cr compare to with a marginal 0.36 Cr profit in Q3

o Made provision of 16.95 Cr in Q4 . Company provide 24 % more then the minimum amount require by the RBI

o Disbursement were Rs 954 Cr during the Quarter compare to 688.8 Cr previous quarter . 100 % of disbursement are now done in Non-Cash Manner directly into customer bank A/c

o 15.01 Lakh customers , 832 branches , more then 4168 employee , 19 states , 6th largest MFI in the country with a capital adequacy of 15 %

o Parent company had infused 100 Cr in the subsidiary which will take the capital adequacy to over 20 % - Home loan business

o Total loan book of 374 Cr , up by 9.5 % QOQ , it operate from 35 branches .

o Disbursal stood at 625 Cr up by 25 % QOQ and operate from 73 location

o New business stands at 25 % of the consolidated AUM

o Consolidated finance cost was Rs 268 Cr , average cost of borrowing decrease by 10 basis points to 8.66 % . Average cost was down by 104 basis points YOY - Employee cost increase marginally by 1.8 % to 162 Cr

- Consolidated headcount stood at 24,886

- Administrative cost decline by 5.6 % decline in 133.24 Cr

- Depreciation was 18.39 Cr for the quarter

- Number of Gold loan branches were 3330

- Provision for the standalone entity was 24.59 Cr which was 0.7 %

- Consolidated net worth stood at 3836 Cr

- Consolidating borrowing stood at 12593 Cr

- Capital adequacy stand at 27 %

- Gold loan growth yoy was 2.6 % qoq growth in gold ton stand at 54 ton

- Micro finance business had bounce back . Expect growth in micro finance and gold

- Non gold portfolio collectively grew by 59 % for the full year led by commercial vehicle growth which was double putting together contribution was more than 25 % in the total AUM

- ROA stood at 4.04 % and ROE at 17.81 %

Q&A

- What was the company Gross NPA in the housing sector in last quarter and current quarter ?

o Currently its 4.7 % and last quarter it was 3-3.5 %

o Spike in the NPA was low in last quarter and now it slightly growing - What about collection efficiency of Asirvad ?

o Company is at 99.6 % currently more then par of 1.3 % in the par more then 90 days - At what scale does company see cost to income after getting at 100-125 Cr income level ?

o It will come down going further , it was high just because of demonetisation last year so company was not able to do disbursal and growth

o Currently it is 6.7 % and it will come down to 5.9 % next year and it is best performing in the Industry - Will company have a problem from Tamil Nadu elections in disbursement ?

o No company had totally moved toward direct bank credit so there will be no problem from elections and same was experience in Karnataka elections also . Collections are much smaller then Disbursement

o Micro finance in not part of any farmer waiver loan scheme from government . There can be a dip for 1 or 2 months in collections temporary

o Concentration of a particular area has also coming down , it was 80 % some years ago and now it is less then 30 % . Company is managing the portfolio by spreading it - Why company NPA is still High Housing segment and how does the company see competition in housing segment ?

o There is stress going on in the market and lot of competent increase as there were 64 players few years back but now 94 players and another 14 licenses are gone for approval with NHB . But issues will sort out in coming future all the assets are on the book and provisions are made more then required . Standard of asset provision is also more .

o In last quarter company ambition was not to grow but to find a resolution because there was some stagnation in the portfolio . Now with the new team in place , disbursal had started

o GNPA in another one will come down to another 2 % - From total 60 % borrowings of bank what percentage will come from PSU banks and what is the incremental cost of borrowing ?

o Around 60 % of overall borrowing come from PSU banks . Incremental borrowing cost will be 8.8 % - What is the reason behind not good growth in Income from operation in spite of closing good AUM ?

o Company is in stabilizing stage and competence scenario is increasing and micro finance will be turning around in FY19 expecting substantial contribution in bottom line and company is going to add housing finance fast so it will add to top line - Does company is in position to increase debt level at current yield ?

o Whatever the yield will be It can be pass on - What was the auction number for the quarter and last quarter ?

o 89 Cr and last quarter it was 84 Cr - What capital will be require for growth in housing finance going forward ?

