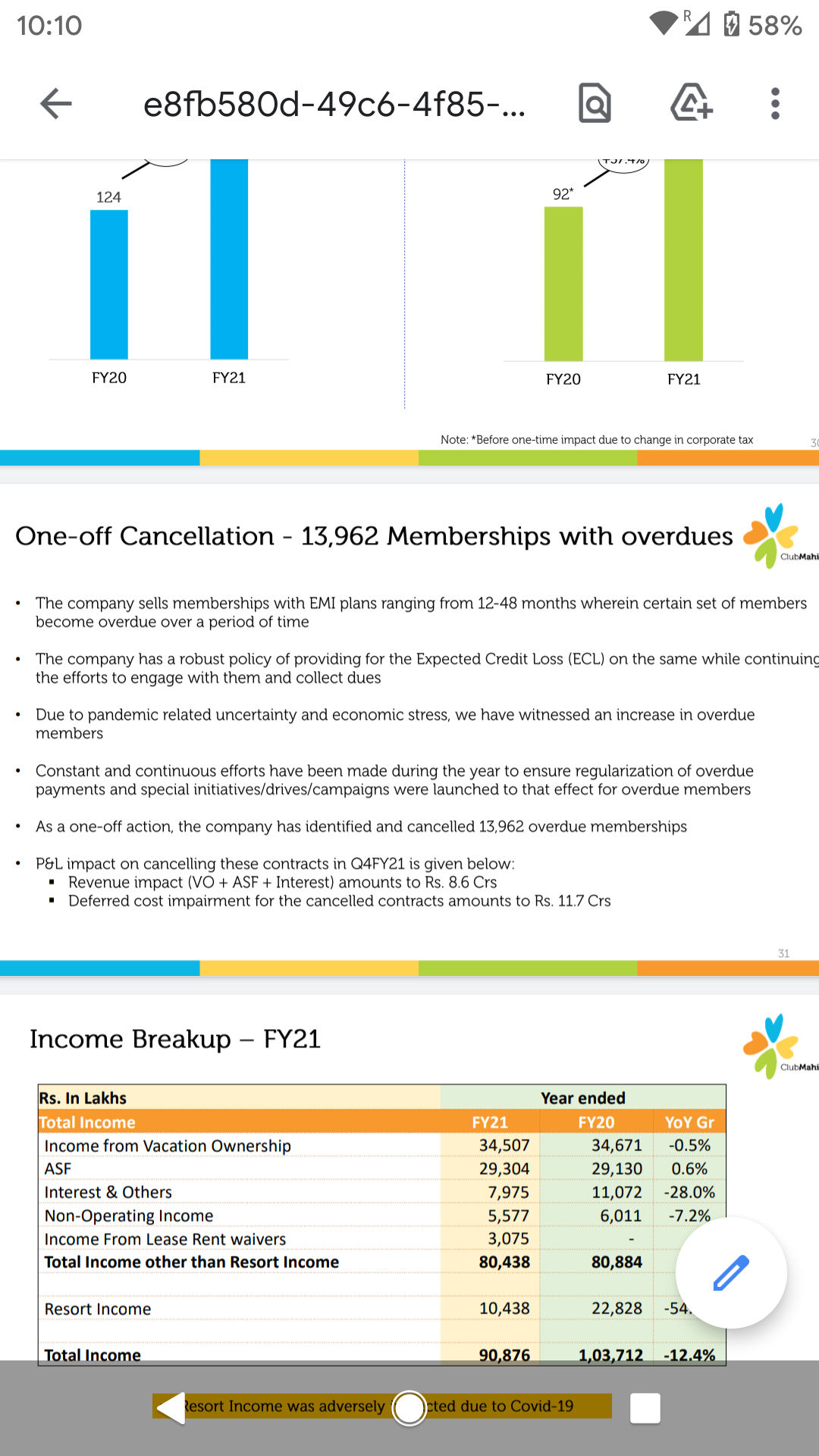

There is a note in the presentation

“VO Income and ASF Income was lower in FY21 due to one-off cancellations”

Also, both are unrelated. ASF comes from all existing members, so even if new membership sell is zero, ASF will largely remain intact.

There is a note in the presentation

“VO Income and ASF Income was lower in FY21 due to one-off cancellations”

Also, both are unrelated. ASF comes from all existing members, so even if new membership sell is zero, ASF will largely remain intact.

Yes, as you mentioned it’s there in the investor deck.

One off membership cancellation figure

is higher than the new member additions. Hence that explains the drop in ASF as net member addition is negative!

A detailed article highlighting the vacation ownership industry and Mahindra holidays can be found in the link below.

What is the company doing with so much extra cash? Why did they shelve the plan to move into 5star hotels within city limits? Nor have I heard any acquisitions? Atleast they could pay dividend if they don’t have other expansion plans… have not paid dividends since 2018

@Mayank.mail MHRIL plans to utilise the excess cash for expanding its resorts / room inventory. Glad that they did not move into 5-Star Hotels. Hotels, especially 5-Star hotels are very capex intensive, too many moving parts in a hotel business as compared to vacation ownership which is cash +ve and a +ve flot business. 5-Star Hotels are also lower margin businesses in comparison to MHRIL’s core business. MHRIL’s acquisitions have not played out, their HCR (Finland) acquisition was a mistake and has been a loss making venture for MHRIL. Wish they would sell HCR.

