Few more bits

I think worst may be over for Majesco in term of customer acquisition and revenue growth, but Majesco is unlikely to report consistent profitability in next few quarters. Here is my question to management in Q2 FY18 (US)

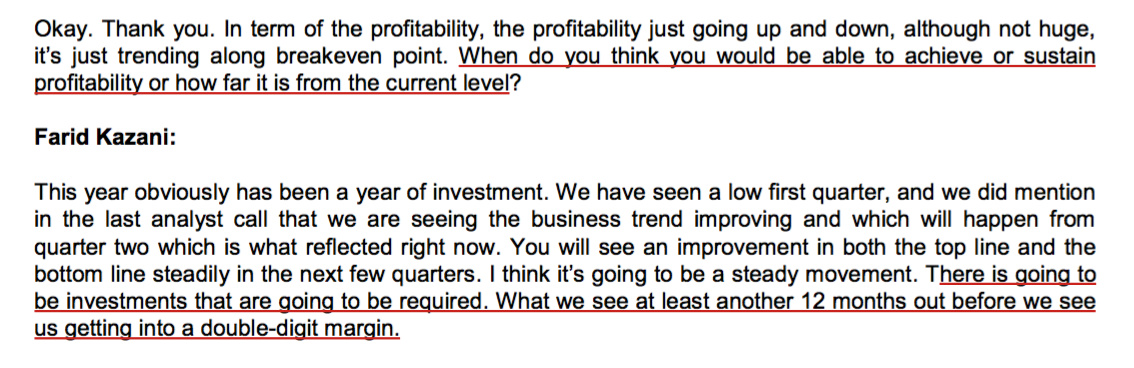

Management talked about at least 12 months away from consistent profitability in Oct, so hopefully, by (Q2-Q3) FY19, they will report consistent/double-digit profitability. But I have seen last few quarters have seen a clear turnaround in a positive sense.

In Q4 FY16, Majesco ramped up the sales team and management has set an ambitious goal of reaching $200 million by FY18 (I know they are way off from that now). In a subsequent quartes, they indicated that the sales cycle is long and it takes around 12 to 18 months before a deal is signed with a customer. I think increased sales team hasn’t delivered clients deal in a times frames the management had indicated. But based on the current deal’s announcements, I have a feeling that sales activities are beginning to deliver results. Hopefully, it will continue.

I think subscription revenue is the key to consistent profitability. Currently, subscription revenue is around 9%. In my view when it reaches 12-14, it will be more or less equal to R&D expenses. Management has indicated that the R&D is a kind of fixed cost. In fact, if they manage to increase the sale at a good pace, R&D as a percentage will go down on it own.

The current Market cap is around 1400cr. Majesco has raised 240cr plus they have cash and cash equivalent of 110cr in their book. It means that 25% of the company’s value is in cash. And Majesco is not burning money as such. Operationally, they are generating profit, but it is not meaningful. It means a significant portion of the 350cr, is available for M&A activities.

M&A- Instead of making one big acquisition of $30-$40 million, Majesco may go for two acquisition (I have no knowledge, I am just speculating). It may give them more customer to cross-sell their products. Guidewire is acquiring companies very aggressively in last few years, so Majesco needs to move swiftly.

I am trying to validate one assumption about cloud profitability. Majesco management has indicated in the past that first three years of the cloud contract are not profitable. However, the real profitability will start after year four onwards. I am investigating if that assumption still holds true. Maybe this is a question for a next con call. However, if anyone has an idea/article on profitabilities on cloud business in general, please feel free to share.

Overall, how many customer they acquire in the next few quarters along with M&A will decide the directions for the company.

Disc- Invested, hence my view could be biased.