o Housing finance is already capitalised by 100 Cr so it will not require capital

o In Asirvad company had put capital of 150 Cr so there will be need of extra capital in end of FY19. - What was the profits in the housing finance segment in FY18 ?

o It ended up to 8 Cr - What is the reason behind significant increase in gold loan disbursement from last 2 quarters in spite of not much increase in AUM growth ?

o Because of challenges of Demonetisation in Q1 and Q2 there was low disbursement then in Q3 it get normalised and then again business churn up so that is the reason for Gold loan disbursement and it is coming in AUM also - Why was the operating revenue side was very weak in the last year and how it will get correct in FY19 ?

o Average revenue had grown by 4 % and on operating expense side as company is working on technology so the security cost will come down and overall administrative expense to come down in FY19 - Any guidance on Credit loan business and tax rate ?

o The NPA will be coming down and the tax rate will remain the same - What is the actual addressable market of Gold loan for the company compare to unorganised sector ?

o Unorganised sector is still very large . Client will shift because of higher technology , Online Gold option , higher security . Unorganised sector must be around 2-3 times of organised sector - What contribute to significant jump in other loans ?

o These are some loans that company had give to other NBFC where company is making yield of around 14 % . These all are rated corporates that have IFA market . Company had lend it because company capital adequacy was higher - After infusing 100 Cr in Asirvad what is the company total stake ?

o It is now 95 % - What is the company plan with Asirvad going forward ?

o No merger will be there . Company can go for a IPO for further capital requirement going forward - What will be the company further strategy for borrowing mix ?

o Company have a large customer base so company can go for a NCD and as of now company is not known about where interest rates are headed . Company is very much comfortable on the ALM. Company have further sanctions in place

o Borrowing cost should be below 9 % going forward - What will be the operating expense going forward ?

o Company believe it can be 7 % going forward - What was the average yield during the quarter ?

o Gold loan yield is around 24 %

o Commercial vehicle is around 18-19 %

o Asirvad is around 22 % - What percentage of borrowing will be reprised in FY18 ?

o Around 1000 Cr of NCD will be coming up which are around cost of 11 % because these are all old NCD and also have bank loan which are short term - In vehicle finance which sector is company focusing on ?

o Mainly on Commercial vehicle

90 % of that is huge commercial vehicle

o Also started two-wheeler loan which is a very good cross sale opportunity and currently it is in few states not in PAN India - What is the Consolidated number in GNPA and NPA ?

o GNPA on Gold Loan is 0.6 % , commercial vehicle is 2.7 % , Housing finance is 4.8 % , Asirvad at 2.3 % - What is the average tenure of micro loans and gold loans ?

o Gold loan average tenure is two months , in micro finance it is around 18-24 months - When the tenure reduces how does it impact on asset quality ?

o Gold loan asset quality goes up as margin of safety increases

o In micro loan the shorter the tenure is good but it depend on customer income and competitive scenario - What is the period of company gold options ?

o It happen all the time , it is not centralised so different regions have it - How does company see Housing finance sector in coming period ?

o Housing for all scheme under prime minister has boosted a lot of competition . Affordable housing is very much happy segment and there are many players looking at it

o Now government had requote the PMAY Gram and PMAY Urban also and March 19 the deadline is given for the gram part .

o Lot of good players will come in organised market supply side will increase because of meaning full lending opportunity and demand will also increase

o Company is focusing on territories and big cities also in entire Tier-2 and Tier-3 segment. This is a 4-5 year play . Company had set up very good online platform for Housing loan which is going under phase which will deliver top line growth and have control on the delinquency - How much was the total amount of Gold auction in FY18 and FY17 . What is the normal recovery rate in terms of amount that can be recovered ?

o Get almost 90 % of the amount in the auction . Total was 4.5 ton in FY18 similar to FY17 . In FY 17 amount was 929 Cr and FY18 it was 900 Cr - What will be the net interest margin in FY19 ?

o It is regulated and it is 10 % company cannot go beyond it - What impact can be seen if gold prices fallen sharply ?