But doesn’t HCR help increase in number of rooms available for members?Also for exisiting members and new members resort network outside india is a welcome addition .

Can you provide reference when they had plan to move into 5star hotels in city limit?

A club Mahindra member going west of India for vacation, where he is most likely to go?

My thinking is that unless he has done 3) and/or 2), he is not going for 1)

Unless number tells otherwise, I am not of view that HRC helps increase in number of rooms available for Indian members. Do we have numbers or commentary from them?

Hi - Per consolidated balance sheet, borrowings - loans have increased from 32667 to 80706 for YE March 31, 2021. Analyst meet talks about HRC having a borrowing of Euro 26M and cash of Euro 12M. Presentation mentions zero debt company.

Seems like zero debt is on standalone basis. Would anyone be able to shed light on increase in borrowing - more than double when co. has rich cash balance. A heavy debt co. is not a good trait during COVID times. Thanks and stay safe

@ laxman_sreekumar Agree with @ Gupta Regarding HCR, 33 out of 34 properties are located in Finland. Indian travelers prefer a variety of locations (countries, like covering 5 European countries in 2 weeks) and experiences when they travel overseas and majority would not prefer to stay in an single location as it is not a good ROI when you factor travel, air fares just to travel to a single destination, hence HCR will not appeal to most Indian travelers (read as MHRIL customers) and HCR does not add value to MHRIL’s portfolio. The oroginal thinking was to expand international footprint but that thesis has not played out

JR_R Reg Zero Debt, MHRIL is Net Debt positive. There is some debt in HCR books and HCR debt has also gone up in FY21 but HCR also has cash. I guess the reason MHRIL is keeping this debt is because cost of debt in Finland / Europe is very cheap. Though MHRIL can payoff the HCR debt from the Indian books, MHRIL prefers to invest the cash in treasury which yields much higher return in India and it might be using the returns from the free cash / reserves to pay off the HCR debt interest. This is a good / smart arbitrage from MHRIL

If we take out 2017 and 2018, the net profit shows declining trend since 2010. Negative net cash flows for more than half the time since 2010. I wonder why market values this company at the current valuation. One major positive probably though is management is trustworthy and very honest.

valuehunt Reported revenue & PAT numbers in P&L and Balance Sheet (BS) will show poor growth / de-growth. If you dig deeper into the balance sheets you will find that changes / decline in profits, revenues & margins (all trending lower) over recent years are on account of change in revenue recognition policy and shift from Ind AS 115 to Ind AS 116 accounting standards.

Till a few years ago MHRIL had an aggressive strategy of booking 70% (maybe 60%) of new membership revenues in Year 1 and spreading the reminder 30% over the customer life cycle, mostly 25 years. With the change in accounting and BS restructuring MHRIL is and has to book revenues over the customer life cycle. For a 25 year plan, MHRIL can only book 4% of the revenues every year. MHRIL’s revenues are almost on par with an annuity model. There is revenue visibility for 25 years with each passing year. This information is available in the Earnings Call transcripts of 2018/2019

Some salient features of MHRIL business model which in my view is very unique.

Hi pskrishnan - Can you numerically elaborate how MHRIL is net debt positive? Per analyst call, debt (Euro 26M) of HCR is more than cash (Euro 12M). Per consolidated balance sheet, borrowings - loans are 80706 against cash & bank balance combined of 40255. Awaiting the annual report (notes to accounts), cannot comment on the nature of financial assets - thus, have not factored in.

Further, from debt:equity ratio, debt is 80706 vs equity of 8467

We need to understand the breakup of the Borrowings figure in the consolidated balance sheet.

Operational Debt of HCR like you mentioned is only 26 Mn which translates into Rs 230 odd Crs,

MHRIL via one of its subsidiaries over the years has taken Debt to acquire ownership in HCR. If i am not wrong the cumulative investments in HCR total to around 70 Million Euros. Which Translates into around Rs 650 Crs. The interest on this debt gets serviced by the dividend that HCR pays. So effectively this debt is not an actual debt and should be knocked off against the investments. And this is also why in my opinion one should not consider HCR in valuation of Mahindra Holidays as Net Enterprise Value of HCR will be Zero (for now, as the story changes once they start monetizing their stake above their cost of investment)

So MHRIL effectively is a Debt Free company having a cash balance of Rs 940 Crs.

Hi,

The annual report is now available: 6aae3f2b-8d95-41e3-9ffe-b0395d4136fb.pdf (bseindia.com)

Can you please let me know how the debt figures are panning out. I am not very savvy to read the fine-print in the statements. It seems the cash on the books is slightly exceeding the outstanding debt. Thanks!

Hi, You will have to analyze subsidiary annual reports for those details as HCR is owned by one of MHRIL’s subsidiary.

Again to reiterate what I am saying, Comparing the debt of the Consolidated balance sheet with Cash of standalone business wont be right because bulk of this debt (Around 70 Mn Euro) was taken to buy stake in HCR. I estimate HCR entity to have an enterprise value around 70 Mn Euro’s thus Net Equity Value of HCR for MHRIL is Zero (As Enterprise Value of HCR gets fully offset by the debt they have taken to acquire it) and thus one should only value MHRIL on standalone numbers.

Q2 concall