o Previous when it happen then also company was success to deliver good returns . Gold will not go down in one spike it will go gradually so on daily basis company is correcting it on LTV basis . Company is not expecting much downfall in gold prices

o There could be shrinkage on the yield when the loans are pre return so that is the challenge - Does auction cover both interest and principal ?

o Company collect more then 90 % and company LTV is more then 70 % . - What kind of product is company new Gold loan product that if offer at 9.9 % ?

o It is an online gold loan product . This is for loan above 50 lakh which are few in number

14 Likes

V.P. Nanadakumar’s commentary on Q4 FY18 and FY19 guidance:

CFO Kapil Krishan’s commentary on the results as well as the reason for his resignation:

Q4 FY18 Conference Call transcript:

2 Likes

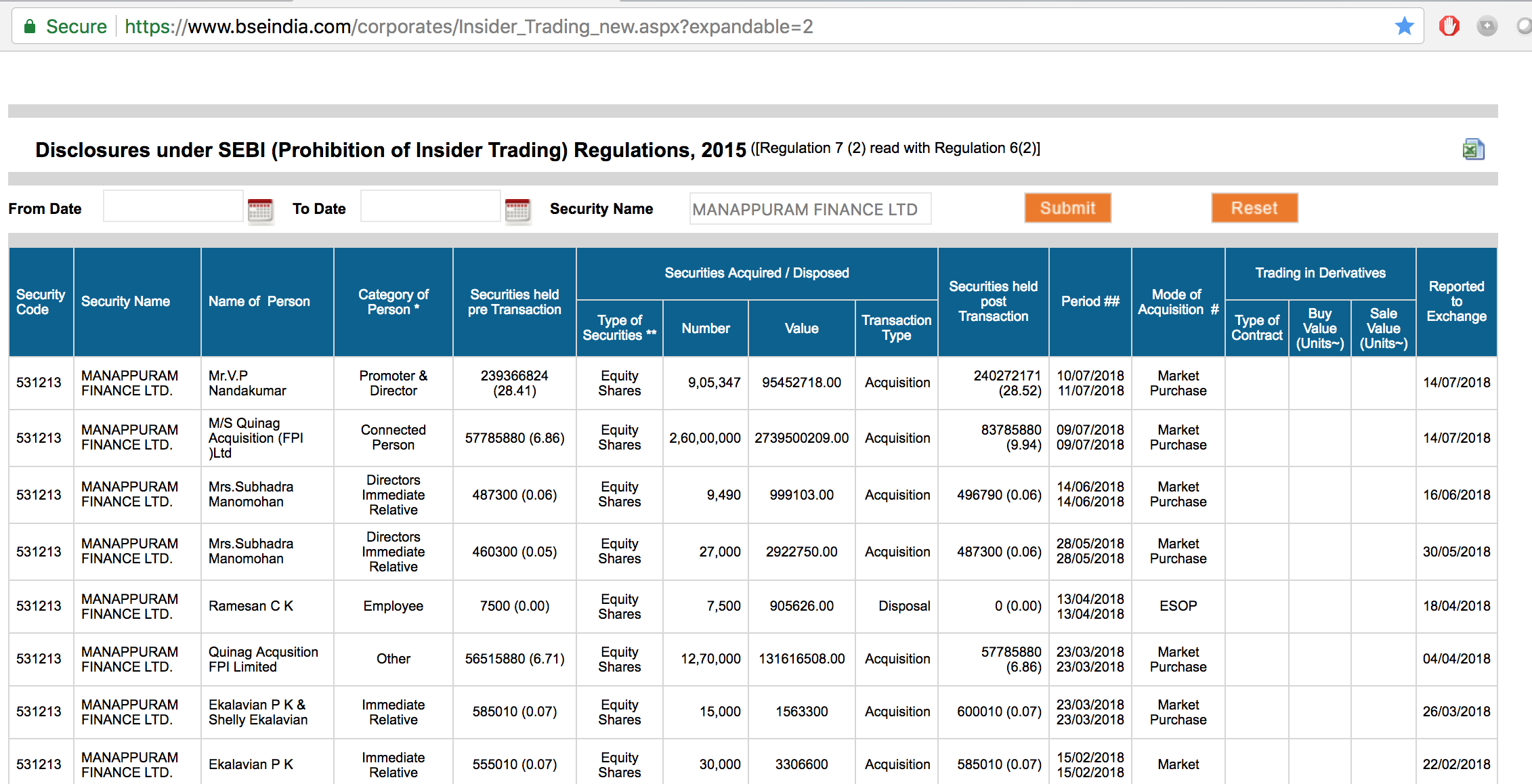

Directors Immediate Relative bought 27000 shares on 28th May.

Manappuram Finance: Company To Consider Issuance Of Private Placement Of Rated, Listed, Secured, Redeemable Ncds

Acquisition of ISFC for 212 Cr

2 Likes

From my initial reading - the company has a real high quality talent pool and is on an aggressive growth path. Manappuram will be definitely be able help IFSC reduce the finance cost and help them expand to other geographies - Valuation of about 4 times books seems to be reasonable considering they are growing at a brisk pace(>60% annually).

Looks to be a complete win win.

What to know more about the latest acquisition? See the credit rating reports of ISFC below -

Indian School Finance -R-September 2017.pdf (224.3 KB)

Indian School Finance- March 2018.pdf (198.4 KB)

Disclosure: Invested in Manappuram

3 Likes

I wouldnt reach that conclusion so fast. In my opinion, prima facie it looks like an act of diworsification for the sake of it.

Gold loan is a very attractive and low risk business. First because these are small loans given to a large number of retail borrowers. Hence the risk is well diversified across a large number of borrowers. Second even in the case of default, there is a collateral which can be “easily” sold and the loan recovered. The major risk in gold loan business is of a sudden and precipitous drop in the price of gold.

I dont know much about the business of lending to affordable schools. And i bet Manappuram doesnt have much expertise in this area either. Plus this is a business which has low profitability and higher risk than the gold loan business. Profitability - Gold loan ROAs are of the order of 4% as against 2% in this business. Risk - The loan amounts in this area are much higher. A few defaults can make a dent in the profitability of the entire business. That seems to be happening. From the report - “ISFC’s asset quality indicators deteriorated during FY2017 with 90+ DPD of 1.45% as on March 31, 2017 as compared to 0.93% as on March 31, 2016. The deterioration was mainly on account of slippage of a few big ticket accounts and the impact of demonetisation on collections.”

Manappuram had a business which was antifragile. They have turned the business into a fragile business through this acquisition. Because in the lending space, one thing which we can be sure of is that mistakes will invariably happen. In the gold loan, mistakes don’t cost the company much. But they will in this new space.

Positive thing about the schools is that they have a stable and annuity source of revenues. Hence my fears may turn out to be unfounded. But when I invested in Manappuram i was looking for exposure to gold loan. Hence I would look to shift to Muthoot.

7 Likes

I didn’t understand how is this additional line of biz is diworsification? The primary biz is lending and lending for a defined purpose can not be called an unrelated biz. The writing on the is that gold loan growth has stagnated across industry and will require additional line of lending to grow their balance sheet. Listen to Rashesh Shah why NBFCs need to be adequately diverified for their long term sustainability.

Coming to this acquisition which is very small compared to overall size of opportunity and even Manappuram’s AUM. I would look at this as an excellent opportunity rather than a problem child. Expenditure on education will grow and should support higher leverage going forward.

7 Likes

While I agree that this is a good opportunity for Manappuram to deploy their capital to scale up the business. And this can provide the much needed growth since the gold loan business has been stagnating.

But my point is that the acquisition will dilute the quality of the business from a perspective of risk as well as returns (in the long term). Every investor should judge for themselves whether they are willing to pay that price for growth.

I am not because i believe that gold loan business is much more attractive and I value quality and low risk over growth. The growth in this business has been disappointing for the past few years. In this lean period, my preference is for the management to be patient and continue to work on the core business instead of getting distracted with other lower quality businesses. When the growth comes back as it will in my opinion, the wait will be worth it.

3 Likes

The acquired company has 3% RoA and leveraging it 6x will give you 20%+ RoE closer to what Manappuram could earn on consolidated basis. Even HDFC has separate education sector vertical managed by a different team. What do you mean by gold loan being high quality biz? Whatever is good for a customer is great for businesses ultimately. It might be great for investors but not so for borrowers currently. That is one reason gold loans don’t get great valuation. Ask a question to yourself - would you go and mortgage your jewelry in normal circumstances?

I consider gold loans as necessary evil for a society in which there are large numbers of undisciplined or distressed borrowers. The credit system needs to be extra cautious and probably punish them with high interest rates for their lack of financial planning or extra savings. Sustainability of gold biz in very long term is always in doubt.

BTW Quinag acquired another 3% stake today in a block deal to take their stake to 10%.

6 Likes

Mr Nandakumar’s interview regarding IFSC acquisition

3 Likes

Manappuram promoter bought over 9lk shares from open market. Every quarter when company announces dividend, promoter increased his holding consistently

1 Like

quinaq bough…but @aniljain u just mentiond promoter bought also…can u share link for that

Any news of the new CFO? Kapil Krishnan’s last working day was 30th of June 2018.

Manapuram AR 18 notes

AUM – 15,765 cr ; 15.4 % yoy

Gold loan disbursements – 62, 155 cr ; 18.5 % yoy

NII – 23957 cr; 8 % yoy

Total customers – 3.8 million ; 12% yoy

• Digitalization important part of our strategy

• New businesses 1/4th of our AUM , will go up in future

• 2/3rd of Indias GDP is in gold in households , right now only 10 % monetized , we hope to encash this

• Gold – 64 ton assets

• Borrowing cost – 8.7 %

• 4199 network branches , 24886 team of employees

Gold loan Division

• Gold loan AUM Rs.11,700 cr ( 5.5% growth)

• NP – 700 cr

•

Asirvad Microfinance

• MFI AUM 2437 cr vs 1796 cr ( 35 % yoy)

• Gross NPA 2.33 % NPA vs 4.47 % last year( seems like bad effects of demonetization are going off)

• Total branches added 69 ( 832 total)

• 2nd half of the year was much stronger , provisions for the year at 17.2 cr declined 57.2 % yoy

• This segment can be a major growth driver

Housing finance

• AUM at 375 cr ( 20.7 %)

• Plan to touch this AUM to 1000 cr , in next 2- 3 years .

• Opex brought down to 8.44 % from 10.3 % last year

• Gross NPA – 4.8 %

• Western region contributes the largest share of the loan portfolio.

• 419 staff, parent company( Manappuram) can put in equity when required

• Average ticket size of a Home Loan is about 11.50 lakh and for the LAP segment, it stands at about 8.00 lakh.

Vehicle finance

• AUM doubled to 625 cr

• Added 26 new branches taking total to 76

• Leveraging gold loan channel for this

• Gross NPA – 2.7 %

• Planning to add 26 new branches this year

• 70 % preowned vehicles

•

Gross NPA at 0.5 % vs 2% last year

Net NPA at 0.3% vs 1.7 % last year

Return on assets at 4 % vs 5.4 % last year

Employees at 23886 vs 18993 last year ( 26 % increase)

Online gold loan account for 32 % of the book as against 12 % last year.

Planning to venture into new businesses like corporate finance, personal loans, MSMEs , project and industrial finance

27.28 cr spent on branding and advertising

MD&A

NBFCs gaining an upper hand to banks as banking secotr

Bond yields and loan rates are on the climb ,will adversely affect margins

Limited opportunities to grow in gold loans, gold loan NBFCs are focusing on other areas

Obtaining gold loans is relatively easier to other loans , hence its rising popularity

Untapped markets of north and west india hold opportunity for gold loan penetrations

Gold loans have flexible terms , no need to pay EMI , can pay interest at end of tenure

Organized gold loan market to touch 3101 bn by 2020, growing 12-13 % CAGR

In August 2017, CARE Ratings has upgraded the long-term credit rating of Manappuram Finance Ltd (MAFIL) to CARE AA (double A) stable from CARE AA- (double A minus) stable

The Company also invested in ramping up safety of the lockers by installing IOT-based keyless e-lockers which offer multiple benefits including monitoring of the lockers by the customer from a remote location.

24 Likes

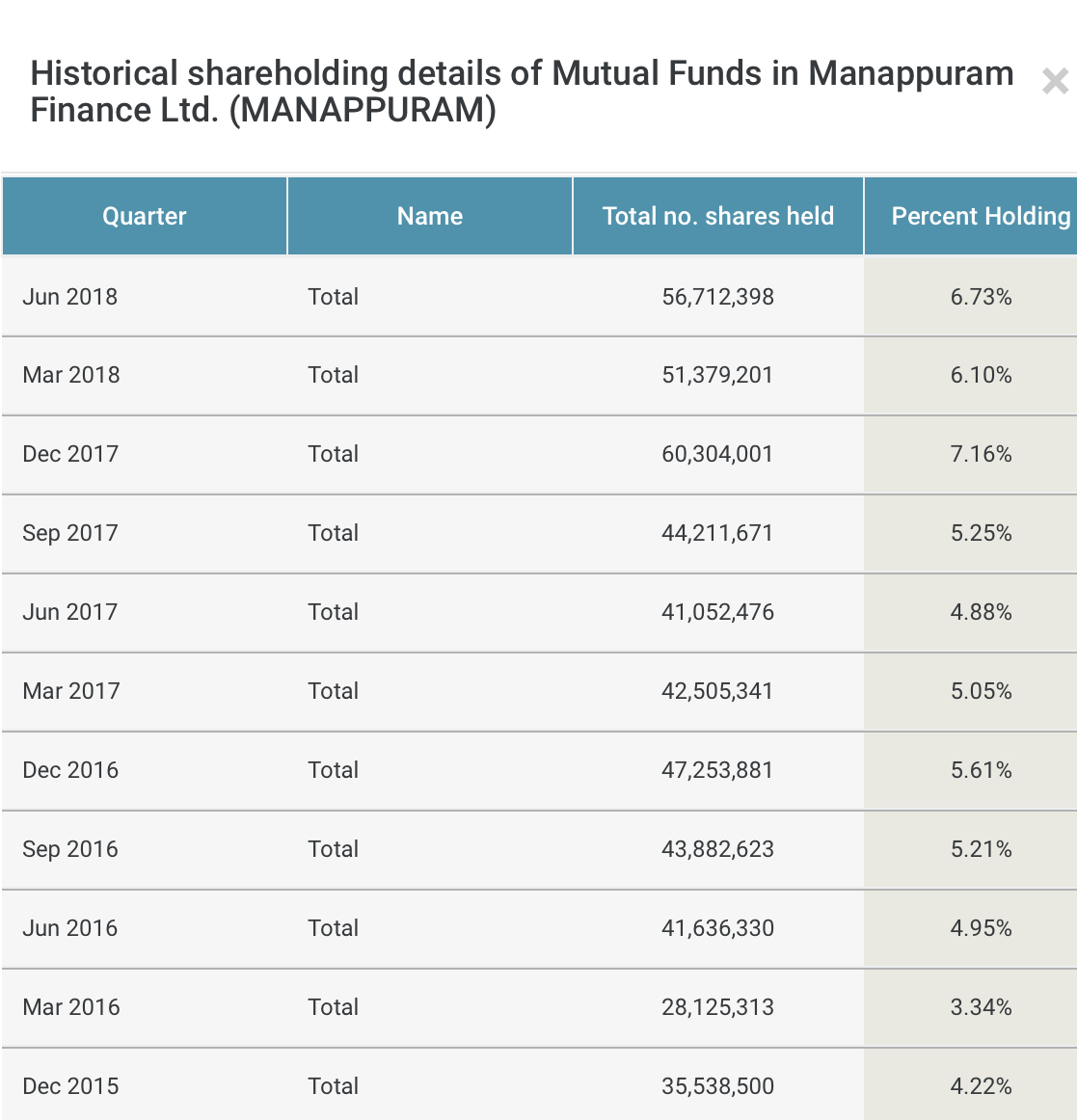

Mutual Fund holdings of Manappurum Finance has shown a decrease in the month of June’18

Source : https://www.rupeevest.com/Mutual-Fund-Holdings/131213